Wonderful CPI Day

Mar 16, 2016Jeremy ParkinsonFinance

My Post-CPI Tweets

Good morning and welcome to another wonderful CPI day!

Three notes before CPI prints in 17 minutes: First, the market is expecting a “soft” 0.2% core (something like 0.16%, rounding up)

Second: If we get exactly 0.2% core, then y/y will round higher to 2.3%. Third: if we get exactly 0.3%, y/y core will round to 2.4%.

Highest core print since the crisis was 2.32% in 2012. We have a shot of exceeding that today with a robust print.

Ten minutes to CPI and time for 1 more coffee and a commercial message: please buy my new book!

whoopsie, core CPI +0.3%. Actually 0.28%, puts y/y at 2.34%. Yayy, a new post-crisis record!

Ouch, seems like a big jump in y/y Medical Care, waiting for the breakdown. If so, that makes core PCE jump even more (again).

So back to back months we’ve had 0.29% and 0.28%. I hate to say I told you so but…

I said 2.33%, Actually 2.34%. We were VERY close to printing 2.4% y/y & setting off panic at the Fed. Which is abt 4 yrs overdue.

I should say 4 years and $2 trillion overdue.

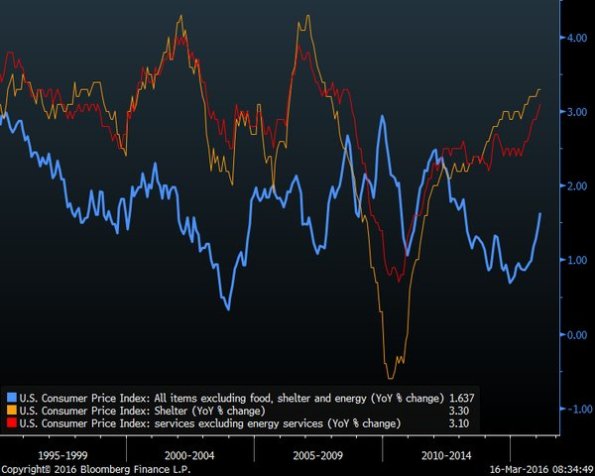

[retweet from @boes_] Core consumer price inflation ex-shelter really accelerating: was 1.6% year over year in February

core cpi. What, me worry?

while I wait for my sheets to calculate, let me stress this is not meaningless for the FOMC meeting today.

Arguments for waiting another meeting before raising rates are very thin.

i have got to put this database on a faster computer. OK, core services 3.1% from 3% and core goods +0.1% from -0.1%.

first positive y/y in core goods in two years.

Housing: 2.12% from 2.10%. Primary rents (3.68% from 3.71%) and OER (unch at 3.16%) are NOT the drivers of the core jump.

Lodging away from home 4.19% vs 2.67%, but that’s a small piece of CPI (<1%)

Apparel had big jump in y/y rate to 0.89% from -0.53%, but again Apparel as a whole is 3% of headline, 4% of core.

Medical care: 3.50% from 3.00%. Yep.

Drugs 2.34% from 2.21%. Professional svcs 2.54% from 2.08%. Hospital svcs 4.90% from 4.32%. Health insurance 5.97% from 4.76%. Ouch.

Med care is ~10% of core, so that 50bp jump is 0.05% on core.

And remember, Medical care gets a HIGHER WEIGHT in the Fed’s preferred measure, core PCE.

U-G-L-Y CPI ain’t got no alibi. It’s ugly (woot! woot!) it’s ugly.

The good news is pretty thin gruel. Median CPI should be +0.22% or so, keeping y/y around 2.42%. At least it isn’t running away yet.

Also, NEXT month we roll off an 0.21% from the y/y figure. So the hurdle will be higher for an uptick in core CPI.

Like I said, thin gruel. There can be no doubt whatsoever that deflation risks are zero for the foreseeable future.

Stocks are doing tremendously well with this, only -9 points or so S&P futures. This is awful news for equities.

…but some observers like to spin “rising inflation” as “sign of robust growth.” Nope. See “1970s” in your encyclopedia.

The only way this is good news is if you recently wrote a book on inflation. Which, as it turns out, I did.

Distribution of price changes. You can be forgiven for seeing this as giving the Fed the finger.

User rating: 0.00

User rating: 0.00% (

0

The Complete List Of Wilshire 5000 Stocks

The Complete List Of Wilshire 5000 Stocks

Future Market Returns = Dividend Yield + Earnings Growth +/- Change In P/E Ratio

Future Market Returns = Dividend Yield + Earnings Growth +/- Change In P/E Ratio

USD/JPY Making A Bullish N Pattern Through Chuvashov Fork

USD/JPY Making A Bullish N Pattern Through Chuvashov Fork

Ebay Rises As Morgan Stanley Double Upgrades On Payments Shakeup

Ebay Rises As Morgan Stanley Double Upgrades On Payments Shakeup

The Pension Crisis Gets A Catchy Name: “Silver Tsunami”

The Pension Crisis Gets A Catchy Name: “Silver Tsunami”