Skill is a slippery concept in finance, courtesy of the shady influence of chance in asset pricing. It’s also an awkward topic in just about every corner of money management because discussing it in detail invariably raises serious doubts about our ability to engineer investment results that are satisfactory much less stellar. But ignored or not, randomness is a factor and perhaps a far more powerful one than generally assumed.

In recent posts I’ve explored several facets of how random market behavior can influence portfolio results. In the first installment on the topic we focused on random rebalancing dates. Then we moved on to the results via randomly changing asset weights in asset allocation. Let’s push this testing a step further and build portfolios by randomly selecting asset classes.

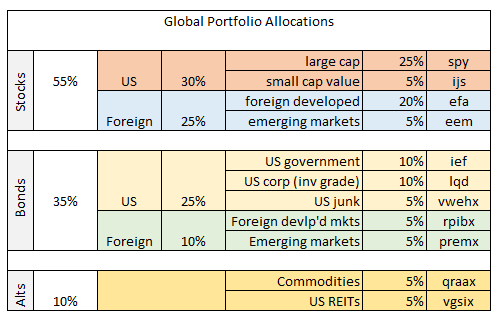

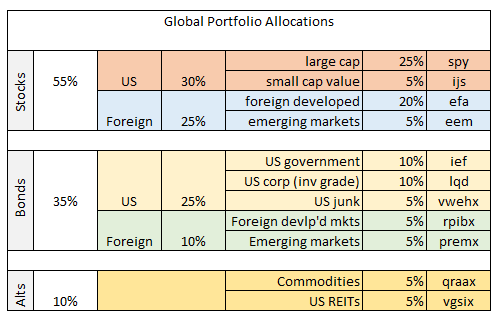

As before, I’ll use the same 11-fund portfolio that’s globally diversified across key asset classes with a starting date of Dec. 31, 2003. The benchmark strategy is rebalancing the portfolio at the end of each year back to the initial weights, as defined in the table below. Let’s call this our “reasonable” attempt at building an informed asset allocation strategy.

For comparison with the element of chance in market pricing, this time the test consists of randomly selecting combinations of asset classes with equal weighting that rebalances the mix back to equal weights every Dec. 31. Note that there are 11 funds in the table above. To test for randomness I’ll use R’s number-crunching prowess to select 1,000 different asset allocation mixes. For instance, one randomly selected portfolio may hold US stocks, US REITs, and commodities and ignore everything else. Another portfolio may hold everything with the lone exception of US junk bonds. (For those who’re interested in the details, I’m selecting time series data via the sample() command with no replacement.) All random portfolios are created as equal weight strategies (if there’s more than one fund) using a start date of Dec. 31, 2003, with results running through yesterday’s close (Apr. 6).