Image Source: Pixabay

Image Source: Pixabay

The Q2 earnings season has effectively come to an end, with results from more than 95% of S&P 500 members already out, with even most of the major Retail sector results known by now. That said, this week’s line-up of quarterly results from more than 140 companies, including 15 from S&P 500 members, includes quarterly results from the only Magnificent 7 member yet to report results, Nvidia (NVDA – Free Report).Other notable companies reporting results this week include Salesforce (CRM – Free Report), Lululemon (LULU – Free Report), Best Buy (BBY – Free Report), and others.Nvidia has established itself as a true leader of the coming artificial intelligence (AI) economy, with the company’s chips as the only game in town when it comes to running the highly complex and demanding computations. This leadership has allowed Nvidia to consistently come out with beat-and-raise quarterly reports in recent quarters.We will see if the company can maintain this operating momentum when it reports results after the market’s close on Wednesday, August 28th. Estimates for the period have essentially remained unchanged in recent weeks, which is unusual relative to what we have been seeing in other recent quarters.Nvidia is expected to bring in $0.63 in EPS on $28.2 billion in revenues, representing year-over-year gains of +133.3% and +109%, respectively. You can see the long-term Nvidia revisions trend in the below Price, Consensus & Surprise chart. Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Nvidia shares were hit hard in the market’s recent down draft, but have effectively recouped most of those losses. The stock has more than doubled this year and handily outperformed the Zacks Tech sector, the broader market, and the Mag 7 stocks, as the chart below shows. Image Source: Zacks Investment ResearchThe biggest driver of the stock’s performance from here onwards will be management guidance for the current and upcoming quarters, as well as the market’s assessment of the company’s ability to ramp up production of the Blackwell chips. There have been speculations in the market that Nvidia is faced with production snags that can delay the product’s delivery schedule.With the stock up more than +150% this year alone, most investors will assume that valuation must be really stretched already. The actual ground reality is not that simple.Nvidia shares are currently trading at 40.2X forward 12-month EPS estimates. This is almost double the comparable multiple for the S&P 500 index of 21.5X. Over the last five years, Nvidia shares have traded as high as 106.3X forward 12-month estimates, as low as 26.8X, and have a 5-year median of 50.7X.Another way to look at Nvidia’s valuation is to look at the magnitude of the premium the stock is currently enjoying relative to where that premium or discount has historically been.Nvidia’s current forward 12-month P/E multiple is 187% of the S&P 500 multiple. Over the last five years, the stock’s multiple has been as high as 569% and as low as 134%, with a median over this period of 248%.In other words, the stock isn’t cheap, but it has traded at higher multiples over its history. Prediction is very difficult, particularly if it’s about the future, as someone wise once opined. Predictions for Nvidia shares require how sustainable the company’s competitive advantages are in the coming AI revolution, not to mention whether the ongoing all-around AI optimism has a solid foundation.Nvidia aside, the earnings focus lately has been on the Retail sector. To that end, we will be getting results this week from Lululemon, Best Buy, Dollar General, and a few other retailers.With respect to the Retail sector 2024 Q2 earnings season scorecard, we now have results from 30 of the 36 retailers in the S&P 500 index. Please note that these 30 retailers account for 97.3% of the sector’s market capitalization in the S&P 500 index.Regular readers know that Zacks has a dedicated stand-alone economic sector for the retail space, which is unlike the placement of the space in the Consumer Staples and Consumer Discretionary sectors in the Standard & Poor’s standard industry classification.The Zacks Retail sector includes not only Walmart, Target, and other traditional retailers but also online vendors like Amazon and restaurant players.Total Q2 earnings for these 30 retailers that have reported are up +17.3% from the same period last year on +4.8% higher revenues, with 63.3% beating EPS estimates and only 46.7% beating revenue estimates.The comparison charts below put the Q2 beats percentages for these retailers in a historical context.

Image Source: Zacks Investment ResearchThe biggest driver of the stock’s performance from here onwards will be management guidance for the current and upcoming quarters, as well as the market’s assessment of the company’s ability to ramp up production of the Blackwell chips. There have been speculations in the market that Nvidia is faced with production snags that can delay the product’s delivery schedule.With the stock up more than +150% this year alone, most investors will assume that valuation must be really stretched already. The actual ground reality is not that simple.Nvidia shares are currently trading at 40.2X forward 12-month EPS estimates. This is almost double the comparable multiple for the S&P 500 index of 21.5X. Over the last five years, Nvidia shares have traded as high as 106.3X forward 12-month estimates, as low as 26.8X, and have a 5-year median of 50.7X.Another way to look at Nvidia’s valuation is to look at the magnitude of the premium the stock is currently enjoying relative to where that premium or discount has historically been.Nvidia’s current forward 12-month P/E multiple is 187% of the S&P 500 multiple. Over the last five years, the stock’s multiple has been as high as 569% and as low as 134%, with a median over this period of 248%.In other words, the stock isn’t cheap, but it has traded at higher multiples over its history. Prediction is very difficult, particularly if it’s about the future, as someone wise once opined. Predictions for Nvidia shares require how sustainable the company’s competitive advantages are in the coming AI revolution, not to mention whether the ongoing all-around AI optimism has a solid foundation.Nvidia aside, the earnings focus lately has been on the Retail sector. To that end, we will be getting results this week from Lululemon, Best Buy, Dollar General, and a few other retailers.With respect to the Retail sector 2024 Q2 earnings season scorecard, we now have results from 30 of the 36 retailers in the S&P 500 index. Please note that these 30 retailers account for 97.3% of the sector’s market capitalization in the S&P 500 index.Regular readers know that Zacks has a dedicated stand-alone economic sector for the retail space, which is unlike the placement of the space in the Consumer Staples and Consumer Discretionary sectors in the Standard & Poor’s standard industry classification.The Zacks Retail sector includes not only Walmart, Target, and other traditional retailers but also online vendors like Amazon and restaurant players.Total Q2 earnings for these 30 retailers that have reported are up +17.3% from the same period last year on +4.8% higher revenues, with 63.3% beating EPS estimates and only 46.7% beating revenue estimates.The comparison charts below put the Q2 beats percentages for these retailers in a historical context. Image Source: Zacks Investment ResearchAs you can see above, the Retail sector companies have struggled with beating EPS and revenue estimates in Q2. In fact, the Q2 revenue beats percentages for these players is the low over the preceding 20 quarters (5 years), and the EPS beats percentage isn’t that far from the low-point either.With respect to the elevated earnings rate at this stage, we like to show the group’s performance with and without Amazon, whose results are among the 26 companies that have reported already. As we know, Amazon’s Q2 earnings were up +99.8% on +10.1% higher revenues, as it beat on EPS but missed top-line expectations.As we all know, the digital and brick-and-mortar operators have been converging for some time now. Amazon is now a decent-sized brick-and-mortar operator after Whole Foods, and Walmart is a growing online vendor.The two comparison charts below show the Q2 earnings and revenue growth relative to other recent periods, both with Amazon’s results (left side chart) and without Amazon’s numbers (right side chart).

Image Source: Zacks Investment ResearchAs you can see above, the Retail sector companies have struggled with beating EPS and revenue estimates in Q2. In fact, the Q2 revenue beats percentages for these players is the low over the preceding 20 quarters (5 years), and the EPS beats percentage isn’t that far from the low-point either.With respect to the elevated earnings rate at this stage, we like to show the group’s performance with and without Amazon, whose results are among the 26 companies that have reported already. As we know, Amazon’s Q2 earnings were up +99.8% on +10.1% higher revenues, as it beat on EPS but missed top-line expectations.As we all know, the digital and brick-and-mortar operators have been converging for some time now. Amazon is now a decent-sized brick-and-mortar operator after Whole Foods, and Walmart is a growing online vendor.The two comparison charts below show the Q2 earnings and revenue growth relative to other recent periods, both with Amazon’s results (left side chart) and without Amazon’s numbers (right side chart). Image Source: Zacks Investment ResearchAs noted earlier, we have started seeing signs of stress at the lower-end of income distribution, and one can intuitively project moderation in consumer spending as the economy further slows down under the weight of tighter monetary conditions. Inflation may be down from the multi-decade highs of a few quarters back, but it still remains a headwind, particularly for the lower end of income distribution. That said, the labor market remains very strong, with wages still going up.

Image Source: Zacks Investment ResearchAs noted earlier, we have started seeing signs of stress at the lower-end of income distribution, and one can intuitively project moderation in consumer spending as the economy further slows down under the weight of tighter monetary conditions. Inflation may be down from the multi-decade highs of a few quarters back, but it still remains a headwind, particularly for the lower end of income distribution. That said, the labor market remains very strong, with wages still going up.

Earnings Season Scorecard and This Week’s Earnings Reports

Through all the results that came out on Friday, August 23rd, we have seen Q2 results from 478 S&P 500 members, or 95.6% of the index’s membership. Total earnings for these index members are up +8% from the same period last year on +5.1% higher revenues, with 79.9% beating EPS estimates and only 60.3% able to beat revenue estimates.As noted earlier, we have over 140 companies on deck to report Q2 results this week, including 15 S&P 500 members. The notable companies on deck to report results this week, besides the aforementioned Nvidia, include Salesforce, Lululemon, Best Buy, Dollar General, and others.The comparisons charts below put the earnings and revenue beats percentages for these companies in a historical context. Image Source: Zacks Investment ResearchThe one notable feature of the above comparison charts is the very low level of Q2 revenue beats percentage. In fact, the Q2 revenue beats percentage of 60.3% is a new low for this group of index members over the preceding 20-quarter period (5 years).Revenue beats have been low from the start of the reporting cycle, a trend that will carry through to the end of the earnings season.The comparison charts below put the Q2 earnings and revenue growth rates for these companies in a historical context.

Image Source: Zacks Investment ResearchThe one notable feature of the above comparison charts is the very low level of Q2 revenue beats percentage. In fact, the Q2 revenue beats percentage of 60.3% is a new low for this group of index members over the preceding 20-quarter period (5 years).Revenue beats have been low from the start of the reporting cycle, a trend that will carry through to the end of the earnings season.The comparison charts below put the Q2 earnings and revenue growth rates for these companies in a historical context. Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

The Earnings Big Picture

Looking at Q2 as a whole, combining the actual results that have come out already with estimates for the few still-to-come companies, total S&P 500 earnings are expected to be up +9.6% from the same period last year on +5.4% higher revenues.This is the highest earnings growth pace in the last eight quarters since the +10% in 2022 Q1. The Q2 aggregate earnings total is on track to be a new all-time quarterly record, as the chart below shows. Image Source: Zacks Investment ResearchThe chart below shows the year-over-year earnings and revenue growth for 2024 Q2 in the context of what we saw in the preceding four periods and what is currently expected for the following three periods.

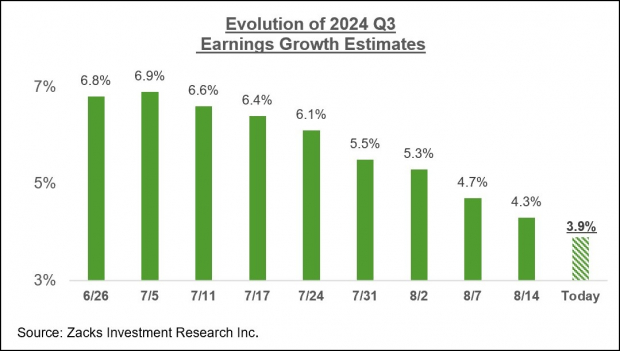

Image Source: Zacks Investment ResearchThe chart below shows the year-over-year earnings and revenue growth for 2024 Q2 in the context of what we saw in the preceding four periods and what is currently expected for the following three periods. Image Source: Zacks Investment ResearchFor the current period (2024 Q3), total S&P 500 earnings are expected to be up +3.9% from the same period last year on +4.6% higher revenues.Please note that estimates for Q3 have been steadily coming down, with the current +3.9% earnings growth rate down from +6.9% in early July, as the chart below shows.

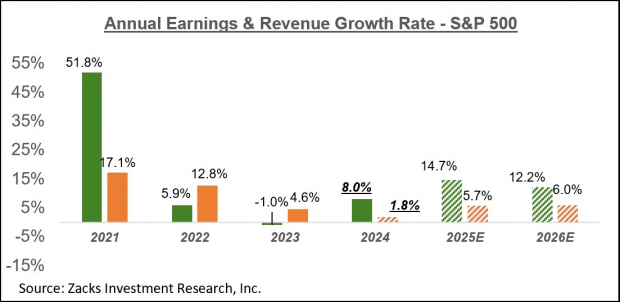

Image Source: Zacks Investment ResearchFor the current period (2024 Q3), total S&P 500 earnings are expected to be up +3.9% from the same period last year on +4.6% higher revenues.Please note that estimates for Q3 have been steadily coming down, with the current +3.9% earnings growth rate down from +6.9% in early July, as the chart below shows. Image Source: Zacks Investment ResearchThis is a bigger cut to estimates relative to what we saw in the comparable periods for the preceding two quarters. The negative revisions trend is broad-based, with estimates for 14 of the 16 Zacks sectors getting cut since the quarter began. The biggest cuts have been to the Transportation, Business Services, Energy, Aerospace, and Basic Materials sectors. On the positive side, estimates for the Tech sector are increasing, while the same for the Finance sector are only marginally higher relative to where we started in early July.Looking at earnings expectations on an annual basis, total 2024 S&P 500 earnings are expected to be up +8% on +1.8% revenue growth. Excluding the Energy sector drag, whose earnings are now expected to be down -11.8% in 2024, total earnings for the rest of the index would be up +9.6%.The expected 2024 revenue growth pace improves to +4.2% once Finance is excluded from the aggregate data, with the index-level aggregate earnings growth for the year declining only to +7.5% on an ex-Finance basis.

Image Source: Zacks Investment ResearchThis is a bigger cut to estimates relative to what we saw in the comparable periods for the preceding two quarters. The negative revisions trend is broad-based, with estimates for 14 of the 16 Zacks sectors getting cut since the quarter began. The biggest cuts have been to the Transportation, Business Services, Energy, Aerospace, and Basic Materials sectors. On the positive side, estimates for the Tech sector are increasing, while the same for the Finance sector are only marginally higher relative to where we started in early July.Looking at earnings expectations on an annual basis, total 2024 S&P 500 earnings are expected to be up +8% on +1.8% revenue growth. Excluding the Energy sector drag, whose earnings are now expected to be down -11.8% in 2024, total earnings for the rest of the index would be up +9.6%.The expected 2024 revenue growth pace improves to +4.2% once Finance is excluded from the aggregate data, with the index-level aggregate earnings growth for the year declining only to +7.5% on an ex-Finance basis. Image Source: Zacks Investment ResearchUnlike the calendar year view that the above chart shows, the chart below the earnings data on a rolling four-quarter basis

Image Source: Zacks Investment ResearchUnlike the calendar year view that the above chart shows, the chart below the earnings data on a rolling four-quarter basis Image Source: Zacks Investment ResearchMore By This Author:Walmart Earnings & Consumer Spending Trends: A Closer Look

Image Source: Zacks Investment ResearchMore By This Author:Walmart Earnings & Consumer Spending Trends: A Closer Look

Earnings Estimates Face Pressure: What To Know

Retail Earnings Loom: A Preview