The Italian government has created another massive turmoil in European markets with its 2019 budget proposal.

With a huge increase in spending, it estimated a deficit of 2.4% for 2019 compared to its previous target of 0.8% and the 1.6% announced by the finance minister.

Not only does it represent a huge increase in a country that already has 131% of debt over GDP, but a brief analysis of the tax revenue estimates shows that the figure presented is simply unattainable. Most independent analysts pointed the evidence of over-optimistic estimated revenues, raising fears of an additional 14 billion euro financial gap.

The Milan stock market collapsed, banks had to be suspended from trading after falling 6-7%, bond yields soared and the 10-year Italian bond fell to the worst level in a year despite the interventions of the European Central Bank.

This is what happens when a country with enormous internal problems launches itself to the eternal magic solution of spending much more and increasing deficits.

Many commented that this is the “price of sovereignty”. Someone has to enlighten me on how you achieve sovereignty raising debt and increasing current spending.

Anyone who believes raising imbalances and threatening with default and leaving the euro is going to be the solution for Italy ahead of billions in maturities and with banks burdened with enormous non-performing loans and government bonds, simply dreams.

The prospect of capital controls, bank runs, and domino bankruptcies is even conservative.

The biggest problem of the proposals is that they are the same old mistakes that never worked. Massive subsidies and political spending are not tools for growth but the recipe for stagnation and ultimately larger and more painful adjustments in the long term.

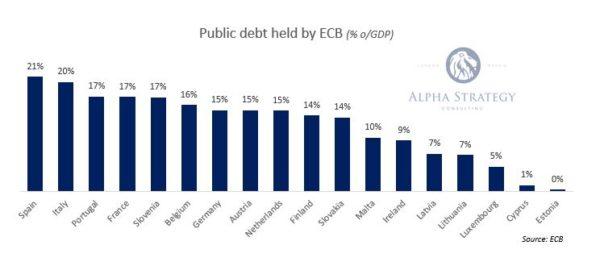

Italy has been one of the main beneficiaries of the ECB bond purchase program. Despite the enormous bubble and bond yield compression created by the quantitative easing policy, Italian bond yields have soared. Imagine outside of the eurozone and with a central bank committed to copying Argentina and Turkish monetary policies, as Spain or Italy did before the euro.