Greetings,

Let’s begin with a few developments in Japan.

1. Dollar-yen fell below 111 as the yen continues to strengthen.

Source: barchart

This is in spite of the BoJ suggesting that the central bank could push rates deeper into negative territory.

Source: MarketWatch

2. Here is the Nikkei 225 response to the yen strengthening,

Source: barchart

3. Just like Germany, Japan’s government can now make money issuing bonds. Here is the 10yr JGB auction.

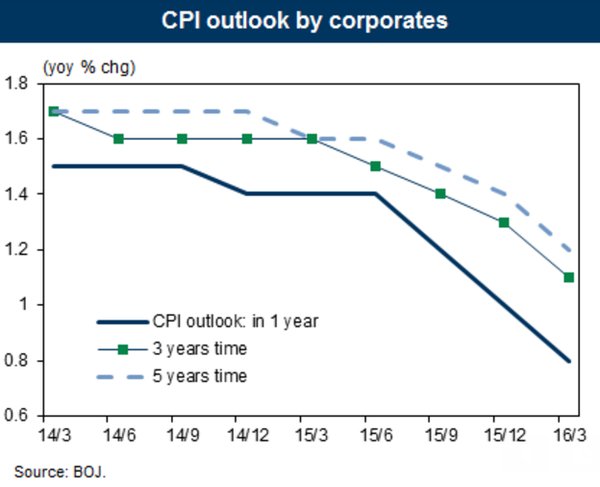

4. Inflation expectations in Japan remain subdued. Here are the corporate inflation expectations as determined by the BoJ.

Source: Goldman Sachs

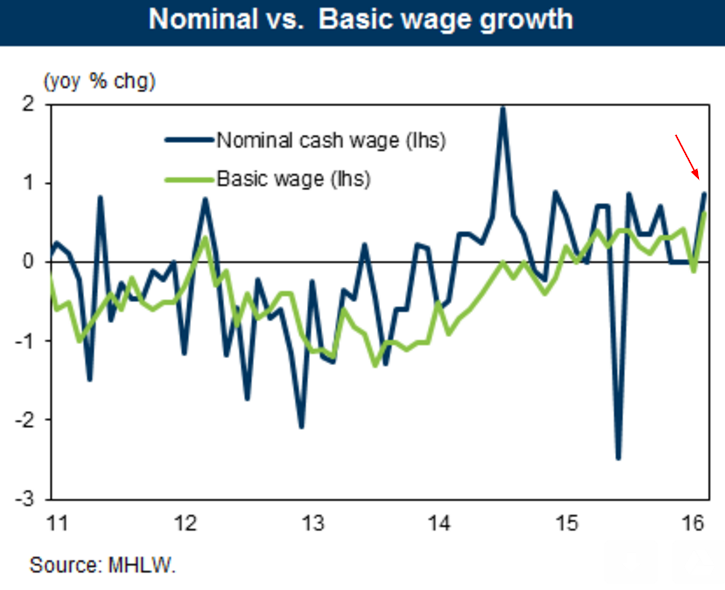

5. One positive development out of Japan is a boost in wage growth. It remains to be seen just how sustainable this is.

Source: Goldman Sachs

Next, we have a couple of trends from China.

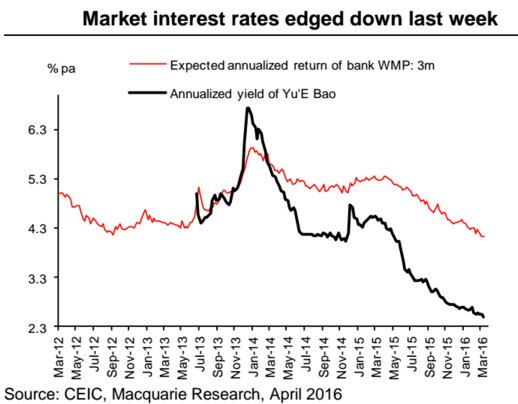

1. Rates offered to China’s consumer (Yu’E Bao is China’s largest money-market fund) continue to decline. This is driven by the persistent demand for yield, boosting the volume of wealth management products.

Source: Macquarie

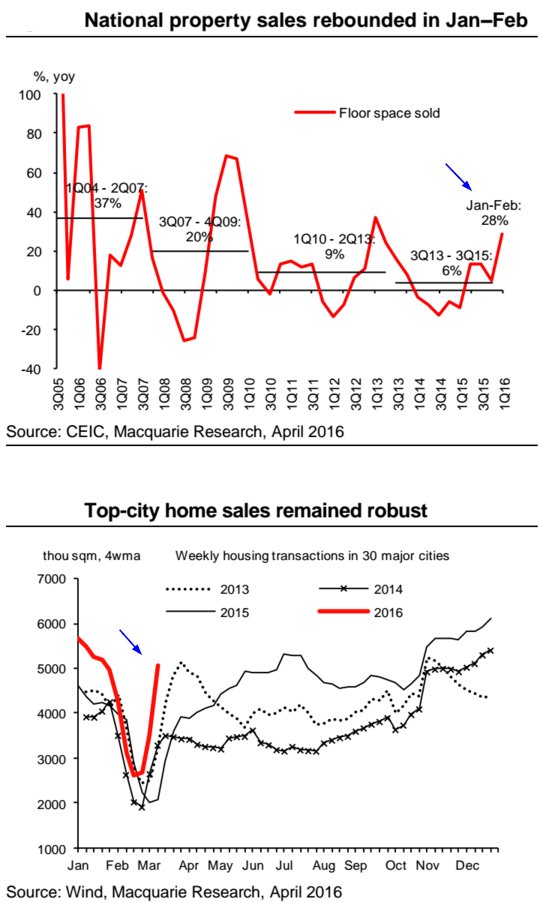

2. We now see more evidence of the rebound in China’s housing market.

Source: Macquarie

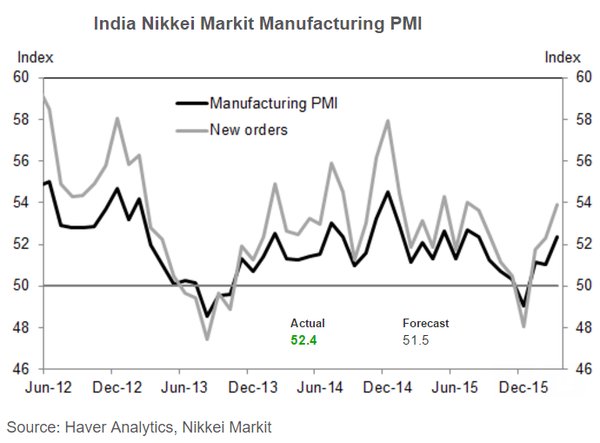

Turning to India, the nation’s manufacturing activity recovered last month.

Source: Goldman Sachs

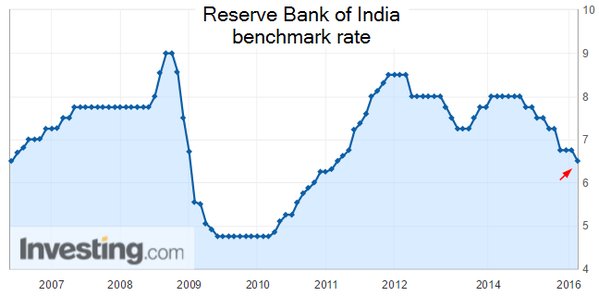

India’s central bank, the RBI, cut rates by 25bp (discussed here recently). The rupee gave up 50bp against the dollar in response, but otherwise the cut was largely expected.

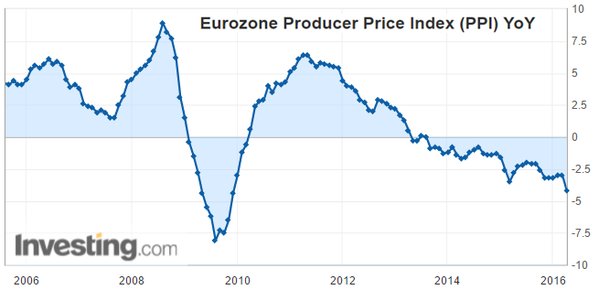

We now turn to the Eurozone where deflationary risks persist. The currency bloc’s wholesale price declines are accelerating.

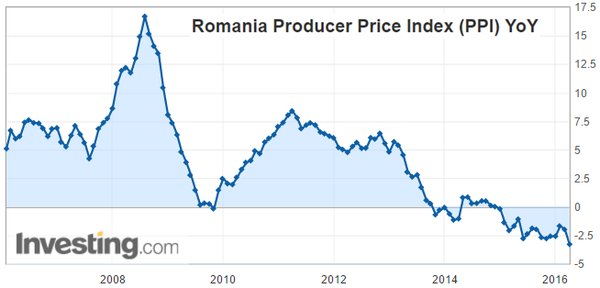

It’s important to note that the PPI deflation is not limited to the Eurozone. Here is Romania’s PPI for example.

In other Eurozone developments, …

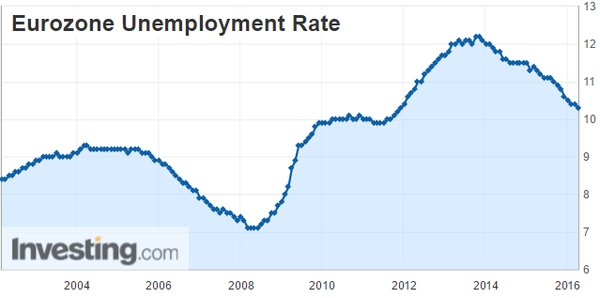

1. The Eurozone’s labor market improvement remains tepid. The unemployment rate, while gradually declining, is still above 10%.

2. German factory orders unexpectedly fell as a result of the recent slowdown in exports.