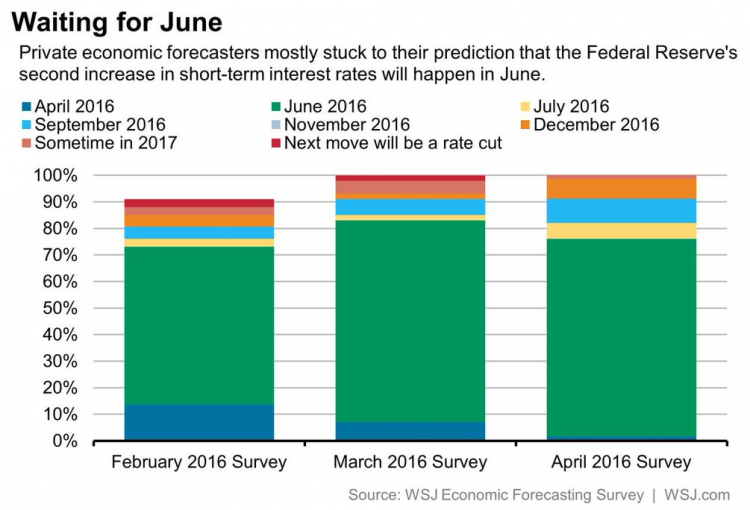

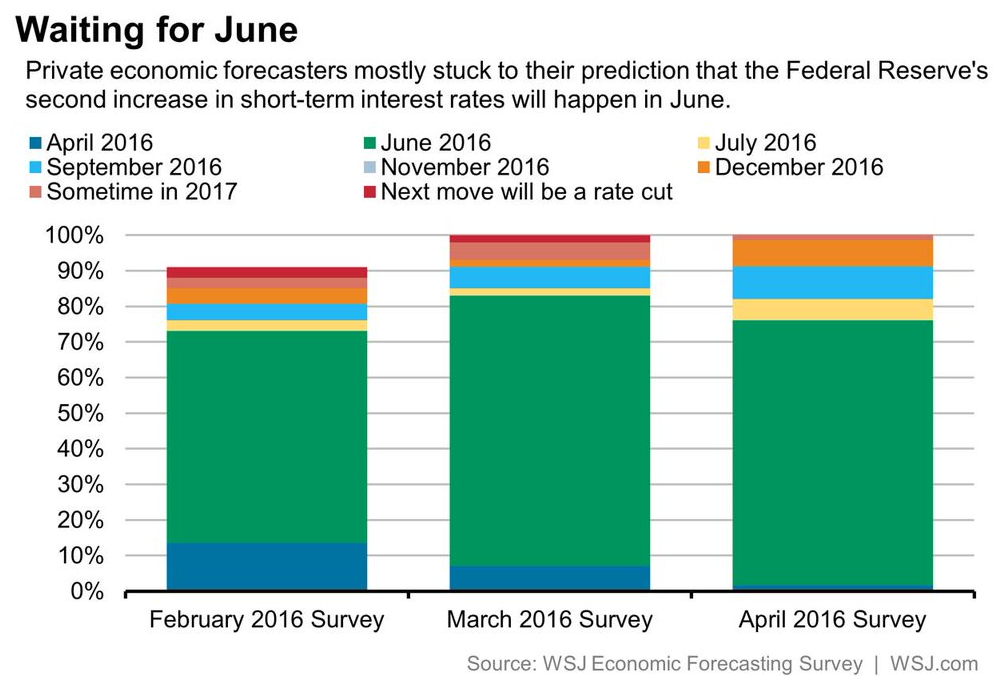

This Great Graphic shows the results of the last three Wall Street Journal survey of business and academic economists on the outlook for Fed policy. The key take away is that despite all the talk and ink spilled on the shifting Fed stance and the split within the FOMC, economists views did not change much over the past month.

In March, 76% of the economists expected the next hike in June. In the April survey that was completed earlier this week found 75% expect a June hike.Only one saw an April hike.Four did in March. Only one saw the next move being in 2017 and only one thought that Fed was one and done.

The June Fed funds futures has nothing like the survey results discounted.Here is the math:

1.Assume that for the first fifteen days of June, Fed funds averages what is currently is, which is 37 bp.(15*37).

2.Assume that on June 15, the Fed hikes the target range 25 bp and that the Fed funds averages 62 bp for the remaining 16 days (16*62).

3.((15*37)+(16*62))/31 equals 49.90, which is what Fed funds would be expected to average over the course of June, assuming the rate hike.

4.The difference between no change and a 25 bp hike is 49.90-37.00 or 12.9 bp or 13 bp.

5.The June contract currently implies a 39 bp, which is 2 bp of the possible 13 bp.This is roughly discounting a 15.4% chance or 15% chance of a hike at the June meeting.

If one assumes that, perhaps due to the UK referendum, a possible Spanish elections and/or market turmoil, the Fed’s caution leads it to not hike rates in June, but wait until December, after the US election, what then?

The math is nearly identical as the December FOMC meeting concludes on the 14th. Fair value for the December contract, assuming a hike then is 50.7 bp or 51 bp.This is exactly where the contract is trading presently.