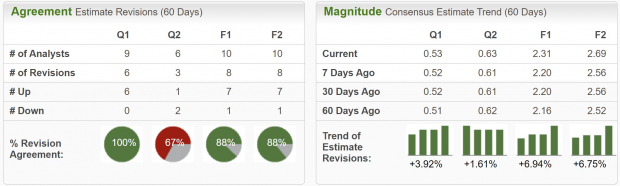

After a very strong first quarter this year, many restaurant stocks experienced more challenging price action as the macro environment entered a period of elevated uncertainty. However, many of these stocks are reporting strong earnings this quarter and look ready to make another bull run into the year end.Although a number of restaurant stocks have reported earnings this and last week, I am going to highlight the four stocks that I think present the most compelling opportunities in the sector.  Image Source: Zacks Investment Research WingstopWingstop (WING) is a popular American restaurant chain specializing in chicken wings. Founded in 1994, Wingstop has grown into a prominent fast-casual dining brand with over 1,400 locations world-wide known for its flavorful and customizable chicken wing offerings. The company’s menu features a variety of wing flavors and styles, along with a selection of sides and dips. Wingstop has a strong presence in the United States and internationally, with a focus on takeout and delivery services.Also, as a chicken wing expert myself, I can personally vouch for the quality of Wingstop’s wings.Wingstop stock has rallied nearly 50% YTD on the back of powerful sales growth, new openings, and digital penetration. Additionally, the stock has a Zacks Rank #2 (Buy) rating, reflecting upward trending earnings revisions.At its Q3 earnings meeting this past Wednesday, Wingstop showed continued progress in business growth. Earnings of $0.69 per share came in 33.2% above analysts’ expectations while sales of $117 million beat by 7.4%. Net income showed a 46% YoY increase and total revenue grew 26.4% YoY.

Image Source: Zacks Investment Research WingstopWingstop (WING) is a popular American restaurant chain specializing in chicken wings. Founded in 1994, Wingstop has grown into a prominent fast-casual dining brand with over 1,400 locations world-wide known for its flavorful and customizable chicken wing offerings. The company’s menu features a variety of wing flavors and styles, along with a selection of sides and dips. Wingstop has a strong presence in the United States and internationally, with a focus on takeout and delivery services.Also, as a chicken wing expert myself, I can personally vouch for the quality of Wingstop’s wings.Wingstop stock has rallied nearly 50% YTD on the back of powerful sales growth, new openings, and digital penetration. Additionally, the stock has a Zacks Rank #2 (Buy) rating, reflecting upward trending earnings revisions.At its Q3 earnings meeting this past Wednesday, Wingstop showed continued progress in business growth. Earnings of $0.69 per share came in 33.2% above analysts’ expectations while sales of $117 million beat by 7.4%. Net income showed a 46% YoY increase and total revenue grew 26.4% YoY.  Image Source: Zacks Investment ResearchSomething from the report that I found extremely interesting was that digital sales increased 67% YoY. Wingstop has deployed its own technology stack for accepting and delivering orders, improving communications, and increasing frequency and retention. WING has data on a reported 35 million users!It seems that Wingstop is taking a page directly out of the book from Domino’s Pizza (DPZ) whose incredible stock performance over the last decade was partially credited to its expansion into the digital world. I find this development very encouraging for the term viability of Wingstop’s business.An additional bullish catalyst for Wingstop is its technical chart pattern. Over the last few weeks, its stock has broken out of a prototypical cup and handle pattern, which looks likely to send it to new all-time highs.

Image Source: Zacks Investment ResearchSomething from the report that I found extremely interesting was that digital sales increased 67% YoY. Wingstop has deployed its own technology stack for accepting and delivering orders, improving communications, and increasing frequency and retention. WING has data on a reported 35 million users!It seems that Wingstop is taking a page directly out of the book from Domino’s Pizza (DPZ) whose incredible stock performance over the last decade was partially credited to its expansion into the digital world. I find this development very encouraging for the term viability of Wingstop’s business.An additional bullish catalyst for Wingstop is its technical chart pattern. Over the last few weeks, its stock has broken out of a prototypical cup and handle pattern, which looks likely to send it to new all-time highs.  Image Source: TradingView PotbellyPotbelly (PBPB) is an American restaurant chain that specializes in sandwiches, salads, soups, and milkshakes. Founded in 1977, Potbelly is known for its cozy and vintage-inspired interior decor and its signature toasted sandwiches. The menu offers a variety of hot and cold sandwiches, with the “A Wreck” being one of its most famous creations. Potbelly operates a combination of company-owned and franchised locations, primarily in the United States.Potbelly stock has struggled since its IPO in late 2013, and still trades well below where it went public, but after reporting earnings this week, looks ready to begin its ascent.The technical chart looks to have formed and low and the price is now back above a critical level of resistance at $10. PBPB stock is up 22% just this week.

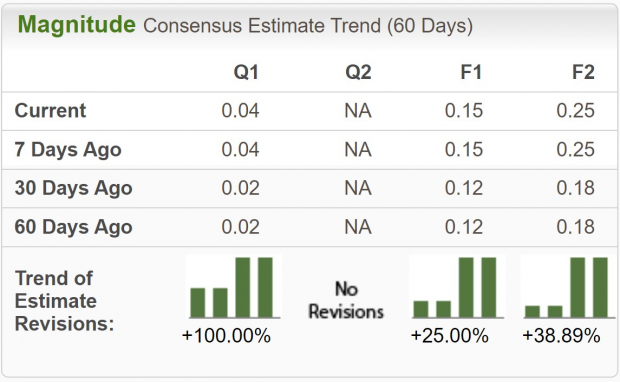

Image Source: TradingView PotbellyPotbelly (PBPB) is an American restaurant chain that specializes in sandwiches, salads, soups, and milkshakes. Founded in 1977, Potbelly is known for its cozy and vintage-inspired interior decor and its signature toasted sandwiches. The menu offers a variety of hot and cold sandwiches, with the “A Wreck” being one of its most famous creations. Potbelly operates a combination of company-owned and franchised locations, primarily in the United States.Potbelly stock has struggled since its IPO in late 2013, and still trades well below where it went public, but after reporting earnings this week, looks ready to begin its ascent.The technical chart looks to have formed and low and the price is now back above a critical level of resistance at $10. PBPB stock is up 22% just this week.  Image Source: TradingViewPotbelly has received some considerable upgrades from analysts over the past two months, giving it a Zacks Rank #1 (Strong Buy) rating. It seems analysts had some good foresight into PBPB’s earnings, because this week it reported very strong quarterly results.EPS were forecast to come in flat at $0.00 per share, but surprised analysts and showed $0.04 per share. Additionally, average weekly sales increased 7.7%, and there have been 150 new shop commitments YTD. Management also raised guidance above all ranges and provided a very strong outlook for Q4.

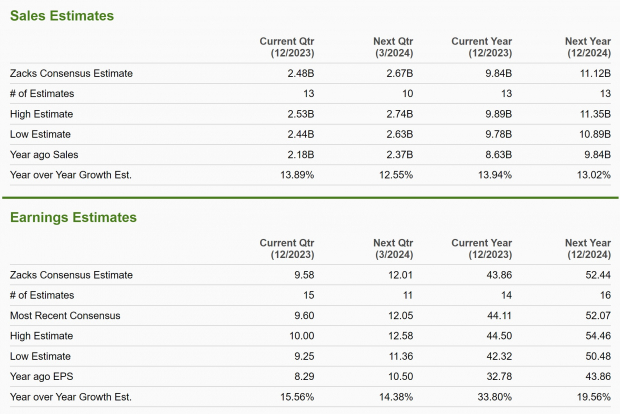

Image Source: TradingViewPotbelly has received some considerable upgrades from analysts over the past two months, giving it a Zacks Rank #1 (Strong Buy) rating. It seems analysts had some good foresight into PBPB’s earnings, because this week it reported very strong quarterly results.EPS were forecast to come in flat at $0.00 per share, but surprised analysts and showed $0.04 per share. Additionally, average weekly sales increased 7.7%, and there have been 150 new shop commitments YTD. Management also raised guidance above all ranges and provided a very strong outlook for Q4.  Image Source: Zacks Investment Research Chipotle Mexican GrillChipotles Mexican Grill (CMG), the restaurant company that brought fast casual to the mainstream continues to build at an impressive rate. Last week, at Chipotle Mexican Grill’s quarterly earnings report they bear analysts estimates on both the top and bottom line, sending the stock 8% over the last week and approaching its all-time high.At the meeting, management shared that total revenue increased 11.3% YoY to $2.5 billion, while operating margins expanded from 15.1% to 16%. Additionally, the company has opened 62 new restaurants over the last year, 54 of which would include a drive through.Chipotle has grown into a mature business but continues to grow sales and earnings at an amazing pace. Sales are expected to continue to grow at a steady 13% annually this and next year, while earnings are forecast to grow 33.8% this year and 19.6% next year.

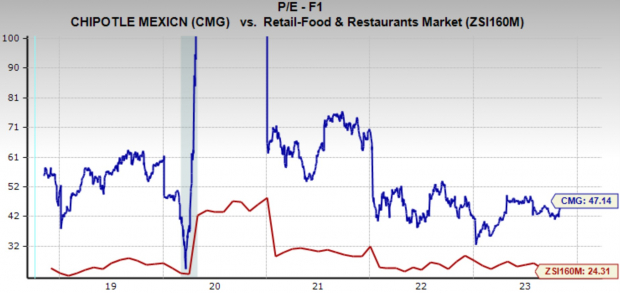

Image Source: Zacks Investment Research Chipotle Mexican GrillChipotles Mexican Grill (CMG), the restaurant company that brought fast casual to the mainstream continues to build at an impressive rate. Last week, at Chipotle Mexican Grill’s quarterly earnings report they bear analysts estimates on both the top and bottom line, sending the stock 8% over the last week and approaching its all-time high.At the meeting, management shared that total revenue increased 11.3% YoY to $2.5 billion, while operating margins expanded from 15.1% to 16%. Additionally, the company has opened 62 new restaurants over the last year, 54 of which would include a drive through.Chipotle has grown into a mature business but continues to grow sales and earnings at an amazing pace. Sales are expected to continue to grow at a steady 13% annually this and next year, while earnings are forecast to grow 33.8% this year and 19.6% next year.  Image Source: Zacks Investment ResearchIt should be noted that those awesome growth rates don’t come cheap though. Today, CMG is trading at a one year forward earnings multiple of 47.1x, which is well above the industry average of 24.3x, but below its five-year median of 54.6x.With EPS projected to grow 26% annually over the next 3-5 years, Chipotle has a PEG ratio of 1.79x.

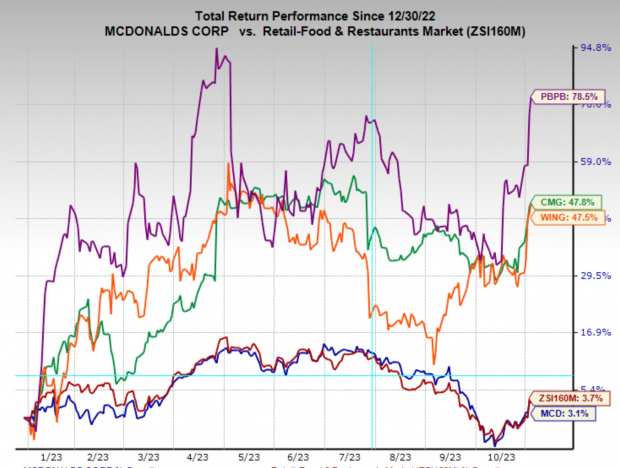

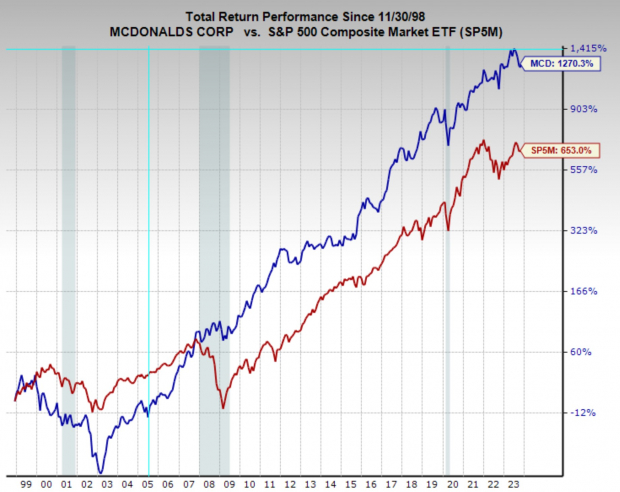

Image Source: Zacks Investment ResearchIt should be noted that those awesome growth rates don’t come cheap though. Today, CMG is trading at a one year forward earnings multiple of 47.1x, which is well above the industry average of 24.3x, but below its five-year median of 54.6x.With EPS projected to grow 26% annually over the next 3-5 years, Chipotle has a PEG ratio of 1.79x.  Image Source: Zacks Investment Research McDonald’sI believe that McDonald’s (MCD) remains one of the great American companies and stocks. Over the last 25 years its stock has doubled the returns of the broad market and outperformed the industry. All the while, McDonald’s has also raised its dividend payment for 47 consecutive years, making it a dividend aristocrat stock and very near a dividend king.

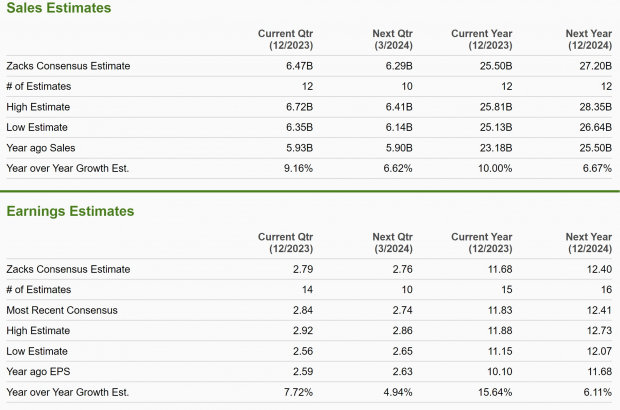

Image Source: Zacks Investment Research McDonald’sI believe that McDonald’s (MCD) remains one of the great American companies and stocks. Over the last 25 years its stock has doubled the returns of the broad market and outperformed the industry. All the while, McDonald’s has also raised its dividend payment for 47 consecutive years, making it a dividend aristocrat stock and very near a dividend king.  Image Source: Zacks Investment ResearchAt this week’s earnings meeting, McDonald’s reported another steady quarter of earnings and sales growth, beating on both the top and bottom line. Total sales grew 11% YoY, while global comp sales increased 8.8%, a very strong reading. EPS of $3.17 was a YoY increase of 18%.Not surprisingly, the company announced an increase in its quarterly cash dividend payment of 10%.Earnings and sales growth are forecast to continue growing at a steady pace, with this year’s sales expected to climb 10% YoY and next year’s sales to grow 6.7%. EPS are projected to increase 15.6% this year and 6.1% next year. Very impressive rates of growth for such a mature business.

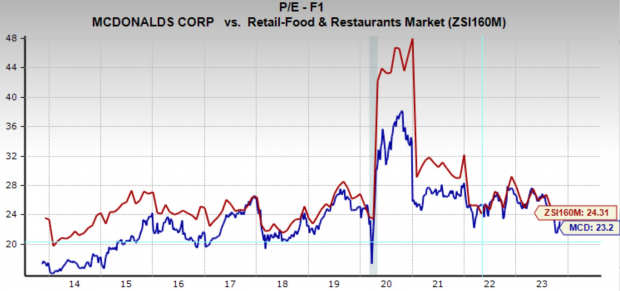

Image Source: Zacks Investment ResearchAt this week’s earnings meeting, McDonald’s reported another steady quarter of earnings and sales growth, beating on both the top and bottom line. Total sales grew 11% YoY, while global comp sales increased 8.8%, a very strong reading. EPS of $3.17 was a YoY increase of 18%.Not surprisingly, the company announced an increase in its quarterly cash dividend payment of 10%.Earnings and sales growth are forecast to continue growing at a steady pace, with this year’s sales expected to climb 10% YoY and next year’s sales to grow 6.7%. EPS are projected to increase 15.6% this year and 6.1% next year. Very impressive rates of growth for such a mature business.  Image Source: Zacks Investment ResearchToday, McDonald’s is trading at a one year forward earnings multiple of 23.2x, which is below the industry average of 24.3x, and just below its 10-year median of 23.7x

Image Source: Zacks Investment ResearchToday, McDonald’s is trading at a one year forward earnings multiple of 23.2x, which is below the industry average of 24.3x, and just below its 10-year median of 23.7x  Image Source: Zacks Investment Research Bottom LineAlthough many new entrepreneurs hear that restaurants are the hardest business to break a profit in, the many public restaurant companies would beg to differ. Here we shared four such restaurant stocks with very strong prospects, bolstered by strong growth, and upward trending earnings estimates. More By This Author:Time to Buy Stock in These 2 Attractive Industry Leaders After EarningsTime To Buy The Post Earnings Rebound In Block Or PayPal Stock? 2 Key Quarterly Releases To Watch Next Week

Image Source: Zacks Investment Research Bottom LineAlthough many new entrepreneurs hear that restaurants are the hardest business to break a profit in, the many public restaurant companies would beg to differ. Here we shared four such restaurant stocks with very strong prospects, bolstered by strong growth, and upward trending earnings estimates. More By This Author:Time to Buy Stock in These 2 Attractive Industry Leaders After EarningsTime To Buy The Post Earnings Rebound In Block Or PayPal Stock? 2 Key Quarterly Releases To Watch Next Week