A year ago many strategists were predicting the U.S. economy would be in a recession by this time in 2023. Far from a recession though, the economy continues to experience respectable growth with the advanced report on third quarter GDP showing the economy grew 4.9%. This follows the second quarter GDP growth rate of 2.1%. Also showing favorable results are company earnings reports this year and especially for the third quarter. Through last Friday, 469 S&P 500 companies have reported earnings with 81.7% of the earnings reports exceeding analyst expectations when a typical beat rate is just 66%. Earnings growth for Q3 2023 is expected to equal 6.6% with earnings growth in 2024 expected to equal 11.2%.

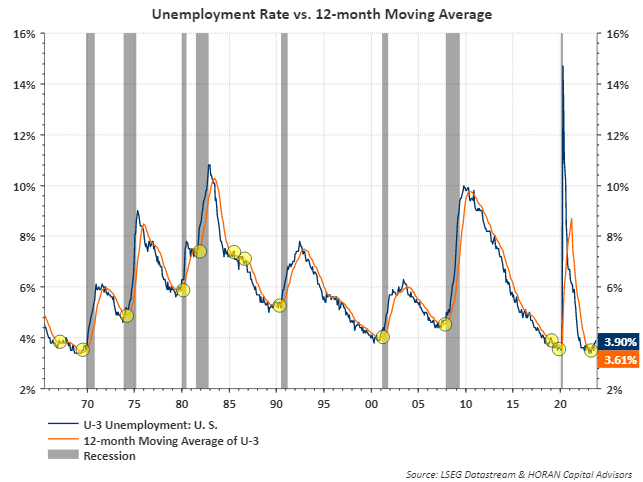

Much of the recent economic reports are providing a mixed picture on the future path of the economy. At HORAN we follow a number of data points that might foretell an economic slowdown. Following are a couple of the reports. Firstly, the unemployment rate of 3.9% has crossed above its 12-month moving average of 3.61%. As the below chart shows, this has signaled a recession approaching on the horizon. Clearly, if companies are reducing their workforce, they must anticipate a slowing economic environment. And, since 70% of economic growth (GDP) is the consumer, lower employment can result in slower economic activity.

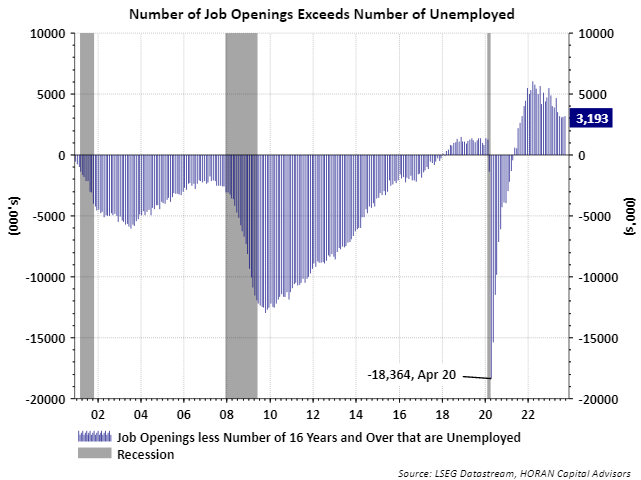

On the flip side of a rising unemployment rate is the fact job openings still exceed the number of unemployed individuals by 3.2 million; however, openings are trending lower.

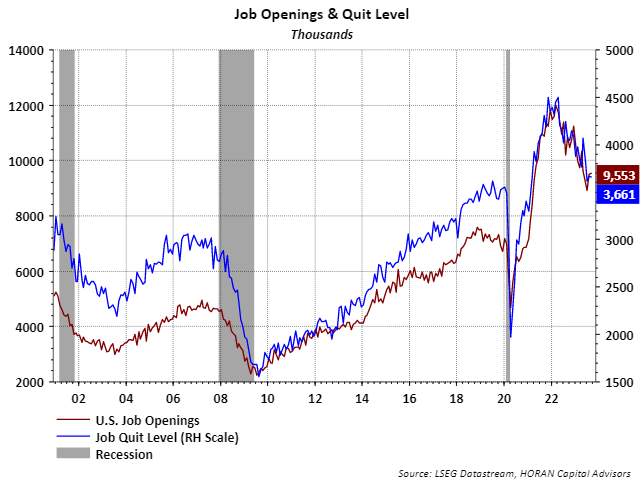

A declining job opening level tends to coincide with individuals quitting at a lower rate as well; thus, signaling a softening labor market.

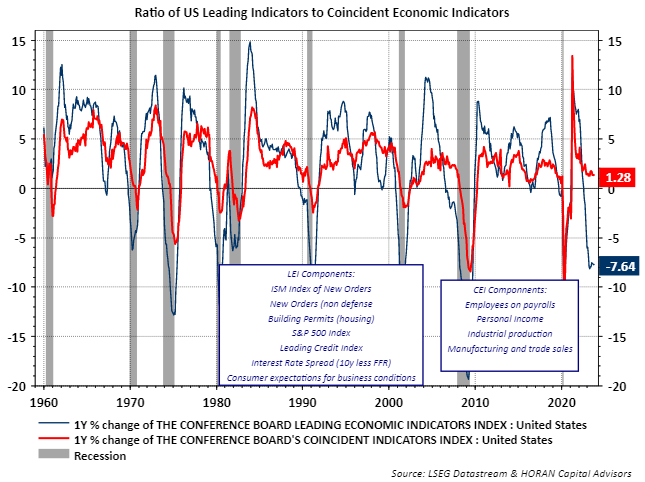

Having noted the weakness beginning to show in the employment part of the economy, the coincident economic indicator (CEI) remains above zero. Notable though is the steeply negative coincident economic indicator (CEI). Two of the components of the CEI are employment-related, i.e., employees on payrolls and personal income. With what appears to be a weakening employment level, maintaining focus on the CEI is worthwhile since economic weakness tends to occur when both of these variables are negative.

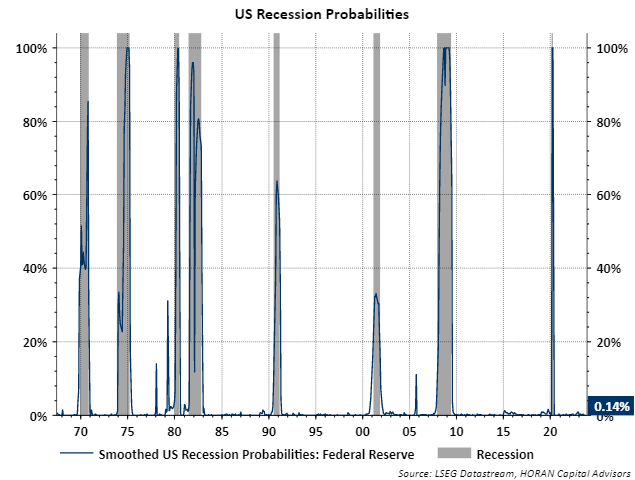

Finally, the Smoothed Recession Probabilities Index remains at a non-recession level and the index includes nonfarm payroll employment data and real personal income data; therefore, in spite of recent employment data weakness, the probability of a recession might be low. More By This Author:Investors Shun Dividend Paying StocksMaybe Time To Look At Small Cap Stocks Equity Market Telegraphing A Strengthening Economy?

More By This Author:Investors Shun Dividend Paying StocksMaybe Time To Look At Small Cap Stocks Equity Market Telegraphing A Strengthening Economy?