Written by Gail Tverberg, Our Finite World

The world is in a dangerous place now. A large share of oil sellers need the revenue from oil sales. They have to continue producing regardless of how low oil prices go unless they are stopped by bankruptcy, revolution, or something else that gives them a very clear signal to stop. Producers of oil from U.S. shale are in this category, as are most oil exporters, including many of the OPEC countries and Russia.

Some large oil companies, such as Shell (RDS-A), and ExxonMobil (XOM), decided even before the recent drop in prices that they couldn’t make money by developing available producible resources at then available prices, likely around $100 barrel. See my post, Beginning of the End? Oil Companies Cut Back on Spending. These large companies are in the process of trying to sell off acreage, if they can find someone to buy it. Their actions will eventually lead to a drop in oil production, but not very quickly–maybe in a couple of years.

So there is a definite time lag in slowing production–even with very low prices. In fact, if U.S. shale production keeps rising, and Libya and Iraq keep work at getting oil production on line, we may even see an increase in world oil production, at a time when world oil production needs to decline.

A Decrease in Oil Prices May Not Fix Oil Demand

At the same time, demand does not pick up as quickly as prices drop. We are dealing with a world that has a huge amount of debt. China in particular has been on a debt binge that cannot continue at the same pace. A reduction in China’s debt, or even slower growth in its debt, reduces growth in the demand for oil, and thus its price. The same situation holds for other countries that are now saturated with debt, and trying to come closer to balancing their budgets.

Furthermore, the Federal Reserve’s discontinuation of quantitative easing has cut off a major flow of funds to emerging markets. Because of this change, emerging market demand for oil has dropped. This has happened partly because of the lower investment funds available, and partly because the value of emerging market currencies relative to the dollar has fallen. Again, a decrease in oil price is not likely to fix this problem to a significant extent.

Europe, and Japan are having difficulty being competitive in today’s world. A drop in oil prices will help a bit, but their problems will mostly remain because to a significant extent they relate to high wages, taxes, and electricity prices compared to other producers. The reduction in oil prices will not fix these issues, unless it leads to lower wages. The reduction in oil prices is instead likely to lead to a different problem–deflation–that is hard to deal with. Deflation may indirectly lead to debt defaults and a further drop in oil demand and oil prices.

Thus, oil prices are likely to continue their slide for some time, until real damage is done, perhaps to several economies simultaneously.

The United States’ Role in the Oil Over-Production / Under-Demand Clash

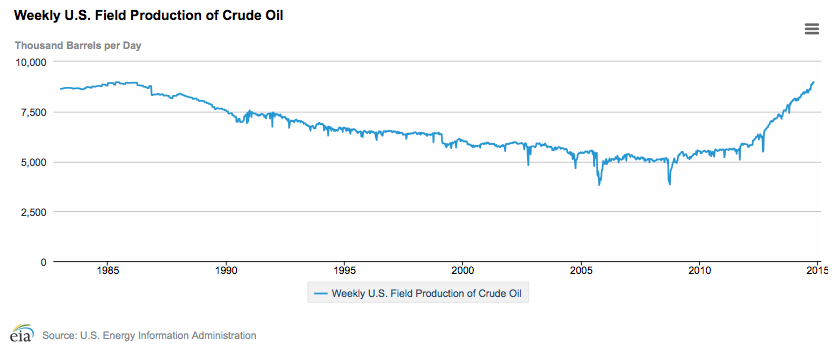

The United States is the country with the single largest increase in oil production in the past year. This growth in oil production seems not to have stopped, in recent weeks.

Figure 1. U.S. Weekly Crude Oil Production through Oct 24. Chart by EIA.

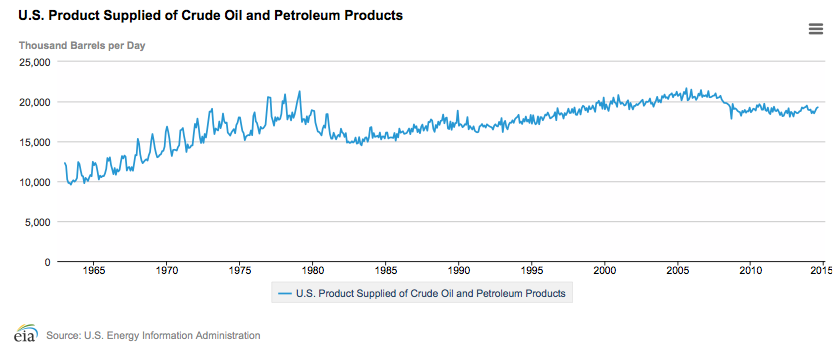

At the same time, U.S. oil consumption has not increased (Figure 2).

Figure 2. U.S. oil consumption (called “Product Supplied”). Chart by EIA.

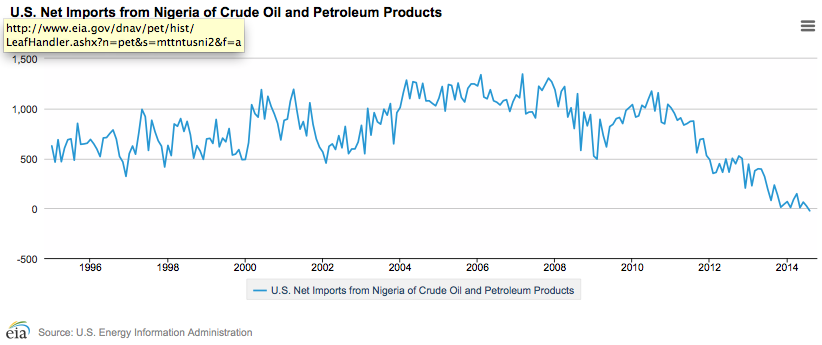

The result is a drop in needed imports. A number of oil exporters have been hit by the U.S. drop in imports. Nigeria extracts a very light oil that competes for refinery space with oil from shale formations. Our imports of Nigerian oil have been reduced to zero (Figure 3). (The amounts I am showing on this and several other charts are “net imports.” These reflect transactions in both directions. Often the U.S. imports crude oil and exports oil products, sometimes to the same country. In such a case, we are selling refinery services.)

Figure 3. U.S. Net Petroleum Imports from Nigeria. Chart by EIA.

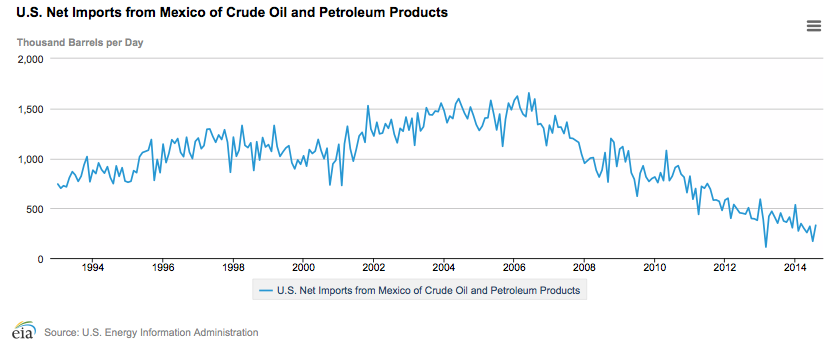

Our imports of oil from Mexico are way down as well (Figure 4), in part because their oil production has been falling.

Figure 4. U.S. Net Imports of Petroleum from Mexico. Chart by EIA.

It is only in the past few months that U.S. imports from Saudi Arabia have started to be significantly affected (Figure 5).