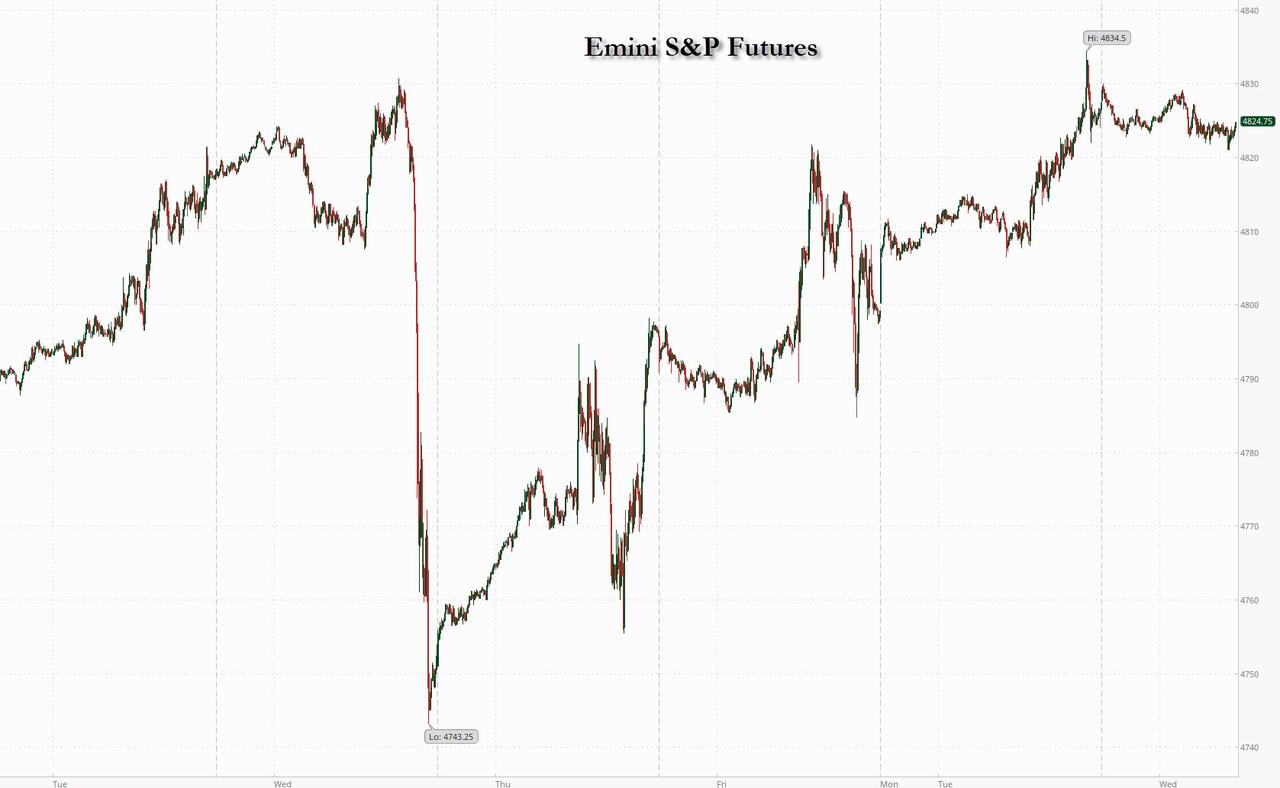

US futures were flat in muted trading following yesterday’s gain which pushed the S&P to within fractions of an all-time high amid trader hopes that the Federal Reserve is getting close to cutting interest rates, even if it means sparking another violent bout of inflation. As of 8:15 am, futures on the S&P 500 and the Nasdaq 100 indexes flirted between small gains and losses; after rising 0.4% on Tuesday, the S&P is heading for a seven-week winning streak and resides within 0.5% of the record high reached early last year. 10Y yields slumped to session lows around 3.842%, down 5 bps from Tuesday’s close, while Brent also dipped about $1, sliding below $80. In premarket trading, Coherus Biosciences rose 37% after the FDA approved its medication administered after chemotherapy to reduce infection risks. Cryptocurrency-related stocks also advanced as Bitcoin recouped some of Tuesday’s losses, and traded around $43,000 rebounding from Tuesday’s drop. Other major cryptocurrencies also gained. Here are some other notable premarket movers:

In premarket trading, Coherus Biosciences rose 37% after the FDA approved its medication administered after chemotherapy to reduce infection risks. Cryptocurrency-related stocks also advanced as Bitcoin recouped some of Tuesday’s losses, and traded around $43,000 rebounding from Tuesday’s drop. Other major cryptocurrencies also gained. Here are some other notable premarket movers:

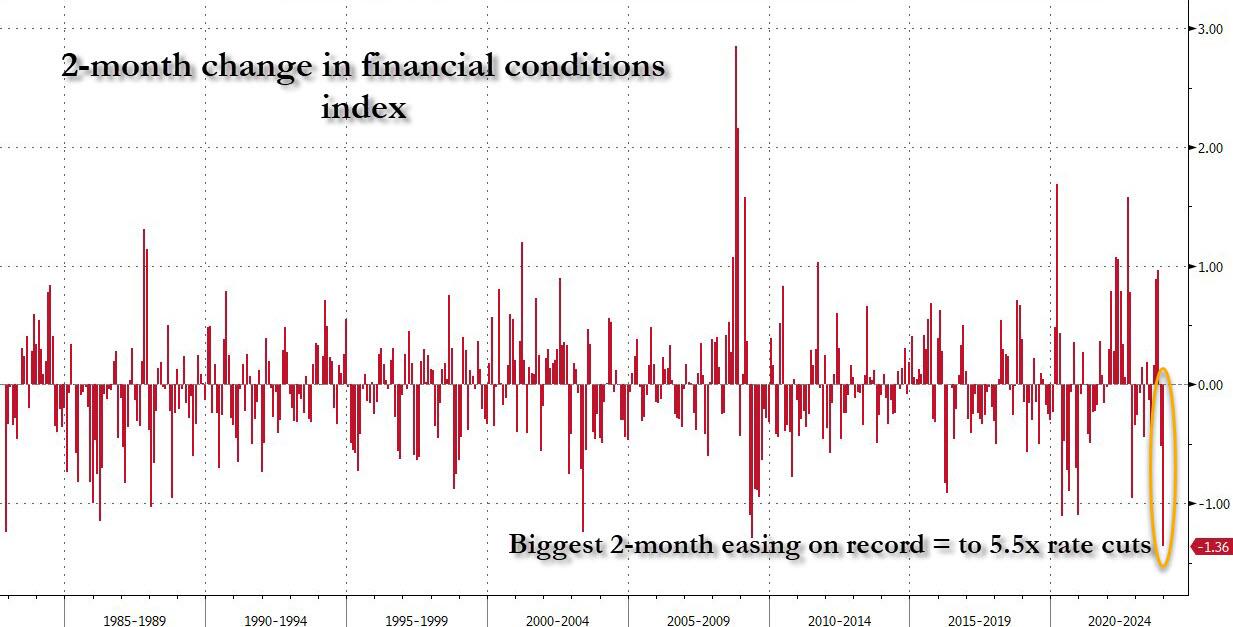

Following the Fed’s shocking dovish pivot on Dec 13, bets that the Fed could start cutting rates as soon as March have pushed US stocks to levels that most consider overbought but that has not stopped them from continuing to rise. This is due to historic move in financial conditions which have eased more in the past two months than ever before, including the launch of QE1, QE2, QE3 and so on. “S&P 500 buyers will certainly not back down before sending the index to a fresh high this week, or the next,” said Ipek Ozkardeskaya, a senior analyst at Swissquote Bank SA. Still, “the market optimism is overstretched. The Fed will probably cut rates but not at the speed that’s currently priced in. Once the Santa high fades, the hangover will hit,” she said.An index of manufacturing sentiment later on Wednesday and unemployment claims on Thursday might provide further clues about the economic and monetary-policy outlook.Meanwhile, shares in Europe posted a modest advance to the highest level since January 2022 as trading resumed after the Christmas holiday break. The Stoxx Europe 600 index is set to end the year with a gain of more than 12%, and also approaching all time highs, after rallying in the past two months amid speculation the ECB and Federal Reserve are moving closer to rate cuts. Trading volumes were light on Wednesday, with only three trading sessions left in 2023. Technology stocks were among the biggest gainers as Prosus NV rebounded from a slump triggered by a selloff in Tencent Holdings Ltd. Anglo American Plc climbed as much as 4.3% after a report that it’s selling a minority stake in Britain’s $9 billion Woodsmith fertilizer mine. On the downside, AP Moller-Maersk AS fell 4.7% after saying it’s preparing to resume shipping through the Red Sea. Container-shipping peer Hapag-Lloyd AG slumped 4.3%. The stocks had rallied on expectations that the disruption caused by attacks on Red Sea container traffic would allow companies to raise the prices. Here are some other notable movers:

“S&P 500 buyers will certainly not back down before sending the index to a fresh high this week, or the next,” said Ipek Ozkardeskaya, a senior analyst at Swissquote Bank SA. Still, “the market optimism is overstretched. The Fed will probably cut rates but not at the speed that’s currently priced in. Once the Santa high fades, the hangover will hit,” she said.An index of manufacturing sentiment later on Wednesday and unemployment claims on Thursday might provide further clues about the economic and monetary-policy outlook.Meanwhile, shares in Europe posted a modest advance to the highest level since January 2022 as trading resumed after the Christmas holiday break. The Stoxx Europe 600 index is set to end the year with a gain of more than 12%, and also approaching all time highs, after rallying in the past two months amid speculation the ECB and Federal Reserve are moving closer to rate cuts. Trading volumes were light on Wednesday, with only three trading sessions left in 2023. Technology stocks were among the biggest gainers as Prosus NV rebounded from a slump triggered by a selloff in Tencent Holdings Ltd. Anglo American Plc climbed as much as 4.3% after a report that it’s selling a minority stake in Britain’s $9 billion Woodsmith fertilizer mine. On the downside, AP Moller-Maersk AS fell 4.7% after saying it’s preparing to resume shipping through the Red Sea. Container-shipping peer Hapag-Lloyd AG slumped 4.3%. The stocks had rallied on expectations that the disruption caused by attacks on Red Sea container traffic would allow companies to raise the prices. Here are some other notable movers:

Asian stocks posted solid gains, rising 1.2% led by a rebound in mainland China where stocks reversed earlier losses, after data showed a quickening speed of growth in the country’s industrial profits, helped by favorable base effects. Japan’s Nikkei 225 index gained over 1%, hovering slightly below its previous high in July, after Bank of Japan board members discussed the potential timing of ending the negative rate policy during their meeting last week, with several members indicating they see no rush to make the move. The yen weakened and Japanese government bond yields fell after the release of the summary. Australia’s S&P/ASX 200 index rose to its highest since April 2022, fueled by gains in miners.in FX, the Bloomberg Dollar Spot Index was little changed while the yield on policy-sensitive two-year Treasuries fell one basis point to 4.34%. The yen fell as much as 0.3% against the dollar after one board member indicated it is appropriate for the central bank to continue monetary easing. Another said the BOJ can wait until after it sees the results of the spring wage negotiations in March to decide if it should raise rates. “Removal of negative interest rate policy in January is off the table” after the central bank took a cautious approach at the December meeting, said Shoki Omori, chief desk strategist at Mizuho Securities in Tokyo. The continuation of NIRP could maintain the rate differential with the US and weaken the yen against the dollar, Omori said.In rates, treasuries held small gains in early US trading, though 2-year notes sold at auction Tuesday remain slightly cheaper than the auction yield, which was lower than anticipated on strong demand and the biggest stop-through since June. Yields are lower by as much as 3bp on the day and still inside past week’s ranges; 10-year 3.87% vs last week’s low 3.827%, reached following downward revision to 3Q GDP. European yields are sharply lower on their first trading day since Dec. 22; German two-year yield fell four basis points to 1.94%, nearing March’s low. Activity remains muted with treasury futures volumes through 7am were less than half 20-day average levels. Supply cycle continues with $58BN in 5-year notes auction at 1pm. WI 5-year yield of 3.865% is lower than 5-year auction results since May and more than 50bp lower than November’s sale following past month’s collapse in yields unleashed by signals from Fed that no further rate hikes are likelyIn commodities, oil traded near its highest close in almost a month, with a new attack on shipping in the Red Sea underscoring why some vessels are avoiding the key route. Brent crude dipped 0.4% after rallying 2.5% on Tuesday when European markets were closed.Bitcoin recovered amid renewed speculation that the US securities regulator is getting close to approving an exchange-traded fund investing directly in the biggest token. Bitcoin advanced as much as 2.1% and traded around $43,000 as of 12:10 p.m. in London, rebounding from Tuesday’s drop. Other major cryptocurrencies also gained. Bitcoin Cash, one of the early offshoots of the original digital currency, rallied as much as 14% after investors piled into an investment vehicle tracking the token.Looking at today’s US economic calendar , we have the December Richmond Fed manufacturing index at 10am and December Dallas Fed services activity gauge at 10:30am. No Fed speakers are scheduled for remainder of year. Market Snapshot

Top Overnight News

US Event Calendar

More By This Author:China’s Spy Agencies Now Targeting The Country’s Economic Pessimists’Biggest Losers’, Bullion, & Black Gold All Bid On Boxing DayHow Bankers Are Exploiting The Fed’s Bailout Program At Your Expense