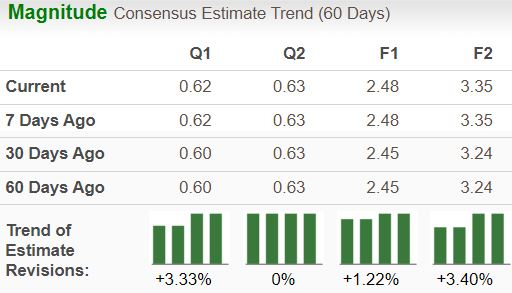

Tesla (TSLA – Free Report) is slated to release second-quarter 2024 results on Jul 23, after market close. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings and revenues is pegged at 62 cents per share and $25.1 billion, respectively.The earnings estimate for the to-be-reported quarter has been revised upward by 2 cents over the past 30 days. The bottom-line projection, however, indicates a year-over-year decline of 32%. The Zacks Consensus Estimate for quarterly revenues suggests a modest year-over-year increase of 0.8%. Image Source: Zacks Investment ResearchFor the current year, the Zacks Consensus Estimate for TSLA’s revenues is pegged at $98 billion, implying a rise of 1.7% year over year. The consensus mark for 2024 EPS is pegged at $2.48, implying a contraction of around 20.5% on a year-over-year basis.In the trailing four quarters, this electric vehicle (EV) behemoth surpassed EPS estimates just once and missed on the other occasions, with the average negative earnings surprise being -1.55%.

Image Source: Zacks Investment ResearchFor the current year, the Zacks Consensus Estimate for TSLA’s revenues is pegged at $98 billion, implying a rise of 1.7% year over year. The consensus mark for 2024 EPS is pegged at $2.48, implying a contraction of around 20.5% on a year-over-year basis.In the trailing four quarters, this electric vehicle (EV) behemoth surpassed EPS estimates just once and missed on the other occasions, with the average negative earnings surprise being -1.55%.

Tesla, Inc. Price and EPS Surprise Tesla, Inc. price-eps-surprise | Tesla, Inc. Quote

Tesla, Inc. price-eps-surprise | Tesla, Inc. Quote

Earnings Whispers for Q2Our proven model does not conclusively predict an earnings beat for Tesla. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. That’s not the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.TSLA has an Earnings ESP of -4.13% and a Zacks Rank #3.

Factors Shaping TSLA’s Q2 ResultsTesla produced 410,831 vehicles (386,576 Model 3/Y and 24,255 Model S/X) in the three months ended June. It delivered 443,956 cars (422,405 Model 3/Y and 21,551 other models) worldwide in the second quarter, missing the Zacks Consensus Estimate of 469,599 vehicles. The reported deliveries were down roughly 5% year over year but increased 15% from the first quarter of 2024.The Zacks Consensus Estimate for TSLA’s second-quarter revenues from automotive sales is pegged at $20.6 billion, implying an uptick from $20.4 billion recorded in the year-ago period. Tesla resorted to price cuts and incentives to spur vehicle sales. While that might have helped stimulate demand in the second quarter, it is also likely to cause margin compression. The consensus mark for gross profit from the automotive unit is $3.75 billion, implying a 23.4% decline from the second quarter of 2023.While automotive profits are expected to contract on a yearly basis in the quarter to be reported, Tesla has been benefiting from increasing energy generation and storage revenues, thanks to the positive reception of Megapack and Powerwall products. The Zacks Consensus Estimate for revenues from the Energy Generation/Storage segment is pegged at $2.32 billion, suggesting growth of 54.6% on a yearly basis. Gross profit from the segment is expected to be $598 million, suggesting growth of more than 100% from the second quarter of 2023.The consensus mark for TSLA’s revenues from the Services/Others unit is pegged at $2.43 billion, up from $2.15 billion recorded in the year-ago period. The company’s supercharging network business is primarily expected to boost the segment’s revenues. Most auto giants like General Motors (GM – Free Report), Ford (F – Free Report), and Stellantis (STLA – Free Report), among others, are adopting Tesla’s NACS charging port standard.

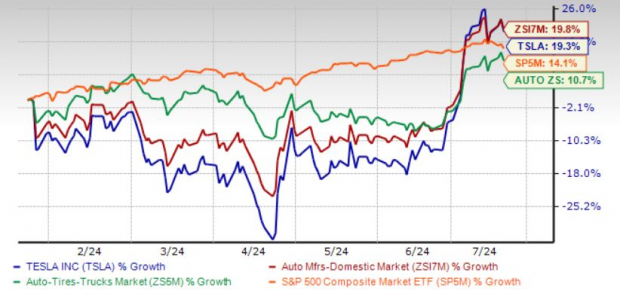

Price Performance & ValuationOver the past six months, shares of Tesla have moved up around 19%, outperforming the sector and the S&P 500 and almost matching the industry’s growth.

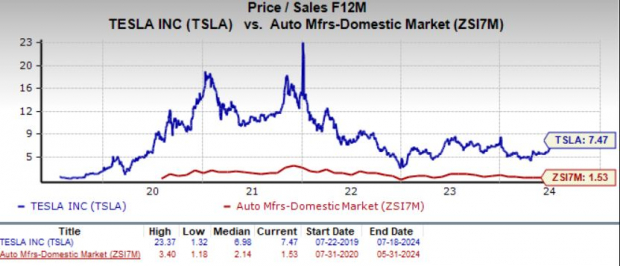

6-Month Price Comparison Image Source: Zacks Investment ResearchFrom a valuation perspective, Tesla looks highly overvalued. Going by its price/sales ratio, the company is trading at a forward sales multiple of 7.47, higher than its median of 6.98 over the last five years. It is also trading at a huge premium compared to the industry’s 1.53. The company has a Value Score of F.

Image Source: Zacks Investment ResearchFrom a valuation perspective, Tesla looks highly overvalued. Going by its price/sales ratio, the company is trading at a forward sales multiple of 7.47, higher than its median of 6.98 over the last five years. It is also trading at a huge premium compared to the industry’s 1.53. The company has a Value Score of F. Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Things Investors Should NoteOf late, shrinking automotive margins amid aggressive price cuts and discounts have been plaguing Tesla. The company expects its vehicle volume growth rate for 2024 to be noticeably lower than in 2023 amid a cooling EV market. With competition intensifying in the EV space, Tesla’s focus on autonomous driving and artificial intelligence (AI) is expected to be a game changer.Tesla aims to launch affordable vehicles, transition into an AI company and is banking on its robotaxi venture. The successful introduction of its Full Self Driving software in China amid stiff competition marks a significant win. Additionally, TSLA’s Energy Generation and Storage business is thriving. High liquidity and low leverage provide Tesla with the financial flexibility to tap growth opportunities. As such, the long-term prospects of the company appear promising.

Is Now the Right Time to Buy TSLA?Investing in Tesla now is essentially a bet on its driverless software and AI potential. However, the company’s history of missed deadlines and the significant engineering and regulatory challenges of autonomous vehicle development warrant caution. Earlier this month, Tesla postponed its highly anticipated robotaxi event from Aug 8 to October. Investors should closely monitor Tesla’s upcoming earnings report on Jul 23, where more details about the robotaxi project are expected. Given the company’s currently stretched valuation, it will be prudent for investors to wait for more clarity and stability before taking a position in the stock.More By This Author:Top Stocks To Buy For Growth As Earnings Approach Don’t Overlook These 2 Top-Rated Stocks After Earnings3 Buy Rated Stocks To Consider After Earnings