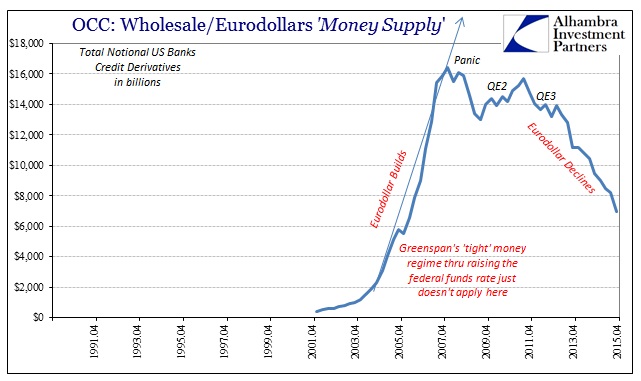

The basis for the ongoing economic paradigm shift that seems to be manifesting in a slow, lingering slowdown (that is now more than year into contraction) in the US and global economies can be nothing but the withdrawal of banks from the necessities of the credit-based reserve currency. So far, the updated bank reports for Q4 last year continue the trend, as do aggregated figures such as that provided by the Office of Comptroller of the Currency’s (OCC) derivative report. Taken from bank call sheets, it is the most comprehensive view of banking activities at least as related to window dressed reporting periods.

Given the circumstances of that time, following the events of August and prefiguring the events of January/February, the OCC finds in Q4 significant bank withdrawal by the proxy of reported gross notional derivative exposures. Total credit default swaps, once undoubtedly the marginal “currency” of interbank function at the eurodollar system’s artificial height, have withered to just $6.99 trillion, almost $10 trillion less than Q1 2008 just before Bear Stearns kicked off the full adjustment. That is the lowest offered balance sheet capacity for credit derivatives since the middle of 2006 nearly a decade ago; and that figure likely consists almost entirely of stale, prior books that are just being runoff.

It is still significant, however, that the trajectory shifted again lower after the events in the middle of 2013 (taper tantrum and the end of QE as possibly “open ended”). That extraction has only continued during the “rising dollar” period, seeing significant additional emphasis on getting out of the space.

Similarly, total interest rate swap notionals declined 20% in Q4 2015 from Q4 2014, to just $138 trillion. That is down almost a third since 2013, with the majority of the reduction being experienced also during the so-called rising dollar.

Total notional derivatives have fallen in line with interest rate swaps, which is expected since IR swaps make up the vast majority by dollar notional. The decay of the eurodollar system as exhibited by balance sheet reporting of notional exposures matches up with the 2011-12 shift in global economic fortunes since that time/inflection. The rebound trajectory after the 2008 panic had been subdued to begin with, and it seems as if the circumstances of 2011 convinced many participants that a full paradigm alteration was at hand.