Target’s Retail Legacy And Recent Strategy Shifts

Target (ticker symbol TGT) has long been a leader in the U.S. retail market, known for blending trendy apparel, home goods, and essentials at competitive prices.The company has rejuvenated its brand, focusing on supply chain efficiency, store renovations, and omni-channel innovation rather than physical expansion.These efforts paid off, with nearly 40% revenue growth since 2019, supported by pandemic-era trends like trip consolidation.Target Video Overview Of Savings Tips With Target Circle

However, Target faces stiff competition from retail giants like Amazon and Walmart, which use their scale to offer lower prices, and warehouse clubs that encroach on its household essentials segment.As a retailer with a largely undifferentiated product portfolio, Target must continually invest in operational efficiencies to compete on price while protecting margins.

Q3 Earnings Miss And Declining Sentiment

Target’s Q3 2024 results highlighted ongoing challenges. Comparable sales grew by a mere 0.3%, falling short of guidance (0–2%) and reflecting weaker performance in physical stores, particularly in discretionary categories like home furnishings and apparel.Target’s earnings shortfall and lowered guidance were attributed to shifting consumer preferences for discretionary items and proactive measures to address supply chain disruptions caused by a port strike. In contrast, competitors like Walmart and Costco posted stronger results in similar categories.This earnings shortfall, combined with lower-than-expected guidance for the holiday season, led to a sharp market reaction, with Target’s shares dropping over 20%.While digital sales grew by 10.8%, Target lagged behind Walmart’s 43% growth in e-commerce, raising concerns about its competitiveness in the digital space.

Challenges Weighing On Margins And Growth

Target’s margins have been under pressure due to promotional pricing strategies, cost increases in healthcare, general liability expenses, and rising selling and administrative costs.These factors, combined with weak consumer sentiment, suggest slower growth in the near term.Additionally, shifting consumer preferences away from discretionary items—an area where Target has more exposure than Walmart—exacerbate the pressure.While operational improvements remain a focus, these challenges are expected to persist in the short to medium term.

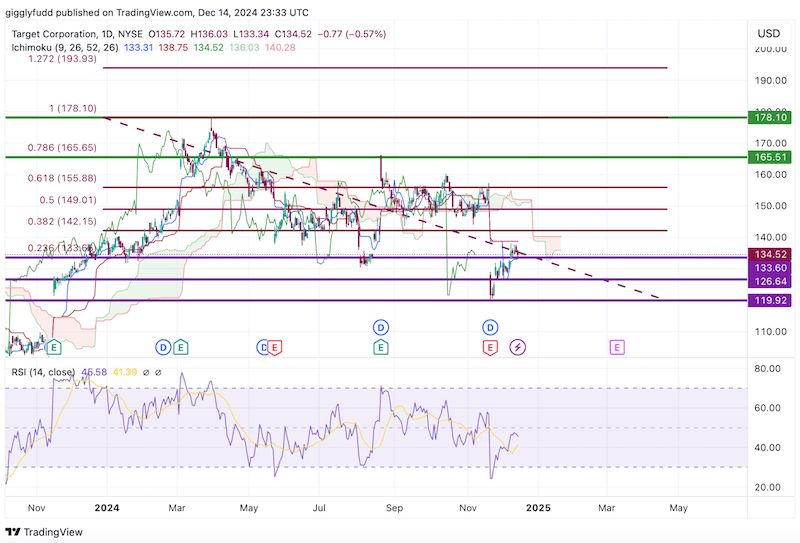

Technical AnalysisOn the daily chart, Target’s price has shown signs of recovery after a sharp post-earnings drop.While the Ichimoku future cloud remains bearish, it is flattening, suggesting potential stabilisation. Candlesticks remain below the cloud, but the recent upward trend could indicate a bottoming-out phase. My personal strategy is to buy at the current market price for a long-term hold, and I also plan on setting the following buy limits to take advantage of potential dips:

Buy Limit (BL) Ideas:

Remember: Investing is personal, and what is right for me might not be right for you. Always do your own due diligence. You should ONLY invest based on your own risk tolerance and your timeframe for reaching your portfolio goals.

A Potential Buying Opportunity For Long-Term Investors

Target’s stock decline may present an attractive entry point for those with a long-term outlook.While short-term challenges such as weak consumer sentiment and supply chain pressures weigh on growth, the company’s strategic initiatives could support a gradual recovery. Investors should carefully weigh Target’s current struggles against its potential for long-term growth and stability.Additionally, Target’s focus on expanding its e-commerce platform and enhancing supply chain efficiency positions it to adapt to evolving market demands.These efforts could drive sustainable growth once macroeconomic pressures subside.More By This Author:Do You Know What To Do When Stock Markets Are Crashing?

Investing In Uncertain Times? How To Use 100 Years Of Market History To Your Advantage

Upstart Holdings Stock Analysis: Navigating AI Lending In A Mixed Market