There were a number of articles about the scary news that debt levels are again above their housing bubble peaks. If you need something to be scared about (really?) I suppose you can worry about this, but if you want to seriously consider the economic impact of this data point, there ain’t much there.

There are two big differences between now and our previous peak ten years ago. One is that the economy and income is considerably higher today. The other major difference is that interest rates are considerably lower on average than they were ten years ago.

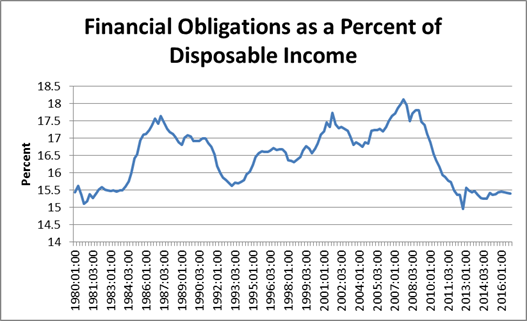

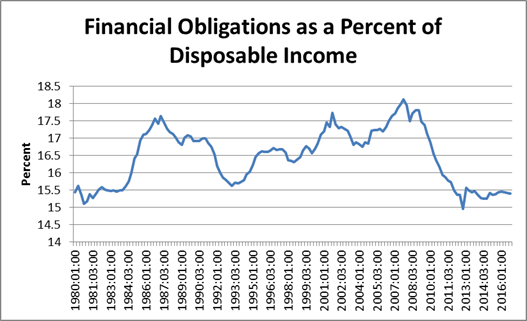

We actually have a very good summary statistic from the Federal Reserve Board that tells us the burden of the debt level. It is called the “financial obligations ratio.” It measures the ratio of debt service payments, plus rent, to disposable income. (Rent is included since rent and mortgage payments can be seen as substitutes.)

Here’s the story since they started the series in 1980.

Source: Federal Reserve Board.

As can be seen, at 15.4 percent, this ratio is near its low point for the last four decades. It is far below the peaks hit during the housing bubble years. In other words, there is little reason to worry about debt burdens suddenly creating a massive drag on the economy and leading to the sort of financial crisis we saw when the housing bubble collapsed.

This doesn’t mean that many people are not struggling to cope with student loans and other debts. Household income has barely recovered from pre-crisis levels and many families are still worse off than they were a decade ago. That’s a really bad story, but it doesn’t mean a financial crisis is imminent.

Can the picture change if interest rates rise? Sure, but not very quickly. (Most of this debt is fixed rate mortgage debt.) Furthermore, how much do we expect rates to rise and how quickly?

The long and short is that many people (not me) were caught sleeping by the run-up of debt in the housing bubble years. They aren’t making up for it by worrying about debt now, they are just being wrong again.