It is easy for those of us in the West to overlook how important China has become to the world economy, and also the limits it is reaching. The two big areas in which China seems to be reaching limits are energy production and debt. Reaching either of these limits could eventually cause a collapse.

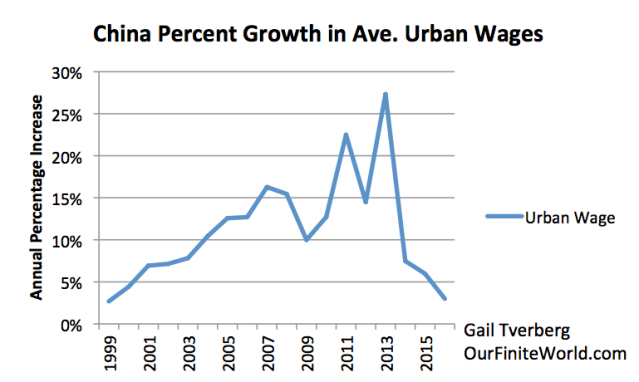

China is reaching energy production limits in a way few would have imagined. As long as coal and oil prices were rising, it made sense to keep drilling. Once fuel prices started dropping in 2014, it made sense to close unprofitable coal mines and oil wells. The thing that is striking is that the drop in prices corresponds to a slowdown in the wage growth of Chinese urban workers. Perhaps rapidly rising Chinese wages have been playing a significant role in maintaining high world “demand” (and thus prices) for energy products. Low Chinese wage growth thus seems to depress energy prices.

(Shown as Figure 5, below). China’s percentage growth in average urban wages. Values for 1999 based on China Statistical Yearbook data regarding the number of urban workers and their total wages. The percentage increase for 2016 was based on a Bloomberg Survey.

The debt situation has arisen because feedback loops in China are quite different from in the US. The economic system is set up in a way that tends to push the economy toward ever more growth in apartment buildings, energy installations, and factories. Feedbacks do indeed come from the centrally planned government, but they are not as immediate as feedbacks in the Western economic system. Thus, there is a tendency for a bubble of over-investment to grow. This bubble could collapse if interest rates rise, or if China reins in growing debt.

China’s Oversized Influence in the World

China plays an oversized role in the world’s economy. It is the world’s largest energy consumer, and the world’s largest energy producer. Recently, it has become the world’s largest importer of both oil and of coal.

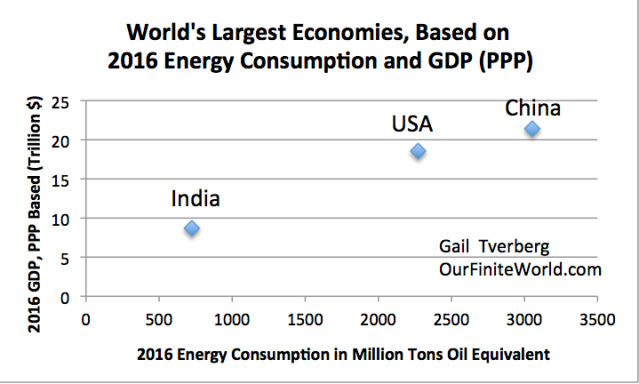

In some sense, China is the world’s largest economy. Usually, we see China referred to as the world’s second-largest economy, based on GDP converted to US dollars. Economists use an approach called GDP (PPP) (where PPP is Purchasing Power Parity) when computing world GDP growth. When this approach is used, China is the world’s largest economy. The United States is second largest, and India is third.

Figure 1. World’s largest economies, based on energy consumption and GDP based on Purchasing Power Parity. Energy Consumption is from BP Statistical Review of World Energy, 2017; GDP on PPP Basis is from the World Bank.

Besides being (in some sense) the world’s largest economy, China is also a country with a very significant amount of debt. The government of China has traditionally somewhat guaranteed the debt of Chinese debtors. There is even a practice of businesses guaranteeing each other’s debt. Thus, it is hard to compare China’s debt to the debt level elsewhere. Some analyses suggest that its debt level is extraordinarily high.

How China’s Growth Spurt Started

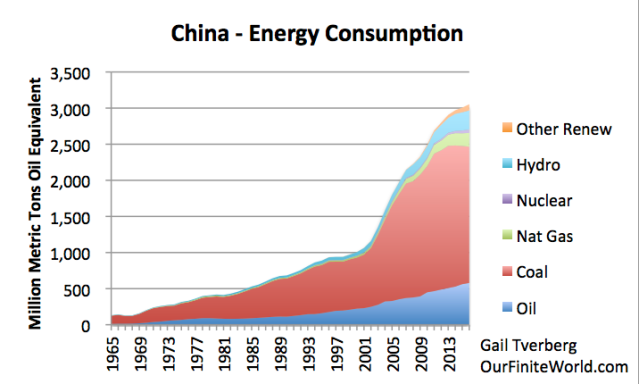

Figure 2. China’s energy consumption, based on data from BP Statistical Review of World Energy, 2017.

From Figure 2, it is clear that something very dramatic happened to China’s coal consumption about 2002. China joined the World Trade Organization in December 2001, and immediately afterward, its coal consumption soared.

Countries in the OECD, whether they had signed the 1997 Kyoto Protocol or not, suddenly became interested in reducing their own greenhouse gas emissions. If they could outsource manufacturing to China, they would be able to reduce their reported CO2 emissions.

Besides reducing reported CO2 emissions, outsourcing manufacturing to China had two other benefits:

Of course, a major downside of moving jobs to China and other Asian nations was the likelihood of fewer jobs elsewhere.

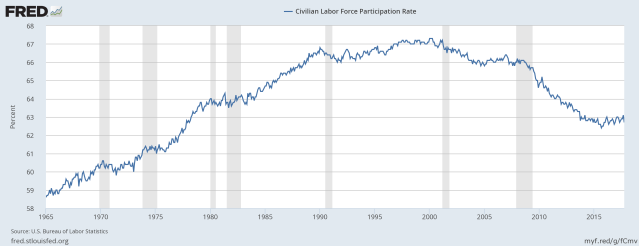

Figure 3. US Labor Force Participation Rate, as prepared by Federal Reserve Bank of St. Louis.

In the early 2000s, when China started competing actively for jobs, the share of people in the US workforce started shrinking. The drop-off in labor force participation did not level out until mid-2014. This is about when world oil prices began to fall, and, as we will see in the next section, when China’s growth in average wages began to fall.

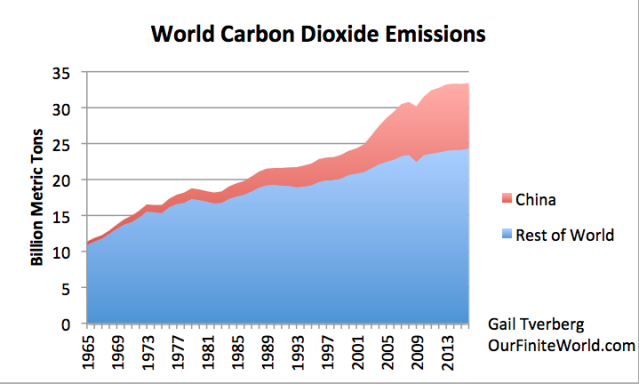

Another downside to moving jobs to China was more CO2 emissions on a worldwide basis, even if emissions remained somewhat lower locally. CO2 emissions on imported goods were not “counted against” a country in its CO2 calculations.

Figure 4. World carbon dioxide emissions split between China and Rest of the World, based on BP Statistical Review of World Energy, 2017.

At some point, we should not be surprised if countries elsewhere start pushing back against the globalization that allowed China’s rapid growth. In some sense, China has lived in an artificial growth bubble for many years. When this artificial growth bubble ends, it will be much harder for China’s debtors to repay debt with interest.

China’s Rapid Wage Growth Stopped in 2014

Rising wages are important for making China’s growth possible. With rising wages, workers can increasingly afford the apartments that are being built for them. They can also increasingly afford consumer goods of many kinds, and they can easily repay debts taken out earlier. The catch, however, is that wage growth cannot get ahead of productivity growth, or the price of goods will become too expensive on the world market. If this happens, China will have difficulty selling its goods to others.