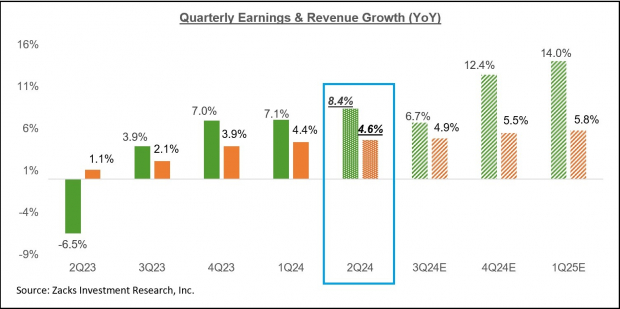

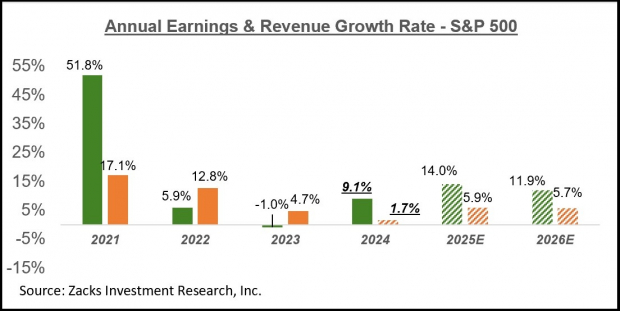

Image Source: PixabayWith the June-quarter reporting cycle taking center stage with reports from JPMorgan (JPM – Free Report) and the other major banks on Friday, July 12th, it is useful to take a big-picture view of where we have been in recent periods and what is expected in the coming quarters.We are highlighting three aspects of the overall earnings setup as we prepare to receive the coming quarterly releases.The first thing we would like all market participants to be mindful of is the steadily accelerating earnings growth trend.You can see this clearly in the chart below, which shows the year-over-year earnings and revenue growth for 2024 Q2 in the context of what we saw in the preceding four periods and what is currently expected for the following three periods.

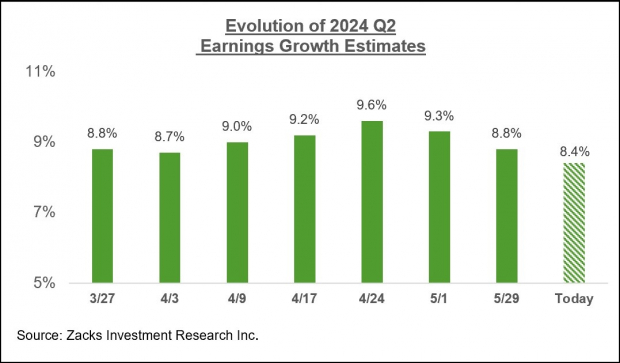

Image Source: PixabayWith the June-quarter reporting cycle taking center stage with reports from JPMorgan (JPM – Free Report) and the other major banks on Friday, July 12th, it is useful to take a big-picture view of where we have been in recent periods and what is expected in the coming quarters.We are highlighting three aspects of the overall earnings setup as we prepare to receive the coming quarterly releases.The first thing we would like all market participants to be mindful of is the steadily accelerating earnings growth trend.You can see this clearly in the chart below, which shows the year-over-year earnings and revenue growth for 2024 Q2 in the context of what we saw in the preceding four periods and what is currently expected for the following three periods. Image Source: Zacks Investment ResearchAs we have noted in this space before, the +8.4% earnings growth in 2024 Q2 is the highest growth pace in almost two years.The second thing we would like to flag here is the favorable development on the revisions front, with estimates for Q2 holding up far better than other recent periods. In the three-month period from the start of the quarter through June 30th, Q2 estimates for the S&P 500 index fell the least relative to comparable periods of other recent quarters.The chart below gives us a good visual sense of this favorable revisions trend.

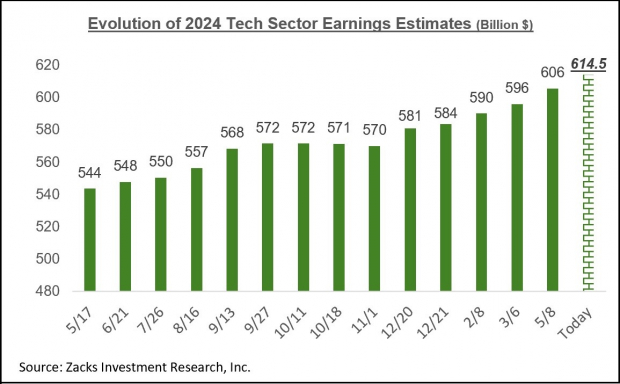

Image Source: Zacks Investment ResearchAs we have noted in this space before, the +8.4% earnings growth in 2024 Q2 is the highest growth pace in almost two years.The second thing we would like to flag here is the favorable development on the revisions front, with estimates for Q2 holding up far better than other recent periods. In the three-month period from the start of the quarter through June 30th, Q2 estimates for the S&P 500 index fell the least relative to comparable periods of other recent quarters.The chart below gives us a good visual sense of this favorable revisions trend. Image Source: Zacks Investment ResearchThe Energy sector was a notable contributor to the positive revisions trend earlier in the quarter. But as the underlying commodity prices lost ground later in the period, analysts also started reflecting that in their estimates. Aside from the Energy sector, estimates increased in the Transportation, Utilities, Tech, Autos, and Consumer Discretionary sectors.On the negative side, estimates have been cut for 10 of the 16 Zacks sectors, with notable declines at the Industrial Products, Aerospace, Consumer Staples, Conglomerates, Construction, and others.The third key feature to keep in mind is the robust earnings outlook for the Tech sector in general and the ‘Magnificent 7 Stocks’ in particular. The stock market leadership of the Tech and Mag 7 stocks reflects this positive earnings backdrop for the group.The Zacks Tech sector has an outsized weight in the S&P 500 index, accounting for 41.1% of the index’s market capitalization and on track to bring 29.9% of the index’s total earnings for the coming four-quarter period. As such, the Tech sector is unlike any other sector, and trends in the sector significantly impact the aggregate picture.As noted earlier, the Tech sector is one of the six sectors that enjoyed a favorable revisions trend in 2024 Q2, a trend that has also been in place for the last few quarters.We are also seeing a favorable revisions trend for the back half of the year, as you can see from the chart below that shows the evolution of aggregate Tech sector earnings over the past year.

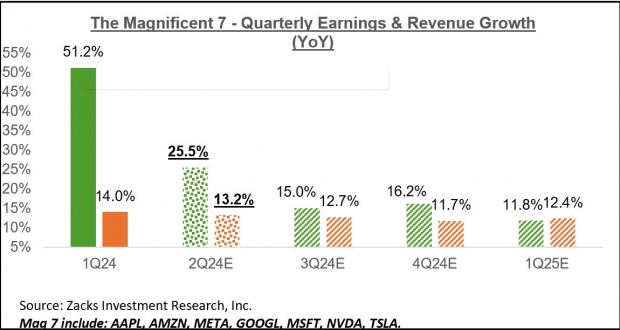

Image Source: Zacks Investment ResearchThe Energy sector was a notable contributor to the positive revisions trend earlier in the quarter. But as the underlying commodity prices lost ground later in the period, analysts also started reflecting that in their estimates. Aside from the Energy sector, estimates increased in the Transportation, Utilities, Tech, Autos, and Consumer Discretionary sectors.On the negative side, estimates have been cut for 10 of the 16 Zacks sectors, with notable declines at the Industrial Products, Aerospace, Consumer Staples, Conglomerates, Construction, and others.The third key feature to keep in mind is the robust earnings outlook for the Tech sector in general and the ‘Magnificent 7 Stocks’ in particular. The stock market leadership of the Tech and Mag 7 stocks reflects this positive earnings backdrop for the group.The Zacks Tech sector has an outsized weight in the S&P 500 index, accounting for 41.1% of the index’s market capitalization and on track to bring 29.9% of the index’s total earnings for the coming four-quarter period. As such, the Tech sector is unlike any other sector, and trends in the sector significantly impact the aggregate picture.As noted earlier, the Tech sector is one of the six sectors that enjoyed a favorable revisions trend in 2024 Q2, a trend that has also been in place for the last few quarters.We are also seeing a favorable revisions trend for the back half of the year, as you can see from the chart below that shows the evolution of aggregate Tech sector earnings over the past year. Image Source: Zacks Investment ResearchPlease note that the Zacks Tech sector differs slightly from the Standard & Poor’s official GICs, as it is essentially a blend of the S&P’s Information Tech and Communication Services sectors.As we have been flagging all along, the Tech sector is firmly in growth mode now, with 2024 Q2 as the fourth consecutive quarter of double-digit earnings growth. Total Tech sector earnings are expected to be up +15.7% from the same period last year on +9.6% higher revenues. Had it not been for the Tech sector’s strong growth, Q2 earnings for the rest of the index would be up only +4.8% (vs. +8.4% otherwise).For the Mag 7 stocks, Q2 earnings are expected to be up +25.5% on +13.2% higher revenues, as the chart below shows.

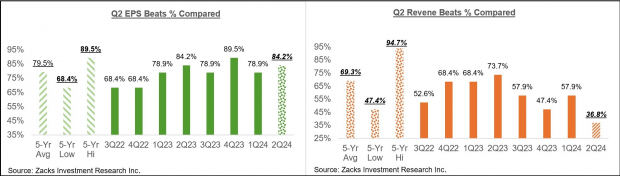

Image Source: Zacks Investment ResearchPlease note that the Zacks Tech sector differs slightly from the Standard & Poor’s official GICs, as it is essentially a blend of the S&P’s Information Tech and Communication Services sectors.As we have been flagging all along, the Tech sector is firmly in growth mode now, with 2024 Q2 as the fourth consecutive quarter of double-digit earnings growth. Total Tech sector earnings are expected to be up +15.7% from the same period last year on +9.6% higher revenues. Had it not been for the Tech sector’s strong growth, Q2 earnings for the rest of the index would be up only +4.8% (vs. +8.4% otherwise).For the Mag 7 stocks, Q2 earnings are expected to be up +25.5% on +13.2% higher revenues, as the chart below shows. Image Source: Zacks Investment ResearchQ2 Earnings Season ScorecardWe noted earlier that the July 12th quarterly report from JPMorgan and the other big banks will put the spotlight on the Q2 earnings season. But the banks aren’t the first to report the Q2 results, as the 19 S&P 500 members that have been reporting results in recent days for their respective fiscal quarters ending in May form part of our overall Q2 tally. A number of the companies in this sample of 19 index members are bellwethers like FedEx (FDX – Free Report), Nike (NKE – Free Report), and others.For the 19 S&P 500 members that have reported their fiscal May quarter results already, total earnings are up +25.7% from the same period last year on +4.4% higher revenues, with 84.2% beating EPS estimates and only 36.8% able to beat revenue estimates.This is too small a sample of results to draw any conclusions from, but the comparisons charts below put the earnings and revenue beats percentages for these companies in a historical context.

Image Source: Zacks Investment ResearchQ2 Earnings Season ScorecardWe noted earlier that the July 12th quarterly report from JPMorgan and the other big banks will put the spotlight on the Q2 earnings season. But the banks aren’t the first to report the Q2 results, as the 19 S&P 500 members that have been reporting results in recent days for their respective fiscal quarters ending in May form part of our overall Q2 tally. A number of the companies in this sample of 19 index members are bellwethers like FedEx (FDX – Free Report), Nike (NKE – Free Report), and others.For the 19 S&P 500 members that have reported their fiscal May quarter results already, total earnings are up +25.7% from the same period last year on +4.4% higher revenues, with 84.2% beating EPS estimates and only 36.8% able to beat revenue estimates.This is too small a sample of results to draw any conclusions from, but the comparisons charts below put the earnings and revenue beats percentages for these companies in a historical context. Image Source: Zacks Investment ResearchThis is by no means a representative sample of results at this early stage, but we will be keenly looking at how the revenue beats percentage evolves in the days ahead, as we are off to a rough start on that count.The Annual Earnings PictureTotal 2024 S&P 500 earnings are expected to be up +9.1% on +1.7% revenue growth. The expected revenue growth pace improves to +3.9% once Finance is excluded from the aggregate data, with the index-level aggregate earnings growth for the year remaining unchanged at +9% on an ex-Finance basis.

Image Source: Zacks Investment ResearchThis is by no means a representative sample of results at this early stage, but we will be keenly looking at how the revenue beats percentage evolves in the days ahead, as we are off to a rough start on that count.The Annual Earnings PictureTotal 2024 S&P 500 earnings are expected to be up +9.1% on +1.7% revenue growth. The expected revenue growth pace improves to +3.9% once Finance is excluded from the aggregate data, with the index-level aggregate earnings growth for the year remaining unchanged at +9% on an ex-Finance basis. Image Source: Zacks Investment ResearchMore By This Author:The Setup For The Q2 Earnings Season Gets Underway

Image Source: Zacks Investment ResearchMore By This Author:The Setup For The Q2 Earnings Season Gets Underway

Q2 Earnings Growth Forecasted To Hit Two-Year High

Top Research Reports For NVIDIA, Amazon.com & UnitedHealth