Every investor has their own unique needs and tolerance for risk, and no one has a working crystal ball. Nonetheless, by assembling a prudent mix of portfolio investments, every individual can increase their odds for success.

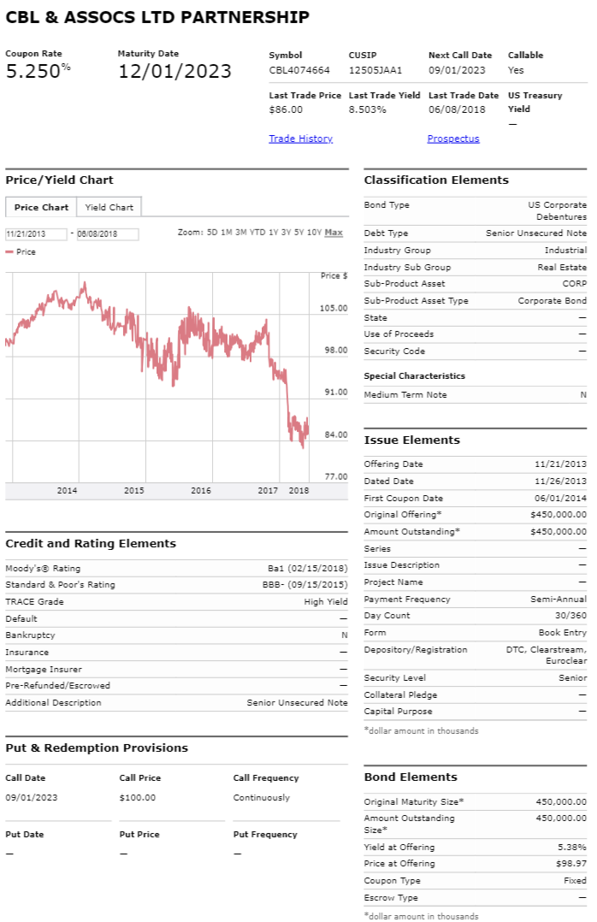

And depending on your situation, the 6.1% yield coupon payments on CBL’s 2023 bonds (they pay a 5.25% coupon at par, but currently trade at a discounted price of 86 cents on the dollar, 5.25% / 0.86 = 6.1%), may be a far better investment option than CBL’s equities (common and preferred), especially considering the bonds recently fell sharply to less than par (i.e. the 86 cents on the dollar thing) thereby providing the opportunity for a double digit percentage gain in price (perhaps sooner than later) and that’s in addition to the 6.1% yield, paid semiannually.

Note: This report was originally released to Blue Harbinger members on June 8th.

CBL & Associates Properties, Inc (CBL)

If you don’t know, CBL is one of the largest owners and developers of malls and shopping centers in the United States. And performance for this REIT has been terrible, as shown in the following chart.

CBL’s Common Equity (CBL), Yield: 13.9%

CBL has been dealing with a variety of challenges that have caused the price to decline dramatically. For starters, shopping malls have been facing new, growing, disruptive online competition from the likes of Amazon, for example. And it doesn’t help that CBL’s properties are not the attractive experiential A-class properties that command higher rents, more foot traffic, and less rent concessions.

Rising interest rates pose another challenge for REITs like CBL. Because they are required to pay out most of their income as dividends, REITs rely heavily on borrowing to fund their businesses; therefore REITs (like CBL) can be particularly sensitive to rising rates (i.e. it increases their significant borrowing costs). Compounding this challenge, many market participants had been utilizing REITs as a bond-like proxy considering bond yields were so low and REITs offer relatively high income. But as bond yields rise, REITs become less attractive to many investors, thereby putting further pressure on the market price of REIT securities.

Finally, as many investors are painfully aware, CBL reduced its big dividend recently. And considering the shares have fallen so far, and the yield is so high, many investors are worried another dividend reduction (or worse) could be on the horizon. We’ll have more to say about CBL’s cash flows later in this report.