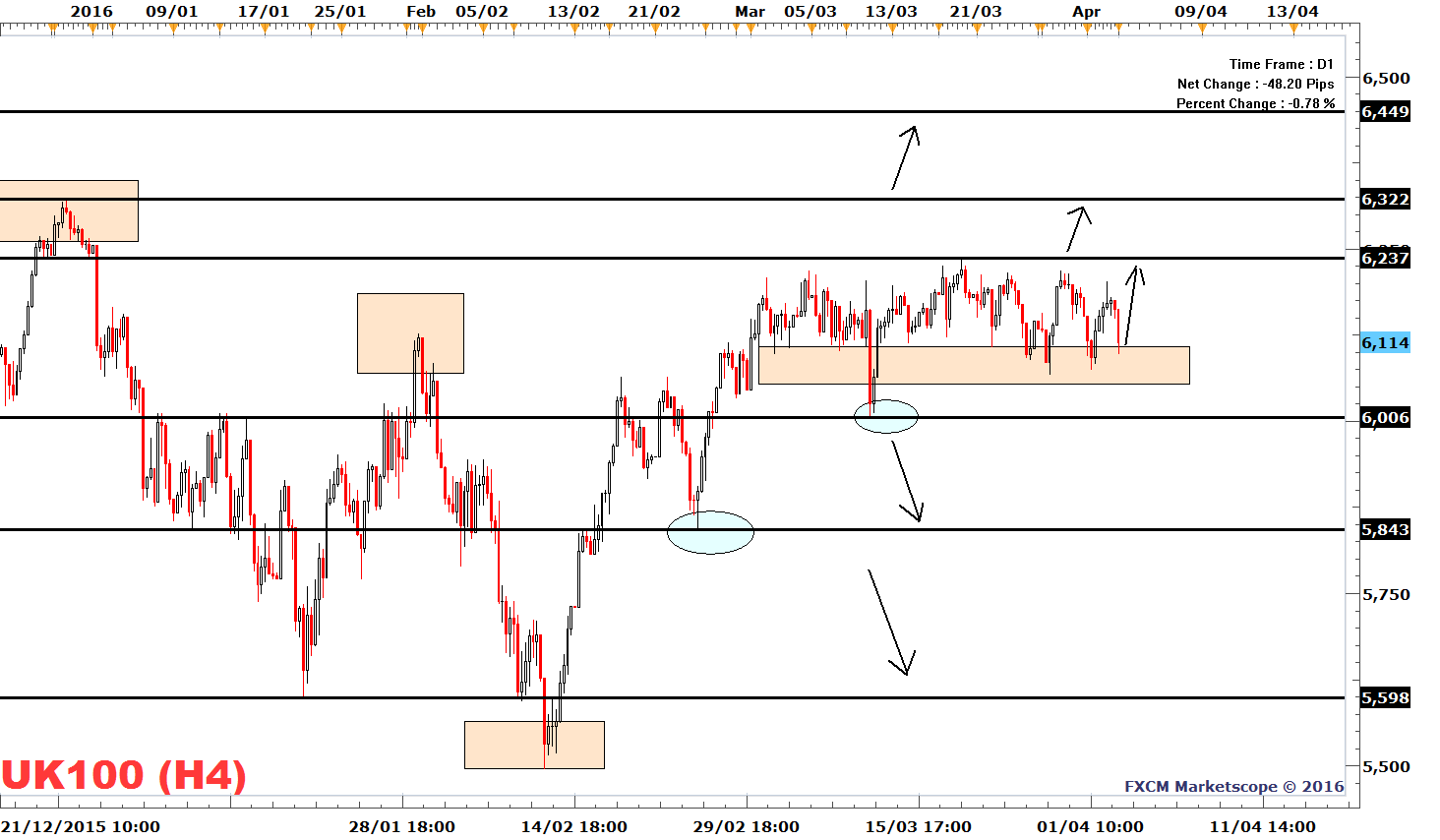

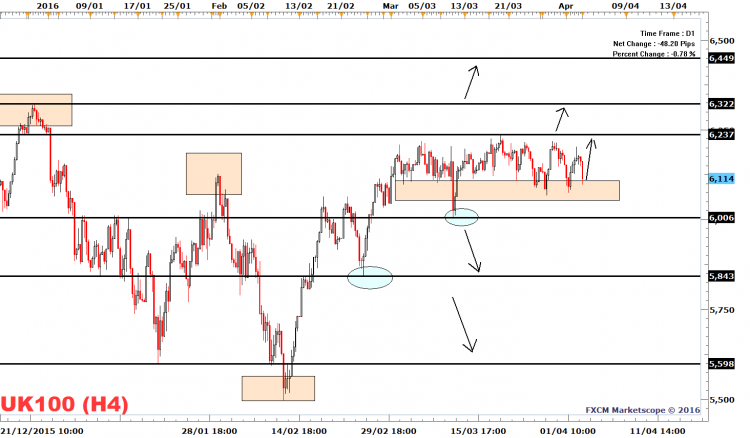

The FTSE 100 (FXCM: UK100) is once again spending another day in the narrow price range of 6006 to 6237, making it a total of 24 trading days since the formation of the range.

While a narrow range like the current does not tend to draw attention and excitement from traders, when the range finally breaks, they nevertheless tend to hurry to get involved.

Which way price may break is hard to know until it is a fact. However, we are able to note the following resistance levels above the upper limit of 6236, namely the December 29 high of 6322 and the psychological level of 6400. Support beyond the lower limit of 6006 are both the February 25 low of 5913, followed by the January 24 low of 5843.

On an intraday basis, the FTSE 100 is currently down by 0.78%, which appears to be an adjustment to soft Asian stock markets overnight. The business press cites soft crude oil prices and positioning ahead of Wednesday’s FOMC minuets as a possible explanation to the softer Asian stock markets. We note that Brent crude prices are lower by about roughly 12% after reaching a high of $42.5 dollars per barrel on March 18.

Potential Market Movers

Markit/CIPS UK Services PMI for March is projected to have risen from 52.8 to 53.4 according to a Bloomberg news survey. In the afternoon we can look towards U.S. Trade Balance and ISM Non-Manufacturing results, with the latter likely grabbing most of the attention given that it gives us hints about the state of the important U.S. service sector. Economists project the ISM Non-Manufacturing results to have gained to 54.1 from 53.4.

FTSE 100 | FXCM: UK100