The good news is:

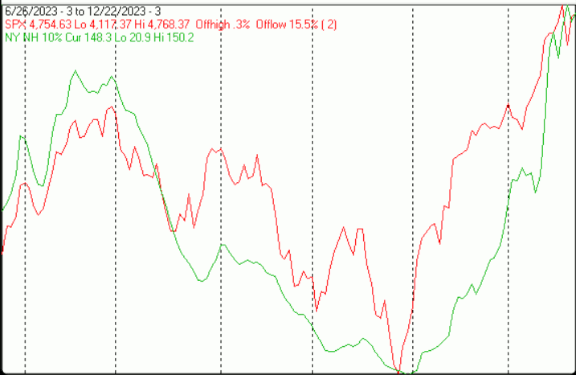

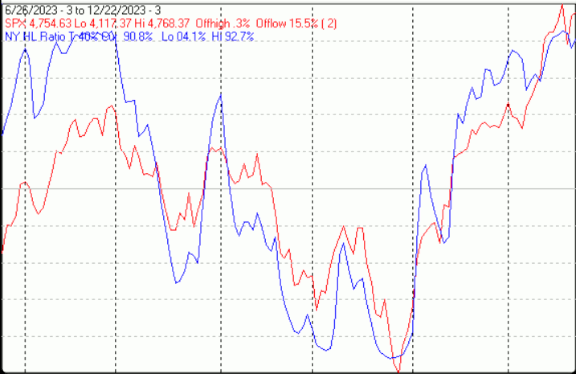

The NegativesThe market is overbought. The PositivesSeasonality for next week is positive.The first chart covers the last 6 months showing the S&P 500 (SPX) in red and a 10% trend (19 day EMA) of NYSE new highs (NY NH) in green. Dashed vertical lines have been drawn on the 1st trading day of each month.NY NH did confirm the SPX at its new high for the year on Tuesday.

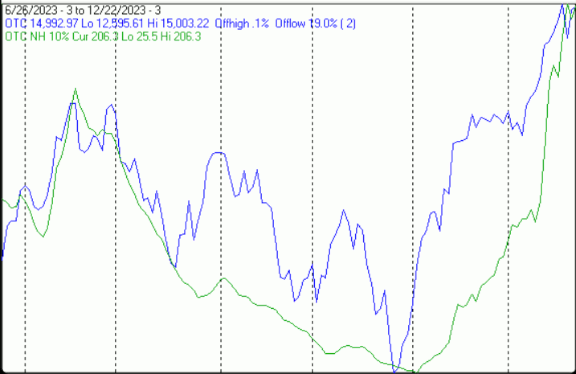

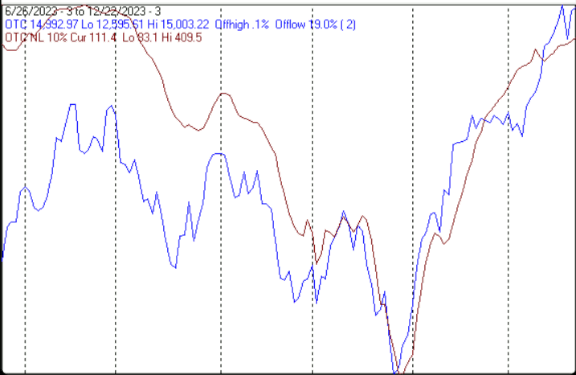

The next chart is similar to the one above, except it shows the OTC, in blue, as the index and the SI’s have been generated from Nasdaq breadth data. No help from this one either.

Report includes the last 4 days of December.

The number following the year represents its position in the Presidential Cycle.

The number following the daily return represents the day of the week;

1 = Monday, 2 = Tuesday etc.

OTC Presidential Year 3 (PY3)

Day4 Day3 Day2 Day1 Totals

1967-3 0.04% 2 -0.09% 3 0.07% 4 -0.14% 5 -0.12%

1971-3 0.44% 1 0.35% 2 0.57% 3 0.12% 4 1.49%

1975-3 0.99% 4 -0.24% 5 0.07% 1 1.77% 2 2.59%

1979-3 0.64% 2 -0.30% 3 -0.03% 4 0.58% 5 0.90%

1983-3 -0.43% 2 0.03% 3 -0.43% 4 0.49% 5 -0.34%

1987-3 0.11% 5 -0.57% 1 -0.20% 2 0.43% 3 -0.22%

1991-3 0.00% 3 -0.36% 4 0.04% 5 0.71% 1 0.39%

1995-3 0.54% 2 -0.50% 3 0.95% 4 0.32% 5 1.32%

1999-3 0.80% 1 0.04% 2 -0.65% 3 1.19% 4 1.38%

Avg 0.20% -0.27% -0.06% 0.63% 0.50%

2003-3 -0.33% 4 -1.43% 5 -0.65% 1 -0.30% 2 -2.72%

2007-3 0.51% 2 0.73% 3 -0.23% 4 -0.42% 5 0.59%

2011-3 -0.16% 2 0.15% 3 -0.15% 4 -0.38% 5 -0.54%

2015-3 0.70% 5 0.00% 1 -0.61% 2 -0.87% 3 -0.78%

2019-3 2.00% 3 0.38% 4 0.08% 5 0.77% 1 3.23%

Avg 0.54% -0.03% -0.31% -0.24% -0.04%

OTC summary for PY3 1967 – 2019

Averages 0.42% -0.13% -0.08% 0.31% 0.51%

% Winners 71% 50% 43% 64% 57%

MDD 12/31/2007 2.65% — 12/29/1987 2.02% — 12/31/2015 1.97%

OTC summary for all years 1963 – 2022

Averages 0.19% 0.05% 0.21% 0.25% 0.71%

% Winners 68% 49% 59% 68% 66%

MDD 12/28/2022 2.71% — 12/31/2002 2.69% — 12/31/2007 2.65%

SPX PY3

Day4 Day3 Day2 Day1 Totals

1931-3 -0.61% 6 -0.27% 1 2.00% 2 1.86% 3 2.98%

1935-3 0.11% 4 2.00% 5 0.32% 6 0.64% 1 3.06%

1939-3 1.18% 3 1.94% 4 0.08% 5 0.53% 6 3.73%

1943-3 -1.13% 1 0.00% 2 1.14% 3 0.10% 4 0.12%

1947-3 -0.13% 5 0.20% 6 -0.33% 1 0.86% 2 0.59%

1951-3 1.91% 3 0.39% 4 0.25% 5 -0.10% 6 2.45%

1955-3 1.03% 2 0.87% 3 0.00% 4 0.67% 5 2.57%

1959-3 1.29% 3 1.16% 1 0.35% 2 0.51% 3 3.31%

Avg 0.59% 0.53% 0.28% 0.41% 1.81%

1963-3 0.62% 3 -0.14% 4 0.05% 5 0.22% 1 0.75%

1967-3 -0.58% 2 -0.48% 3 -0.30% 4 -0.05% 5 -1.41%

1971-3 0.53% 1 1.09% 2 0.21% 3 -0.13% 4 1.69%

1975-3 0.84% 4 -0.44% 5 0.03% 1 2.00% 2 2.42%

1979-3 1.26% 2 -0.88% 3 -0.39% 4 -0.18% 5 -0.20%

Avg 0.53% -0.17% -0.08% 0.37% 0.65%

1983-3 -0.99% 2 0.33% 3 -0.64% 4 0.22% 5 -1.08%

1987-3 0.07% 5 -0.91% 1 -0.53% 2 -0.49% 3 -1.87%

1991-3 0.29% 3 -0.77% 4 0.13% 5 0.46% 1 0.10%

1995-3 0.57% 2 -0.35% 3 0.07% 4 -0.41% 5 -0.12%

1999-3 -0.07% 1 1.33% 2 -0.80% 3 -0.22% 4 0.25%

Avg -0.03% -0.07% -0.35% -0.09% -0.54%

2003-3 -0.31% 4 -1.60% 5 0.46% 1 0.05% 2 -1.41%

2007-3 0.44% 2 0.70% 3 -0.15% 4 -0.45% 5 0.54%

2011-3 0.08% 2 0.10% 3 -0.15% 4 0.07% 5 0.10%

2015-3 0.33% 5 0.09% 1 -0.49% 2 -1.03% 3 -1.10%

2019-3 2.00% 3 0.86% 4 -0.12% 5 0.85% 1 3.58%

Avg 0.51% 0.03% -0.09% -0.10% 0.34%

SPX summary for PY3 1931 – 2019

Averages 0.38% 0.23% 0.05% 0.26% 0.92%

% Winners 70% 57% 52% 61% 70%

MDD 12/29/1987 2.39% — 12/28/1931 2.00% — 12/31/2007 1.96%

SPX summary for all years 1928 – 2022

Averages 0.17% 0.21% 0.37% 0.16% 0.89%

% Winners 63% 60% 68% 62% 73%

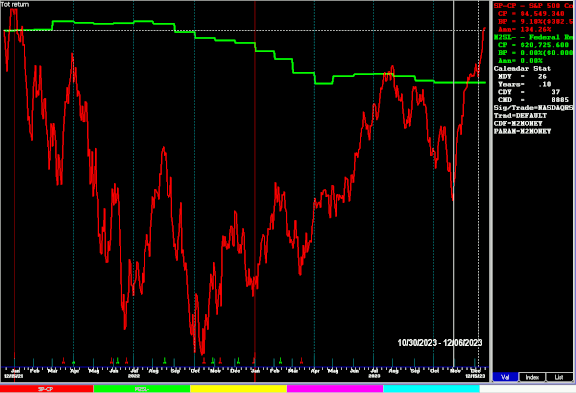

MDD 12/29/1987 2.39% — 12/31/1996 2.12% — 12/28/1931 2.00% Money supply (M2) and Interest RatesThe following charts were supplied by Gordon Harms.The first chart, made with FastTrack, covers the past 2 years showing the SPX in red and M2 money supply in green.Money supply has remained constant for several months.

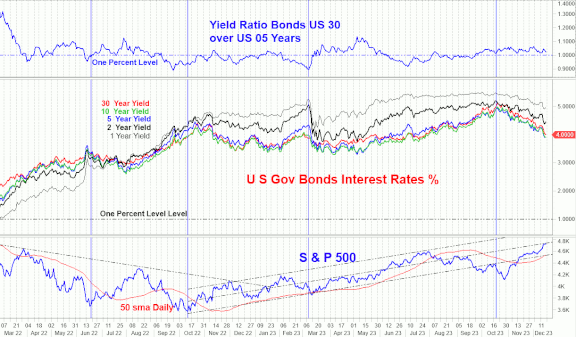

All the rates are inverted (shorter term maturities yield more than longer term maturities) relative to the 2 year; everything else is no longer inverted.The next chart covers the past 15 months showing the 30 year yield over the 5 year yield on top, The 1, 2, 5, 10 & 30 year treasury rates in the middle group and the SPX with a 50 day simple moving average on the bottom.