It Wasn’t Supposed to Do That…

When you’re a central banker in a pure fiat money system and even your ability to print your own currency into oblivion is questioned by the markets, you really have a problem. This is actually funny on quite a number of levels if one thinks about it a bit…

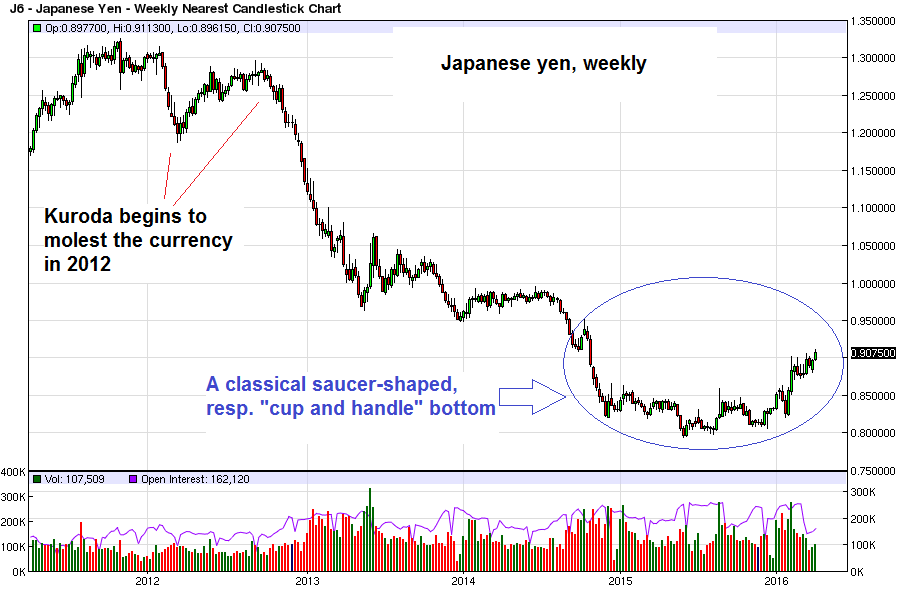

Haruhiko Kuroda (a.k.a. Kamikaze) is such a central banker. His valiant attempts to make Japan richer by making its citizens poorer is beginning to be rejected by Mr. Market:

Kuroda-san’s latest monetary depredations continue to backfire (from his perspective, that is). The chart of the yen actually continues to look quite bullish here – it is in the process of breaking out and has just attained a new 17 month closing high – click to enlarge.

Yes, operation DTY (Destroy the Yen) has been rudely interrupted. It worked for quite a while, but not anymore (or not anymeure, as Clouseau would say). Looking at a weekly chart, one can see a classic saucer-shaped bottoming formation in the yen, which has to look extremely inviting to hedge funds, CTAs, etc. employing technically oriented trading strategies – and there are quite a few of those out there.

The yen, weekly, over the past five year. The BoJ under Mr. Kuroda at first succeeded in driving it lower, although the move probably owed far more to the markets pricing out extreme macro risks such as an imminent euro zone blow-up than to the BoJ’s so-called “efforts”. Central planners and their claqueurs always like to imagine that things happen solely because of what they are doing, but that is of course complete rubbish – click to enlarge.

Given the market’s “muscle memory” of the negative correlation between the yen and the Nikkei, Japanese stocks have been under quite a bit of pressure of late. So what can one conclude from all this? That is actually quite simple: Kuroda-san is going to adopt even more extreme monetary policies.

This conclusion is based on the general Keynesian principle that if a policy fails to bring about the desired results and in fact brings about the exact opposite of what it was supposed to achieve, it must mean you haven’t done enough of whatever it is you’ve been doing.

So the fact that Japan has amassed the by far biggest debt load of all developed nations, has gone through so many iterations of “QE” that we’ve lost count, and has failed to achieve even a single one of its economic and monetary policy aims in 26 years running, doesn’t mean these policies are misguided. It only means they must be implemented in even grander style.