Economic growth is expected to slow in next week’s first-quarter GDP report, but the probability remains low that a new recession has started.

The government’s big-picture update due on Apr. 28 may suggest otherwise, based on recent polling. The median estimate for the “advance” GDP report via CNBC’s Rapid Update survey of economists (as of Apr. 18), for example, sees Q1 output rising by just 0.9% — less than half the 2.1% pace in last year’s Q4. If the projection is accurate, the news will inspire new claims that the US macro trend is sliding over to the dark side. Anything’s possible, of course, but a review of the numbers published to date across a broad range of indicators signals that forward momentum is intact, even if the upcoming GDP results look wobbly.

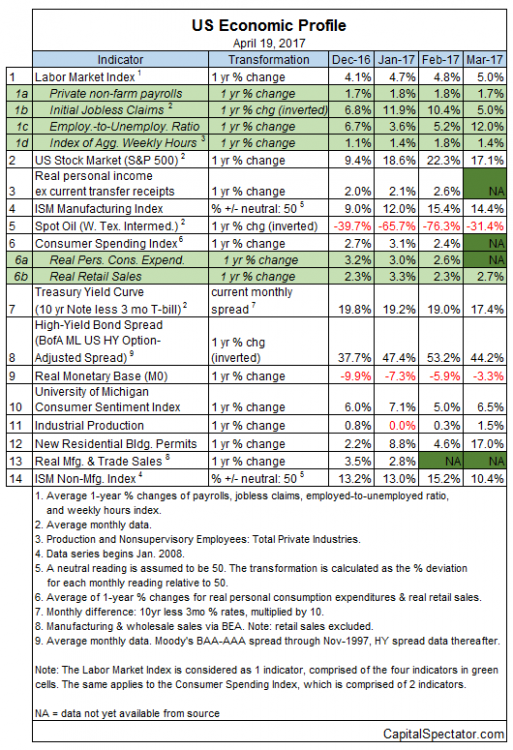

The probability of an NBER-defined recession has started is still close to zero, based on numbers through March via the Capital Spectator’s proprietary business-cycle indexes. The nearly complete profile for last month shows that just two of 14 indicators in our model are negative, which implies that the economy will continue to sidestep a new downturn. (For a more comprehensive read on business-cycle analysis on a weekly basis, see The US Business Cycle Risk Report.)

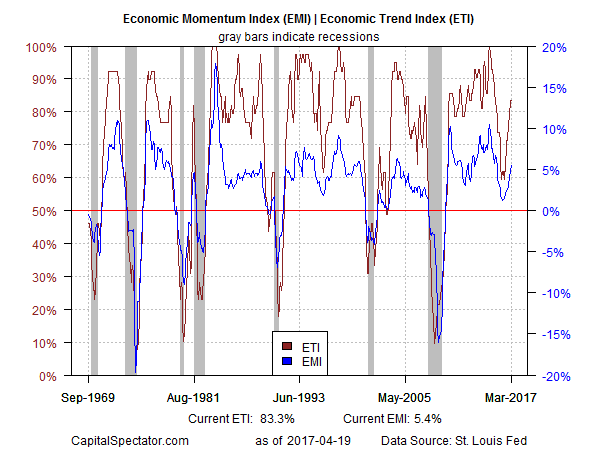

Aggregating the data in the table above continues to indicate that the broad trend remains convincingly positive. The Economic Trend and Momentum indices (ETI and EMI, respectively) were unchanged in March, holding on to gains that unfolded in previous months. As a result, both benchmarks remain well above their respective danger zones: 50% for ETI and 0% for EMI. When/if the indexes fall below those tipping points, we’ll have clear warning signs that recession risk is at a critical level, in which case a new downturn will be likely. The analysis is based on a methodology outlined in my book on monitoring the business cycle.

Translating ETI’s historical values into recession-risk probabilities via a probit model also points to low business-cycle risk for the US through last month.Analyzing the data with this methodology indicates that the odds are virtually nil that NBER will declare March as the start of a new recession.