Credit Suisse is out with a new Global Equities Strategy update.

Now who’s excited?!

No, but seriously, there’s a lot to like about this latest installment from Andrew Garthwaite and team.

Specifically, there’s a lot about the eurozone and the French elections that’s definitely worth a read and the section on Japan isn’t a complete waste of time either.

Of course US investors are a myopic bunch and if most retail investors had their way, there wouldn’t be any markets other than those that are open from 9:30 a.m. EST to 4:00 p.m. EST Monday through Friday.

So because I aim to please, I wanted to highlight the bank’s comprehensive look across US equity markets. And because I also aim to disappoint by raining on the “buy every dip in US stocks” parade, I think all of what you’ll read below is worth noting for what it says about how things are likely to turn out for anyone buying into a market the bank describes as “scoring at the bottom of the scorecard.”

Via Credit Suisse

What are the challenges?

US equity underperformance has been rare in recent years, but year-to-date, US equities have underperformed global equities by around 0.7% in USD terms. We reiterate our underweight stance, and view the challenges for US equities in a global context as the following:

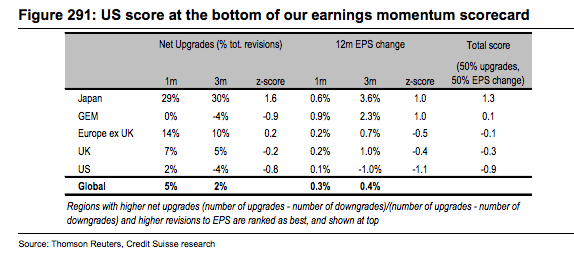

1) The US scores at the bottom of our scorecards. The US scores at the bottom of our composite scorecard, as shown in the overview of this regional update (see Figure 1). This is primarily a result of high relative valuations and low earnings momentum, with the US now at the bottom of our earnings momentum scorecard, as shown below.

2) Relative valuation is unattractive. US equities account for 53% of the MSCI AC World thanks to the relative rally in the underlying equity index, combined with the move higher in the US dollar since 2011. As a result, US equities as a share of market cap are above their late-1990s peak when compared with the DM-centric MSCI World, or just a couple of percentage points below their peak when compared with AC World.

This period of outperformance has, however, left US equities at historically high valuations relative to the rest of the world, which we show below in terms of Credit Suisse HOLT P/B relative (now around 2 standard deviations extended), as well as a simple 12-month forward P/E.