European bourses advance and Asian share rose led by a surge in Hong Kong stocks which rose the most in three months as Japan hit 15 month highs. U.S. futures are little changed along while the dollar rebounded from session lows after Friday’s selloff. Crude oil has continued its retreat, down 0.2% and sliding for a 6th straight day after breifly dropping below $48 in overnight trading.

The Hang Seng China Enterprises Index jumped the most since November amid easing concern that U.S.-China political tensions will weigh on the yuan after BlackStone’s Steve Schwarzman, one of Trump’s top economic advisers, said Sunday on CNN that Trump will likely temper his criticisms of China, including his campaign claim that the country manipulates its currency. South Korean equities rose to the highest since May 2015 following last Friday’s impeachment of president Kim, while European shares headed for a fourth straight gain. The dollar fell against most major currencies, with the euro climbing for a third day. Oil kept sliding below $50 as U.S. drillers continued to boost activity, countering OPEC’s efforts to drain a global glut. Industrial metals advanced for a second day.

Traders are tentative out of the gate ahead of a pivotal week for global markets with the focus falling on Wednesday when there is a trifecta of catalysts between the Fed’s upcoming rate hike, the debt ceiling expiration and the Dutch general elections which comes amid a growing diplomatic spat with Turkey. In addition to the Fed, we will also get announcements by the BoJ, BoE and SNB all of which are expected to keep rates on hold. It’s also possible that the UK could invoke Article 50 this week so another story to watch. President Trump may also dish out his first budget outline for fiscal year 2018 on Thursday while G-20 finance ministers gather in Germany for a series of meetings so there’s plenty to keep markets busy.

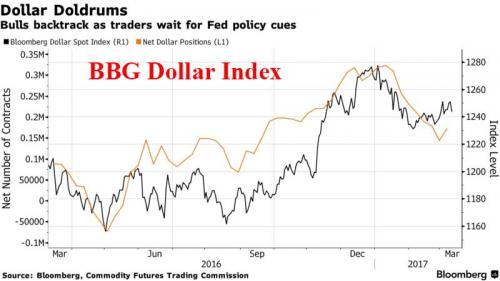

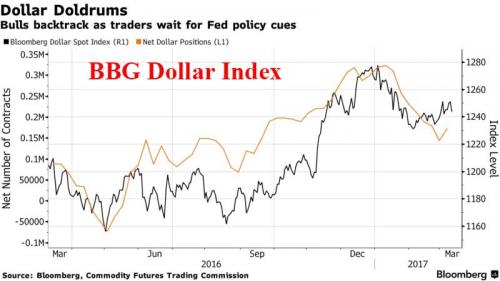

Following last week’s impressive payrolls reports, global equities are trading near a record high as indications of firming growth in the U.S. and Europe coincide with China’s economy showing signs of improvement. U.S. jobs data at the end of last week cleared the way for the Fed to raise interest rates without forcing it to accelerate the pace for future tightening. The euro built on gains from Friday, when European Central Bank policy makers were said to have considered their ability to raise rates before a bond-buying program comes to an end, although the common currency has erased all losses after the European open, and was back near session lows at publication time.

By now it is no secret that traders view a quarter-point Fed hike this week as a virtual certainty after Friday’s data showed U.S. employers added more jobs than forecast in February. They’ll be watching the central bank’s policy decision for signals on what will come next. Futures indicate the market is moving toward policy makers’ December projection of three rate increases in 2017. It would be the first year with multiple Fed hikes since 2006. Fed fund futures prices showed investors pricing in more than a 90 percent chance of an increase in U.S. overnight interest rates and the market’s attention is now firmly on the scale of tightening further out.

“Improved growth and inflation prospects are allowing developed market central banks to sketch their exits from extreme accommodation at varying speeds,” David Folkerts-Landau, group chief economist at Deutsche Bank wrote in a note to clients.

Overnight Goldman flip-flopped on its long-standing bearish position over Chinese stocks, and joined the rush on Chinese shares, becoming the latest major brokerage to upgrade the market. China’s macroeconomy stabilized in the beginning of 2017, Ning Jizhe, head of the National Bureau of Statistics, said at the sidelines of the annual legislature meeting in Beijing on Sunday.

Sterling rose 0.4% against the dollar ahead of a vote in Britain’s lower house of parliament on legislation that will give the government permission to trigger Britain’s exit from the European Union. “The push and pull between solid growth momentum and political risks look set to continue in the near-term,” Folkerts-Landau said.

The world’s most powerful finance ministers and central bankers convene in the German spa town of Baden-Baden on March 17-18, their first meeting since Donald Trump’s U.S. election victory in November where his protectionist stance on international trade is likely to be a key issue.

The MSCI Asia Pacific Index advanced 0.7 percent as of 8:17 a.m. in London. The Hang Seng China Enterprises Index surged 1.9 percent, the biggest jump since Nov. 22. Japan’s Topix rose 0.2 percent, after the gauge rallied 1.2 percent on Friday to the highest level since December 2015.The Kospi index jumped 1 percent, led by a 1.1 percent gain in Samsung Electronics Co. Korean shares extended gains from last week, climbing as President Park Geun-hye’s ouster removes some uncertainty from politics in the nation. The Stoxx Europe 600 added less than 0.1 percent, after similar gains in each of the previous three sessions.

Gains in mining stocks and continued corporate deal-making activity helped European shares offset weakness in oil-related shares, with the benchmark STOXX 600 up 0.2 percent in early trades. The FTSE 100 was up slightly where along with mining blue chips a 1 percent gain for shares of HSBC supported the index. HSBC shares rose after Europe’s biggest bank tapped an outsider, Mark Tucker, for its top job.

In bond markets, euro zone government bond yields pulled back from multi-week highs, as nervous investors turned their focus to this week’s Dutch parliamentary elections, the next key gauge of populism in Europe.Although the risk of a eurosceptic party coming to power in the Netherlands is small, a strong election performance could renew concerns about the popularity of the far-right in French presidential elections in April and May, said Erin Browne, head of macro investments at UBS O’Connor, a hedge fund manager within UBS Asset Management.