This chart series features an overlay of the Four Bad Bears in U.S. history since the equity market peak in 1929. They are:

The series includes four versions of the overlay: nominal, real (inflation-adjusted), total return with dividends reinvested and real total return. The starting point is the aligned peaks prior to the four epic declines. We’ve used an interval of 252 days for the x-axis as it is roughly the number of market days in a calendar year.

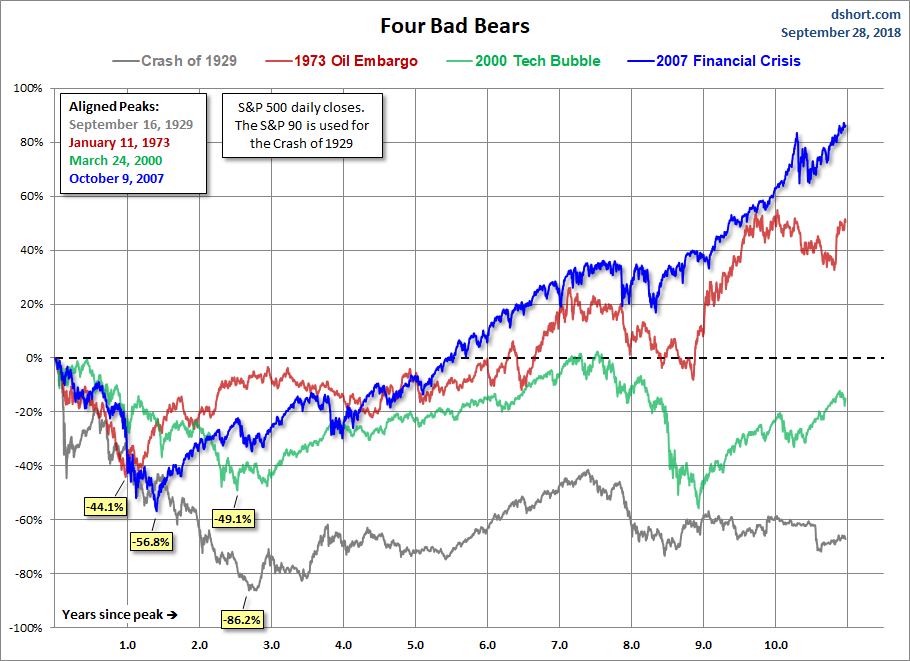

The first chart shows the price, excluding dividends for these four historic declines and their aftermath. As of the September 28 close, we are now 2763 market days from the 2007 peak in the S&P 500.

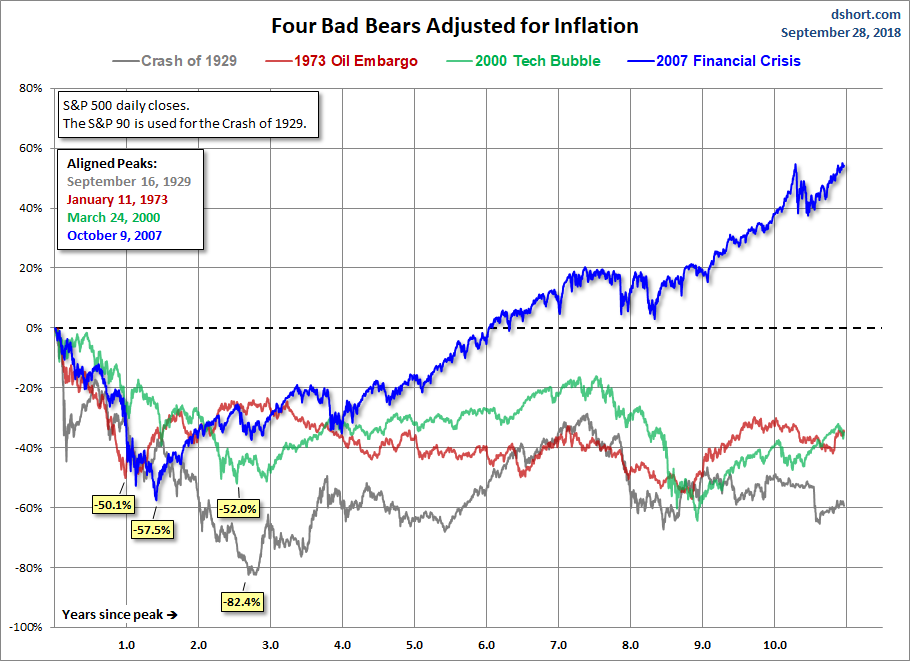

Inflation-Adjusted Performance

When we adjust for inflation, the gap between our current recovery and the other three widens, thanks to exceptionally low inflation in recent years.

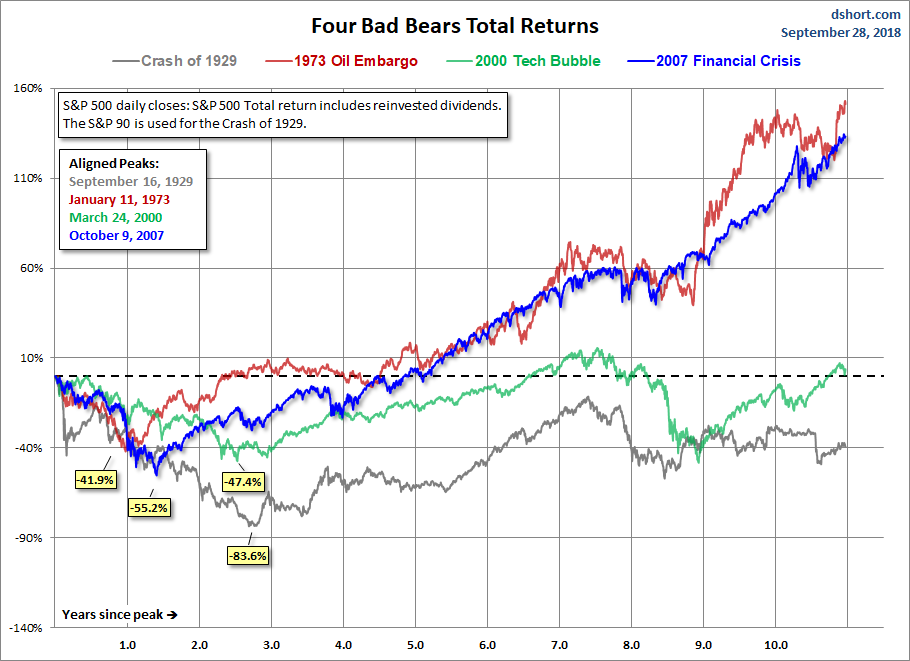

Nominal Total Returns

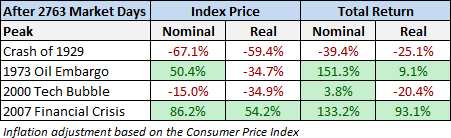

Now let’s look at a total return comparison with dividends reinvested. The 1973 Oil Embargo Bear recovery is the top performer, up 151.3%. The current recovery is in second place, up 133.2%.

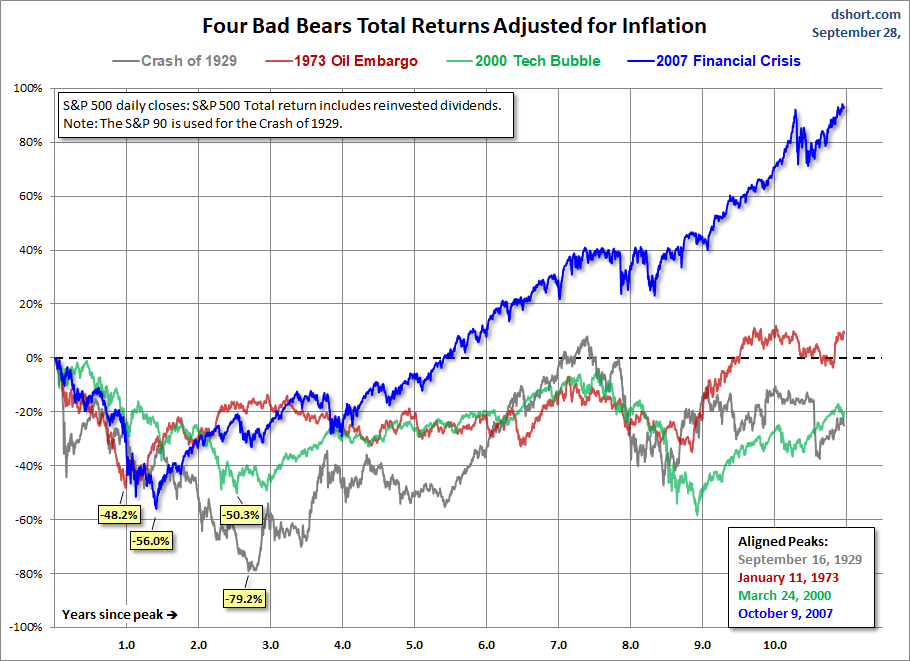

Real Total Returns

When we adjust total returns for inflation, the picture significantly changes. The spread between three of the four markets narrows dramatically, and the current real total return since the 2007 crisis has pulled far ahead of the others, up 93.1%. Second place, by this metric, goes to the post-Oil Embargo rally, with 9.1%.

Here is a table showing the relative performance of these four cycles at the equivalent point in time.

For a better sense of how these cycles figure into a larger historical context, here’s a long-term view of secular bull and bear markets, adjusted for inflation, in the S&P Composite since 1871.