In April 2007 the approximate size of the Fed’s balance sheet was $800 billion, meaning that over the last decade it ballooned by 5X to $4.4 trillion. This was supposed to “stimulate” the main street economy, but once again today we got some “in-coming data” that said essentially nuts to that.

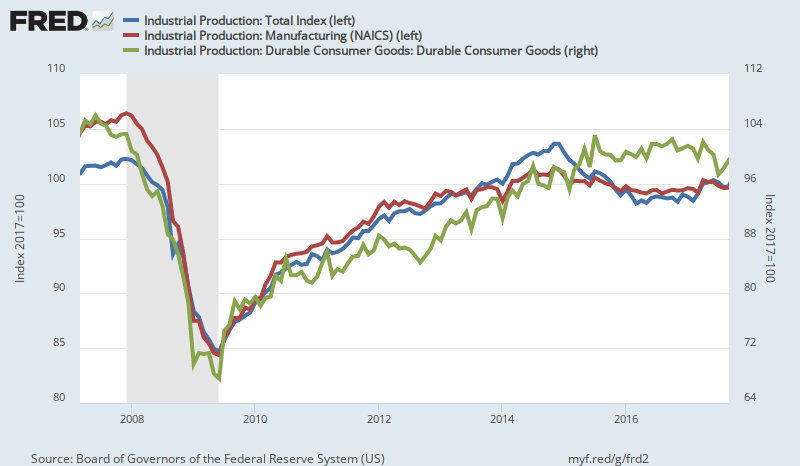

We are referring to the monthly industrial production index for September that the near-sighted financial press greeted as a modest but welcome rebound (o.3%) from last month’s hurricanes which came, well, in hurricane season.

Actually, we saw something considerably more salient. To wit, the overall index came in at a level first reached in April 2007, while the sub-indexes for manufacturing and durable consumer goods are actually still 3.5% below where they were before even the first hint of the great financial crisis.

So let’s see. After a full decade, the “stimulant” has grown by about 5.5X while the “stimulee” is up by 0.0X. Accordingly, the thought occurs that what is being stimulated may not be the main street economy at all.

Indeed, as we shall suggest below, it is not just the Wall Street casino that is collecting huge windfalls from the central bank’s egregious falsification of money. The real bonanza, in fact, is accruing to the very tippy top of that fortunate precinct——-the top 0.0001% or a few thousand hedge fund and private equity operators.

But first let us address the usual canard that in this age of awesome technology and social media dominance that “industrial production” is going the way of the buggy whip and ain’t that important no more.

In fact, that is only true statistically and at the most aggregated level of the GDP numbers. That is, private services and government accounted for $12.4 trillion or 64.4% of the $19.3 trillion rate of nominal GDP in Q2 2107. By contrast, goods production amounted to $4.2 trillion, business investment in plants and equipment was $1.6 trillion and residential construction amounted to $740 billion.

So loosely refer to the latter three components of GDP as “industrial production” and you get $6.6 trillion or just 34% of the total GDP. The implication, of course, is that if the industrial one-third has been flat-lining for a decade, there is always the much bigger services side of the economy to pull the weight of growth and jobs and income generation.

Then again, it’s not even close to being that simple. We will argue until the cows come home that the $3.3 trillion government sector subtracts from real growth and living standards and that its pork barrel modus operandi inherently generates negative productivity growth.

After all, according to the national income and product accounts fully 22% of that amount or $741 billion is accounted for by defense. As a non-interventionist and anti-Warfare State advocate, we don’t see much tangible “safety” or “security” coming from all that military spending, but we are absolutely certain that it does not contribute to private utility and real wealth.