Note: This commentary has been updated to include Friday’s release of the August data for Real Personal Income Less Transfer Receipts.

Official recession calls are the responsibility of the NBER Business Cycle Dating Committee, which is understandably vague about the specific indicators on which they base their decisions. This committee statement is about as close as they get to identifying their method.

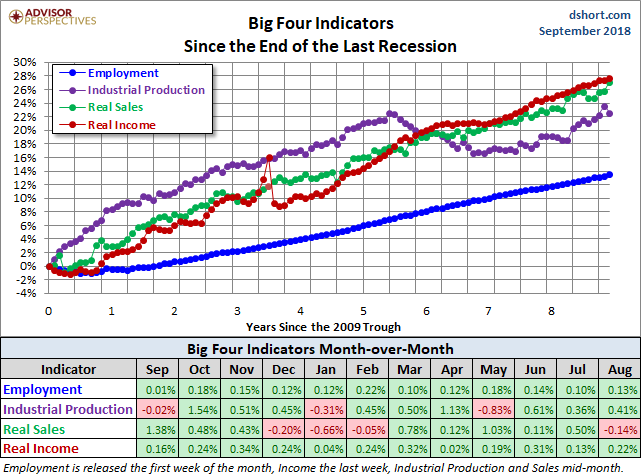

There is, however, a general belief that there are four big indicators that the committee weighs heavily in their cycle identification process. They are:

The Latest Indicator Data

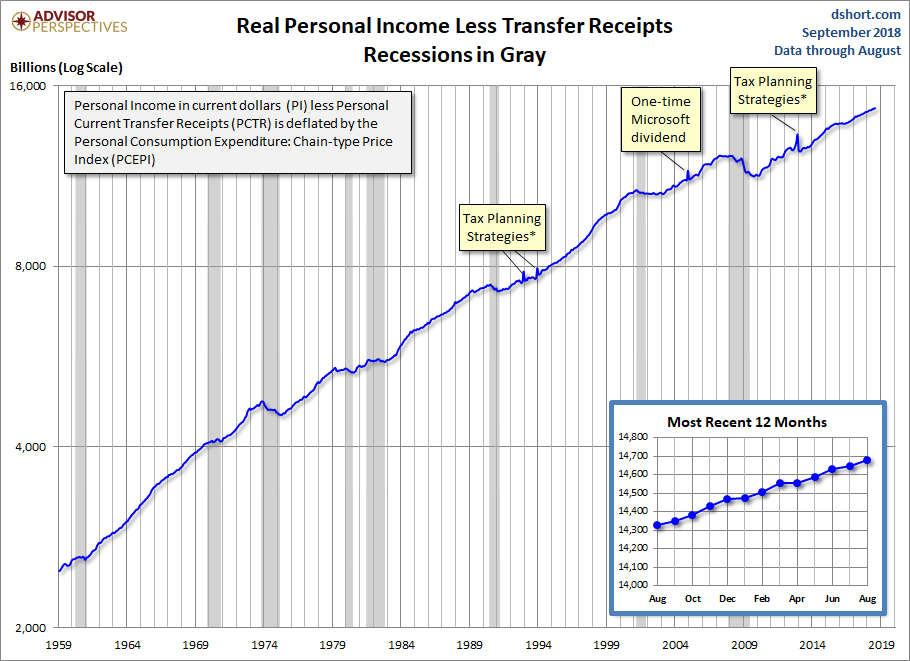

Personal Income (excluding Transfer Receipts) in August rose 0.33% and is up 4.7% year-over-year. However, when adjusted for inflation using the BEA’s PCE Price Index, Real Personal Income (excluding Transfer Receipts) MoM was at 0.22%. The real number is up 2.5% year-over-year.

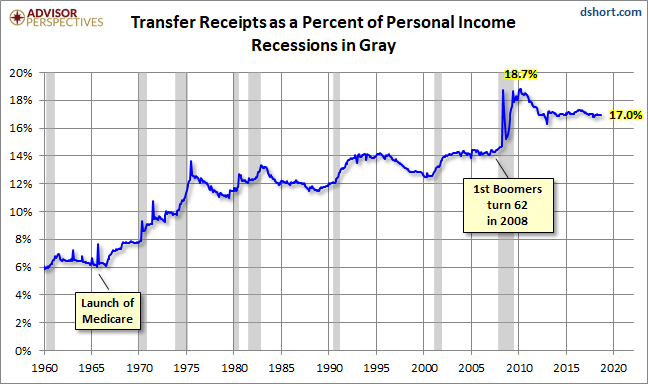

A Note on the Excluded Transfer Receipts: These are benefits received for no direct services performed. They include Social Security, Medicare & Medicaid, Unemployment Assistance, and a wide range other benefits, mostly from government, but a few from businesses. Here is an illustration of Transfer Receipts as a percent of Personal Income.

The Generic Big Four

The chart and table below illustrate the performance of the generic Big Four with an overlay of a simple average of the four since the end of the Great Recession. The data points show the cumulative percent change from a zero starting point for June 2009.

Current Assessment and Outlook

The US economy has been slow in recovering from the Great Recession, and the overall picture has been a mixed bag. Employment and Income have been relatively strong. Real Retail Sales have been rising but below trend. Industrial Production has been slow to recover and has finally been showing signs of improvement.