The selling to start 2024 helped cool an overheated market. The pullback will offer patient investors the opportunity to buy strong stocks at move attractive levels in the days and weeks ahead.The Nasdaq is back below its 21-day moving average, with the S&P 500 rapidly approaching that same key shorted-dated trendline. Stocks and indexes always come back down to key moving averages before they can restart their march higher.The recent red wave helped send the Nasdaq from some of its most overbought RSI levels in the last five years in late December to below neutral. Every investor should pay attention to how the Nasdaq and the S&P 500 interact with the 21-day, the 50-day, and the 200-day in January and throughout the year since they often prove to be lines in the sand the bulls attempt to defend.  Image Source: Zacks Investment ResearchThankfully, the dips might be bought up quickly as more investors big and small chase returns in 2024 as rates fall. The two highly-ranked tech stocks we look at today might slip in the days and weeks ahead. But their valuation levels are already strong, meaning any dip would make them more appealing given their improving earnings outlooks.Fiserv, Inc. (FI)Fiserv is one of the most important financial services companies in the U.S. that many people have never heard of. Fiserv operates in the background helping provide backend payment, processing, money transfer technology, and more used by tons of large financial institutions, banks, credit unions, fintech firms, enterprises, and beyond.

Image Source: Zacks Investment ResearchThankfully, the dips might be bought up quickly as more investors big and small chase returns in 2024 as rates fall. The two highly-ranked tech stocks we look at today might slip in the days and weeks ahead. But their valuation levels are already strong, meaning any dip would make them more appealing given their improving earnings outlooks.Fiserv, Inc. (FI)Fiserv is one of the most important financial services companies in the U.S. that many people have never heard of. Fiserv operates in the background helping provide backend payment, processing, money transfer technology, and more used by tons of large financial institutions, banks, credit unions, fintech firms, enterprises, and beyond.  Image Source: Zacks Investment ResearchFiserv offers account processing, digital banking solutions, card issuer processing, payments, e-commerce, merchant acquiring and processing, and much more. Fiserv’s core reportable segments include Merchant Acceptance, Financial Technology, and Payments and Network. FI expanded steadily for years until it ramped up its revenue and earnings growth via a major 2019 acquisition that greatly enhanced its reach to help Fiserv thrive in a rapidly changing payments and financial services landscape.Zacks estimates call for the company to post 8% revenue growth in FY23 and FY24 to reach nearly $20 billion. Better yet, its adjusted earnings are expected to climb by 15% and 14%, respectively over this stretch.FI currently lands a Zacks Rank #2 (Buy) based on its upward earnings revisions and roughly 70% of the brokerage recommendations we have are “Strong Buys” or “Buys,” with no sells.

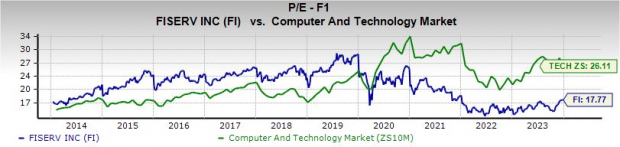

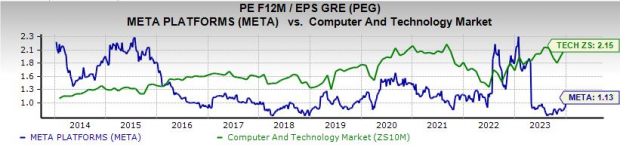

Image Source: Zacks Investment ResearchFiserv offers account processing, digital banking solutions, card issuer processing, payments, e-commerce, merchant acquiring and processing, and much more. Fiserv’s core reportable segments include Merchant Acceptance, Financial Technology, and Payments and Network. FI expanded steadily for years until it ramped up its revenue and earnings growth via a major 2019 acquisition that greatly enhanced its reach to help Fiserv thrive in a rapidly changing payments and financial services landscape.Zacks estimates call for the company to post 8% revenue growth in FY23 and FY24 to reach nearly $20 billion. Better yet, its adjusted earnings are expected to climb by 15% and 14%, respectively over this stretch.FI currently lands a Zacks Rank #2 (Buy) based on its upward earnings revisions and roughly 70% of the brokerage recommendations we have are “Strong Buys” or “Buys,” with no sells.  Image Source: Zacks Investment ResearchFiserv shares have soared 1,300% in the last 20 years vs. the Nasdaq’s 610%. FI has underperformed more recently, up 80% in the past five years compared to the tech-heavy index’s 120% climb.Fiserv has climbed 29% in the past 12 months and it hit new highs in the middle of December. The stock currently trades 10% below its average Zacks price target.Fiserv is back below its 21-day and possibly on a collision course with its 50-day as it slips from overbought in the middle of last month to below neutral. Plus, FI stock currently trades at a 35% discount to its 10-year highs and 32% below the Zacks tech sector at 17.8X forward earnings. Meta Platforms, Inc. (META)Meta might not scream value stock considering it has soared 170% in the last 12 months to crush the tech sector’s 50% run. Yet, the parent company of Facebook, Instagram, and WhatsApp trades at a 7% discount to the Zacks tech sector and 8% below its 10-year median a 24.2X forward earnings. Meta also trades 67% below its 10-year highs, and its PEG ratio, which factors in its earnings growth outlook, sits at 1.1 vs. the Tech’s 2.2 and Meta’s 2.3 highs.

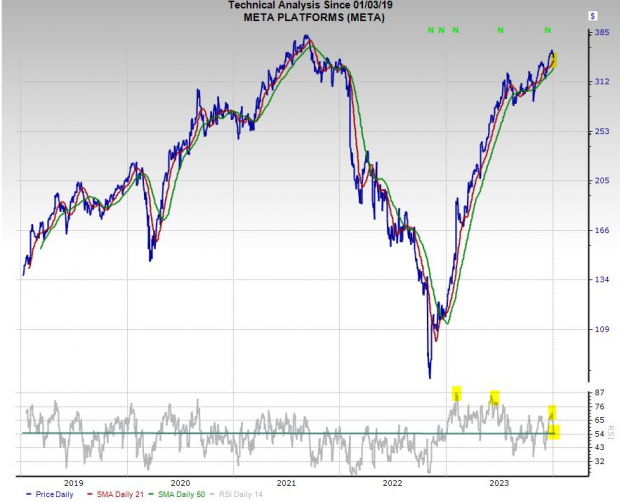

Image Source: Zacks Investment ResearchFiserv shares have soared 1,300% in the last 20 years vs. the Nasdaq’s 610%. FI has underperformed more recently, up 80% in the past five years compared to the tech-heavy index’s 120% climb.Fiserv has climbed 29% in the past 12 months and it hit new highs in the middle of December. The stock currently trades 10% below its average Zacks price target.Fiserv is back below its 21-day and possibly on a collision course with its 50-day as it slips from overbought in the middle of last month to below neutral. Plus, FI stock currently trades at a 35% discount to its 10-year highs and 32% below the Zacks tech sector at 17.8X forward earnings. Meta Platforms, Inc. (META)Meta might not scream value stock considering it has soared 170% in the last 12 months to crush the tech sector’s 50% run. Yet, the parent company of Facebook, Instagram, and WhatsApp trades at a 7% discount to the Zacks tech sector and 8% below its 10-year median a 24.2X forward earnings. Meta also trades 67% below its 10-year highs, and its PEG ratio, which factors in its earnings growth outlook, sits at 1.1 vs. the Tech’s 2.2 and Meta’s 2.3 highs.  Image Source: Zacks Investment ResearchMeta stock trades 12% below its average Zacks price target and roughly 10% below its 2021 highs. Meta is approaching its 21-day right now and sitting at neutral RSI levels after its recent dip.Meta, like Amazon (AMZN) and others, is focused on churning out profits. Meta is projected to grow its adjusted earnings by 46% in 2023 and another 23% next year on the back of 14% and 13%, respective revenue expansion. Meta’s earnings outlook has improved over the last 12 months and it has topped our EPS estimates by an average of 28% in the trailing four quarters.

Image Source: Zacks Investment ResearchMeta stock trades 12% below its average Zacks price target and roughly 10% below its 2021 highs. Meta is approaching its 21-day right now and sitting at neutral RSI levels after its recent dip.Meta, like Amazon (AMZN) and others, is focused on churning out profits. Meta is projected to grow its adjusted earnings by 46% in 2023 and another 23% next year on the back of 14% and 13%, respective revenue expansion. Meta’s earnings outlook has improved over the last 12 months and it has topped our EPS estimates by an average of 28% in the trailing four quarters. Image Source: Zacks Investment ResearchDespite concerns about slowing ad spending and the growing saturation of Facebook, Instagram, and WhatsApp, Meta grew its daily active user (people) base by 7% last quarter to a mind-blowing 3.14 billion. Meanwhile, its monthly active users popped 7% to 3.96 billion.The company’s various apps focused on different niches of social media and digital communication attract advertisers clamoring to reach the massive user base in a world where people are glued to their phones. All of this means that Mark Zuckerberg’s metaverse bet doesn’t have to pay off anytime soon—if ever. And Meta’s balance sheet remains robust. More By This Author:Finding The Best Value Stocks To Buy To Start 2024

Image Source: Zacks Investment ResearchDespite concerns about slowing ad spending and the growing saturation of Facebook, Instagram, and WhatsApp, Meta grew its daily active user (people) base by 7% last quarter to a mind-blowing 3.14 billion. Meanwhile, its monthly active users popped 7% to 3.96 billion.The company’s various apps focused on different niches of social media and digital communication attract advertisers clamoring to reach the massive user base in a world where people are glued to their phones. All of this means that Mark Zuckerberg’s metaverse bet doesn’t have to pay off anytime soon—if ever. And Meta’s balance sheet remains robust. More By This Author:Finding The Best Value Stocks To Buy To Start 2024

3 Top-Ranked Growth Tech Stocks To Buy In 2024

2 Top S&P 500 Stocks To Buy On The Dip For Big 2024 Gains