I have been pessimistic on the U.S. economy even before the financial crisis. The government’s response to the crisis — quantitative easing and bail outs to Wall Street — has been great for the investor class, but has done nothing for the populace. Now that the Fed has taken away the punch bowl I expect the economy to pull back again. I believe cyclical names like Thor Industries THO are headed for a fall, and I have been loud about it:

In 2015, industry RV shipments surpassed 374,000 in 2015 – the first time this has happened since 2006; they fell to as low as 166,000 in 2009. Shipment have rose steadily since, spurred by quantitative easing by central banks. In addition to an end to the Fed’s stimulus program, the U.S. economy is beginning to show cracks … If workers are concerned about their future, they may be reticent to spend on big ticket items like RVs with an average cost of about $80,000.

Now that the Fed is no longer creating a wealth effect in stocks, fundamental analysis may become more important. My bottoms up analysis implies THO is 20% overvalued.

Thor Is Worth $48

According to my valuation THO is worth $48 and is about 20% overvalued.

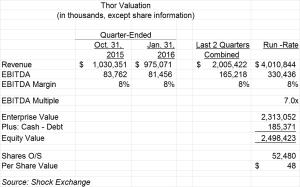

Run-Rate Revenue

Run-rate revenue is simply revenue for the last two quarters annualized. The company generated $2 billion combined revenue over the past six months. The run-rate of $4 billion is slightly optimistic given that revenue is trending down. For the most recent quarter the top line fell 5% sequentially. Unit volume also fell 8% sequentially and it could fall further if Thor runs out of acquisition targets.

EBITDA

EBITDA is actual results for the past two quarters annualized. I expect the 8% margin to erode due to a loss of scale. The dual impact of revenue declines and margin erosion could cause a sharp decline in the stock.

EBITDA Multiple

A multiple of 5.0x to 7.0x is appropriate for an industry leader in a cyclical industry in decline. I valued Thor at the top end of the range since EBITDA has been relatively stable thus far.