Image Source: HomeDepot.comEarnings season continues to wind down, with the bulk of S&P 500 companies already revealing quarterly results. And recently, we heard from home improvement retailer Home Depot (HD – Free Report), posted results that caused bullish activity.With peer Lowe’s (LOW – Free Report) on deck to reveal its quarterly results on August 20th, let’s take a closer look at what investors can expect.

Image Source: HomeDepot.comEarnings season continues to wind down, with the bulk of S&P 500 companies already revealing quarterly results. And recently, we heard from home improvement retailer Home Depot (HD – Free Report), posted results that caused bullish activity.With peer Lowe’s (LOW – Free Report) on deck to reveal its quarterly results on August 20th, let’s take a closer look at what investors can expect.

Home Depot Maintains Bright Outlook

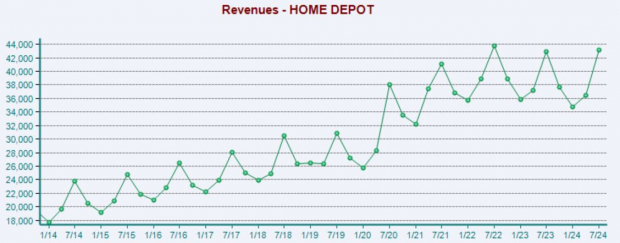

HD posted a 2.9% beat relative to the Zacks Consensus EPS estimate and reported sales 1.4% ahead of the consensus. Earnings were down marginally from the year-ago period, whereas sales were up a slight 0.6%.As shown below, the company’s sales growth has flattened post-pandemic. Pulled-forward demand surrounding home improvement retailers during COVID initially benefited the company significantly but has reversed course, with consumers now taking on much fewer projects.In other words, consumers rapidly upgraded their homes (porches, fences) during the period, and the trend has decelerated sharply.

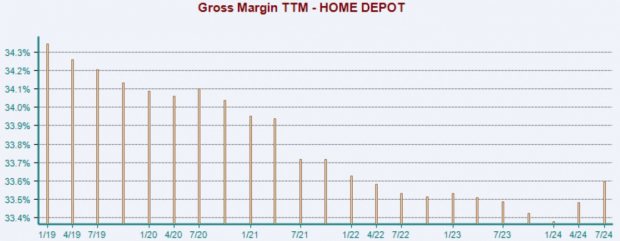

Image Source: Zacks Investment ResearchTed Decker, CEO, confirmed the trend but remained positive, stating, ‘The underlying long-term fundamentals supporting home improvement demand are strong,’He continued, ‘During the quarter, higher interest rates and greater macro-economic uncertainty pressured consumer demand more broadly, resulting in weaker spend across home improvement projects.’Margin pressures have also negatively impacted profitability, but the tide has begun to change over recent periods, as shown below. Please note that the chart is on a trailing twelve-month basis.

Image Source: Zacks Investment Research

Lowe’s Growth Expected to Cool

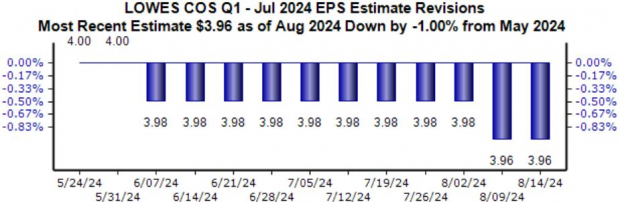

Earnings expectations for LOW have moved modestly lower over the recent months but remained stable following HD’s quarterly release, a key development. The company is expected to witness a growth cooldown, with earnings expected to be down 13% on 4% lower sales.

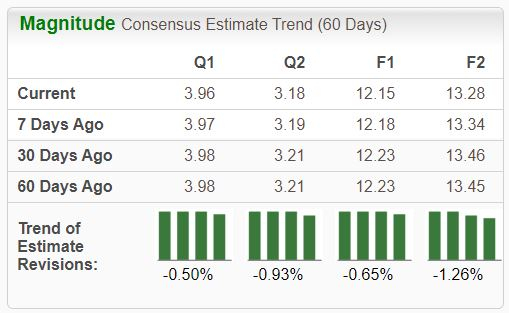

Image Source: Zacks Investment ResearchSimilar to HD, Lowe’s has been facing a demand slowdown, with comparable store sales falling 4% year-over-year throughout its latest period amid a decline in big-ticket discretionary items. Given the read from HD, it’s reasonable to expect that the company continued to experience a slowdown in big-ticket items throughout the period.In addition, it’s worth noting that LOW is currently a Zacks Rank #4 (Sell), with earnings expectations shifting lower across the board over recent months. Investors should stay on the sidelines until positive earnings estimate revisions hit the tape, which would likely be caused by favorable guidance and better-than-expected quarterly results.

Image Source: Zacks Investment Research

Putting Everything Together

Home improvement titan Home Depot recently delivered its quarterly results, with shares seeing a slightly positive reaction post-earnings. There weren’t any meaningful spooks in the release, though the slowdown among big-ticket discretionary items remains a thorn in the company’s side.We’ll likely see a similar read from Lowe’s in its upcoming release on August 20th, as the company has also faced a slowdown in big-ticket spending. Lowe’s expectations allude to a slowdown, with both earnings and revenues expected to be lower Y/Y.More By This Author:3 Buy Rated Finance Stocks Flashing Relative Strength: HRTG, ERIE, EZPW

2 Companies Actually Benefiting From AI: Palantir, Meta Platforms

3 Companies Unlocking Higher Profits: DECK, KMB, SKX