For most folks, earnings season means the 4 to 6 week period at the end of each calendar quarter when announcements of quarterly earnings releases dominate market headlines. For folks like us, however, who have to monitor and record each and every earnings release, the definition and duration of each earnings season isn’t that simple. Take for example, the 161 companies coming out with quarterly results this week, including 4 S&P 500 members.

Since we are still a couple of weeks away from the end of the March quarter, most folks would assume that all of these reports represent the tail of the 2016 Q4 earnings season. But that’s not correct; not all of this week’s earnings releases fall in the Q4 bucket. In fact, a number of this week’s earnings releases form part of the Q1 earnings season. For example, the Oracle (ORCL – Free Report) report after the market’s close on Wednesday is for that company’s fiscal quarter that ended in February, which will form part of our Q1 earnings tally. The Adobe (ADBE – Free Report) report after the close on Thursday similarly becomes part of the Q1 bucket.

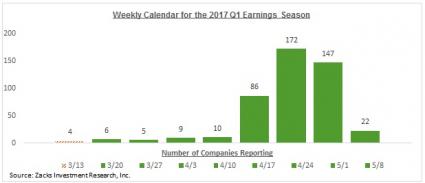

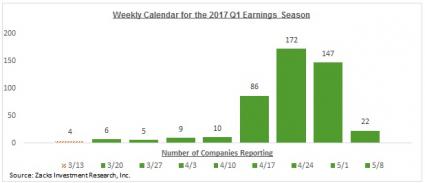

That said, most of this week’s 161 earnings releases do represent the tail of the Q4 reporting cycle. The chart below of weekly reporting calendar for the S&P 500 index clearly shows that we still have another four weeks to go before the Q1 earnings season really takes off.

Expectations for Q1

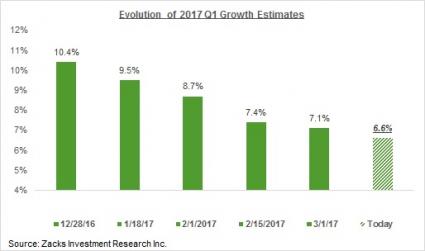

Total Q1 earnings are expected to be up +6.6% from the same period last year on +6.5% higher revenues. This would follow +7.4% earnings growth in 2016 Q4 on +3.7% revenue growth, the highest growth pace in all most two years.

Estimates for Q1 came down as the quarter unfolded, with the current +6.6% growth down from +10.4% at the end of December. The chart below shows how Q1 earnings growth expectations have evolved over the last three months.

Please note that while Q1 estimates have followed well traversed path that we have been seeing consistently over the last few years, the magnitude of negative revisions compares favorably to other periods. In other words, Q1 estimates have come down, but they haven’t come down by as much.

The table below shows the summary picture for Q1, contrasted with what was actually achieved in Q4 (please note that we have not officially closed the books on Q4 yet, as four index members still have to report quarterly results).