Official recession calls are the responsibility of the NBER Business Cycle Dating Committee, which is understandably vague about the specific indicators on which they base their decisions. This committee statement is about as close as they get to identifying their method.

There is, however, a general belief that there are four big indicators that the committee weighs heavily in their cycle identification process. They are:

The Latest Indicator Data

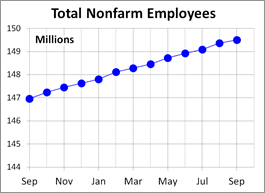

This commentary has been updated to include this morning’s release of Nonfarm Employment. September’s 134 increase in total nonfarm payrolls was accompanied by upward revisions of 87K. The unemployment rate dropped to 3.7%. The Investing.com consensus was for 185K new jobs and the unemployment rate to drop to 3.8%.

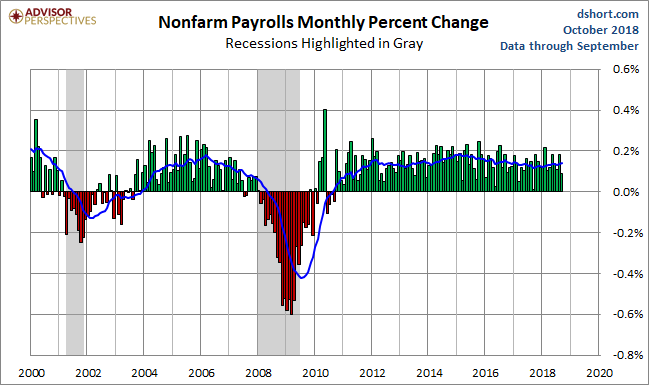

The chart below shows the monthly percent change in this indicator since the turn of the century, a period that includes two recessions. We’ve included a 12-month moving average to help visualize the trend.

The Problem of Revisions

At first glance, this indicator appears to have a strong correlation with the business cycle. However, there is a major problem with this assumption: The data in this survey of business establishments undergo multiple revisions. The initial monthly estimate is subject to a first and second revision, subsequent benchmark revisions and annual revisions that stretch back many years (the most recent includes revisions back as far as February 1990). The cumulative size of the revisions is quite stunning, much of which is owing to the “hindsight” of those annual revisions.

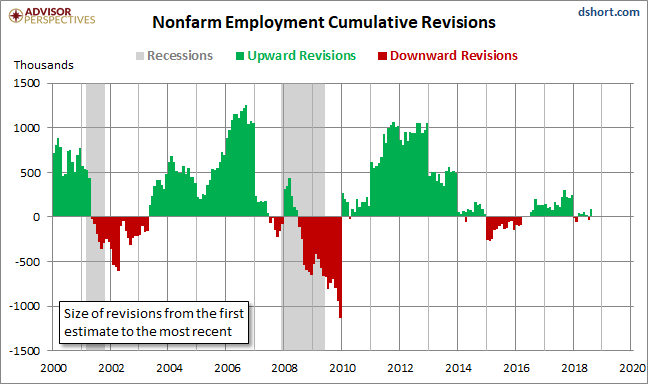

The chart below measures the size of the revisions from the initial estimate to the latest employment report.

The Problem of Population Growth

Another problem with the Nonfarm Employment data is that it isn’t adjusted for population growth, which reduces its usefulness in illustrating secular trends. The chart below incorporates a population adjustment by dividing the Nonfarm Employment (FRED series PAYEMS) by the Civilian Labor Force Age 16 and Over (FRED series CLF16OV). We’ve added a couple of trend lines and a callout — not to suggest a forecast but rather to highlight the potential impact of a near-term business-cycle downturn. Note also that the current level is about where we were during the 2001 recession.