Image Source: Shutter2U – iStockPhoto

Image Source: Shutter2U – iStockPhoto

A Look Back at the Best Trades of the Past 50 Years

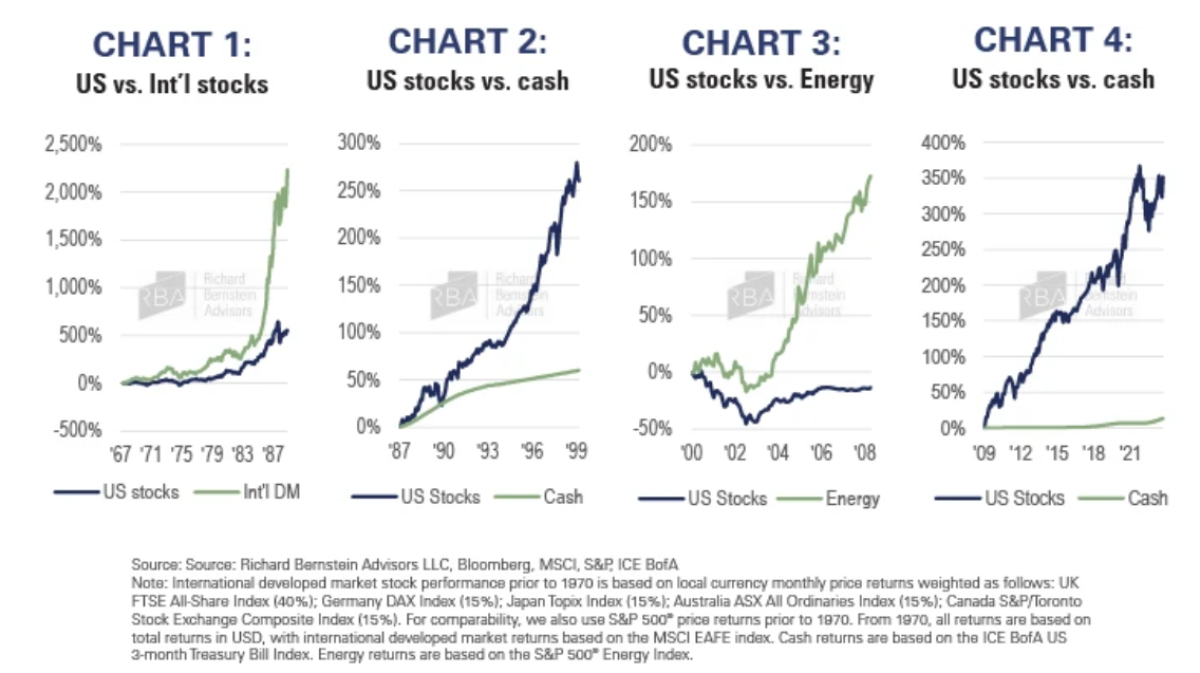

We believe that we are at a major inflection point in macro fundamentals and market leadership, offering investors a once-in-a-generation opportunity to reposition portfolios.To put the magnitude of this opportunity into perspective, we have identified what we believe are the best trades of the past 50 years — those asset class, regional, and sector allocation decisions that would have netted the greatest long-term outperformance. Each of these trades would have generated excess returns averaging 7-19% per year, spanning periods of eight-22 years:

The Rise and Fall of American Exceptionalism

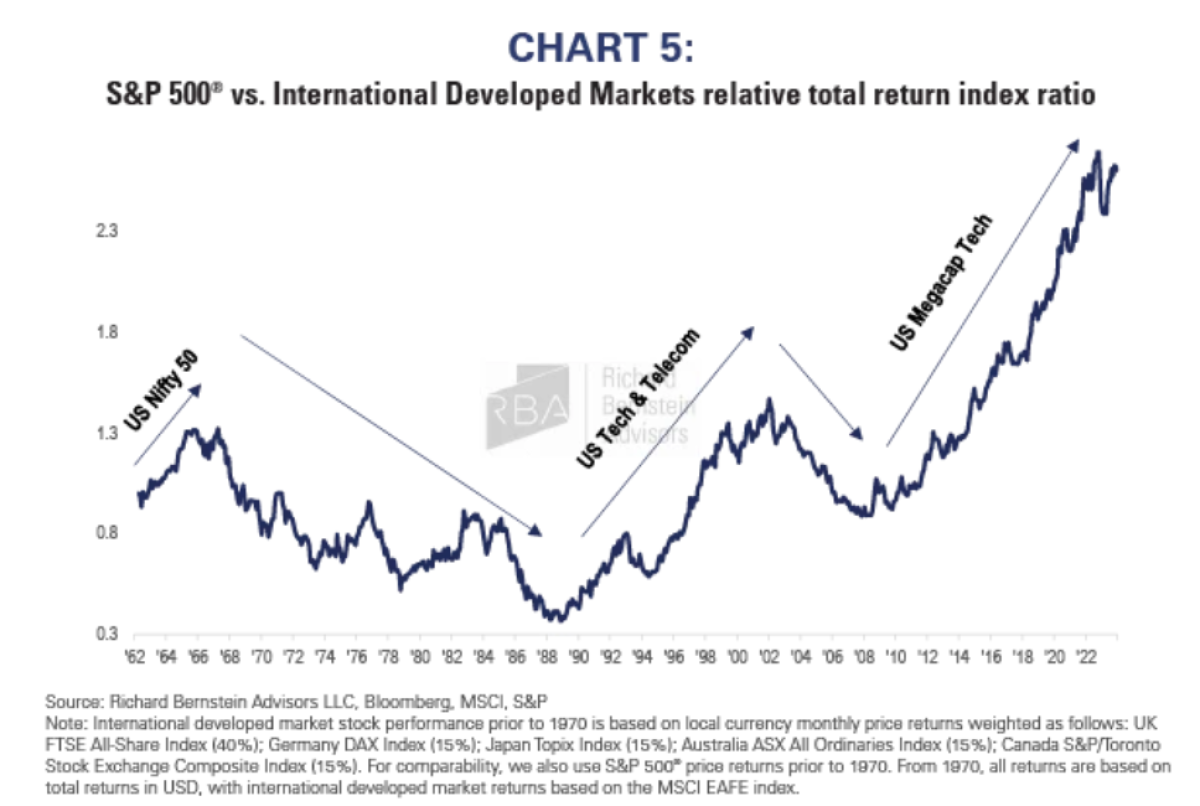

In many ways, each of these unique periods can be characterized by the rise of American exceptionalism.Beginning with the ascension of the US Nifty 50 stocks in the 1950s and 1960s, followed by the Tech and Telecom bubble of the 1990s, to the so-called Magnificent 7 leading today’s markets, a certain group of US companies becomes so dominant that they come to be perceived as the only stocks worth owning. Each time that became the pervasive sentiment, it generally signaled that the next big investment opportunities lay elsewhere (Chart 5).

The US Is Back to Being “The Only Investment Worth Owning”

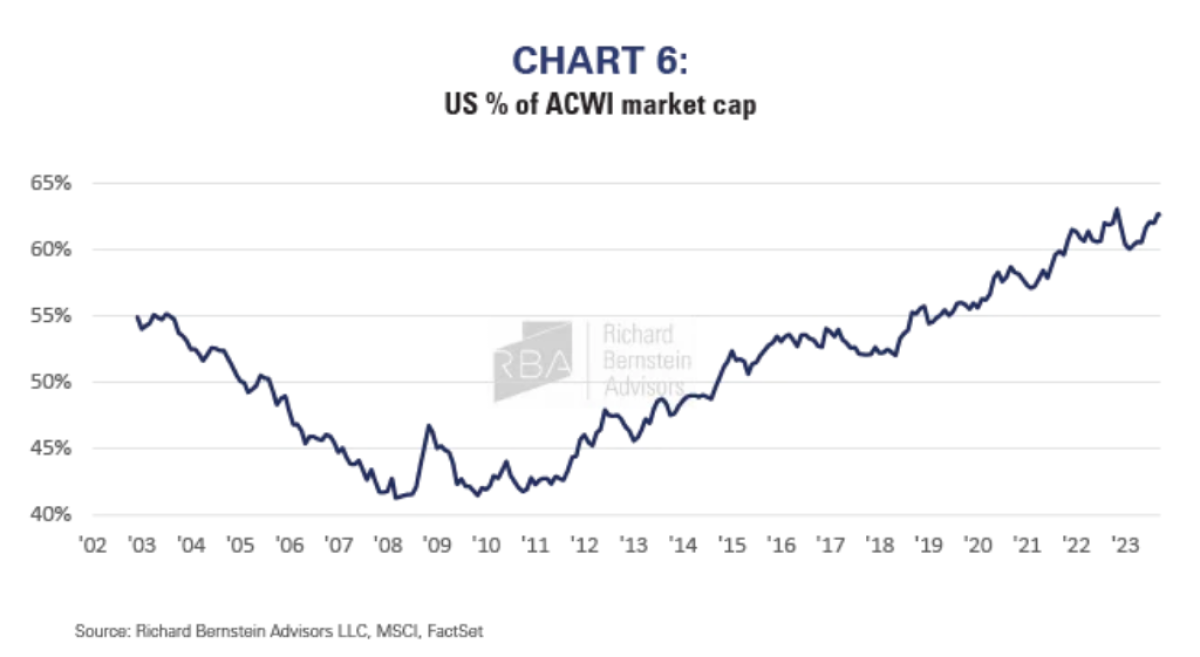

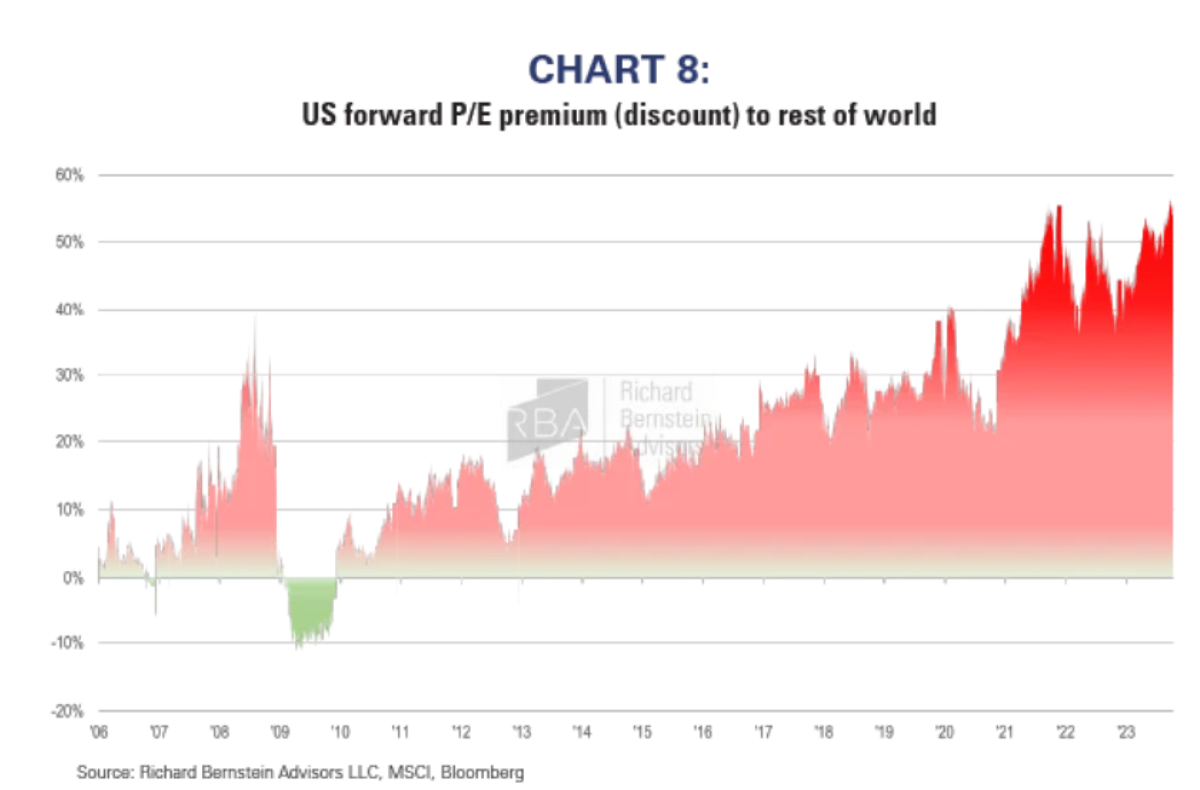

As the US has gone from “uninvestible” at the beginning of this bull market to today’s “obvious trade,” its share of the global stock market has surged from 40% to 64% (Chart 6), pushing market concentration to unprecedented levels (Chart 7). The US is the most expensive it has ever been compared to the rest of the world, with the premium having gone from -11% (a discount) in 2009 to +60% today (Chart 8).But rather than take steps to mitigate this extreme portfolio concentration, it appears that investors are doubling down. According to Bank of America’s latest fund manager survey, institutional investors are overweight US stocks, but even more worrisome may be the concentration in smaller investor portfolios.According to a recent Wall Street Journal article citing Vanda Research, the average individual’s stock portfolio has 40% of its value tied up in just three tech stocks.

Nothing Lasts Forever

Eventually, high valuations and unattainable growth expectations lead to disappointments and significant devaluations. The subsequent period of deteriorating fundamentals and weak returns causes the pendulum to swing to opposite extremes.As a result, periods of significant outperformance tend to be followed by periods of significant underperformance, reversing much of the previously earned extraordinary gains, even for the biggest of secular themes (Chart 9). Positioning and valuation suggest that investors expect the US equity dominance of the past 15 years will last indefinitely, but history seems to suggest otherwise (Chart 10).

A Once-in-a-Generation Opportunity Hiding in Plain Sight

Market leadership tends to change in response to structural shifts in the macroeconomic fundamentals. The global economy is currently undergoing major inflections across inflation, interest rates, globalization, corporate profitability, demographics, and government balance sheets. When coupled with the prevailing bifurcation of sentiment and record market concentration, the current juncture may offer investors a once-in-a-generation opportunity to rebalance portfolios.Just as in the wake of the Internet bubble, what part of the market you own could mean the difference between another lost decade of returns for crowded and expensive assets or very attractive returns or assets where capital is truly scarce. With all eyes on US large-cap growth stocks and disinflation beneficiaries, we see bigger opportunities in international, small-caps, value stocks, and inflation beneficiaries.

About the Author

Dan Suzuki is the Deputy Chief Investment Officer and Chairman of the Investment Committee at Richard Bernstein Advisors LLC. In his role, Dan leads RBA’s Investment Committee and is responsible for portfolio strategy, asset allocation, investment management, and marketing to major warehouses and independent RIAs.Prior to joining RBA, Dan worked at Bank of America-Merrill Lynch in Global Research for over 15 years, during a portion of which he worked closely with Rich Bernstein and Lisa Kirschner (RBA’s Director of Research). Most recently, Dan was a senior equity strategist, where in addition to his in-depth analysis on valuation and sectors, he authored regular publications on the S&P 500® EPS Outlook and US Small and Mid-Cap Strategy.Prior to working in strategy, Dan was a fundamental equity research analyst covering the Business Services sector. He is a frequent guest on CNBC, Bloomberg TV and is often quoted in leading financial publications including The Wall Street Journal, Financial Times and Barron’s. Dan holds a BS in economics from Duke University, and he has been a Chartered Financial Analyst® charterholder since 2006.More By This Author:The Distribution Of Stock Market ReturnsCredit Hedging Done Right: CDX Outperforms with DefenseDPLTA: Playing The German Back-End Game