Listen, here’s the thing: at some point, credit markets are going to wake up.

Now I’ll confess I have no idea when that’s going to be and if the last 13 months have taught us anything, it’s the DM central bank liquidity tsunami is capable of keeping spreads near their post-crisis tights even in the face of political turmoil the likes of which we haven’t seen since World War II.

I was talking to a credit strategist at one of Wall Street’s biggest banks this week and he shared my incredulity at how Teflon credit has proven to be.

For anyone interested in a truly illuminating look at how still the credit pond has been, I strongly encourage you to at least skim “That’s Not Low Volatility, THIS Is Low Volatility.”

More than a few commentators have remarked on credit’s resilience in the face of the recent DM rates mini-tantrum. Consider, for instance, what spreads have done since Draghi’s “transitory” inflation comments in Sintra on June 27. “Credit spreads tightened over the past three weeks despite some notable rate volatility along the way,” Deutsche Bank noted last night, adding that “IG stood out during the period, in relative terms, having seen its OAS tighten by 7bp to 109 in the environment of rising rates, which could be described as very strong in Europe, and moderate in the US.”

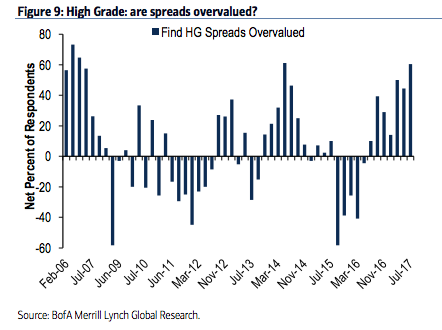

So it’s against that backdrop that we present the results from BofAML’s most recent credit investor survey in which “the net share [of respondents] that found high grade spreads overvalued increased to 60% in July – the highest level since May 2014 when spreads were near cyclical tights – from 44% in May”…

… even as “the net share of high grade investors expecting wider spreads over the next three months declined to 21% in July from 36% in May“…

So while investors may have pushed out the timeline on a selloff, you should probably note that “the net share expecting wider spreads in 12 months jumped to 78% in July – the highest on record – from 39% in May”…