As we get into the midst of the Q2 earnings season, we can take a closer look at the results through the 1st quarter of the year. Despite the exuberance from the media over the “number of companies that beat estimates” during the most recent reported period, 12-month operating earnings per share rose from $106.26 per share in Q4 of 2016 to $111.11 which translates into an increase of 4.56%. While operating earnings are widely discussed by analysts and the general media; there are many problems with the way in which these earnings are derived due to one-time charges, inclusion/exclusion of material events, and outright manipulation to “beat earnings.”

Therefore, from a historical valuation perspective, reported earnings are much more relevant in determining market over/undervaluation levels. It is from this perspective the news improved as 12-month reported earnings per share rose from $94.55 in Q4 of 2016 to $100.29, or 6.07% in Q2.

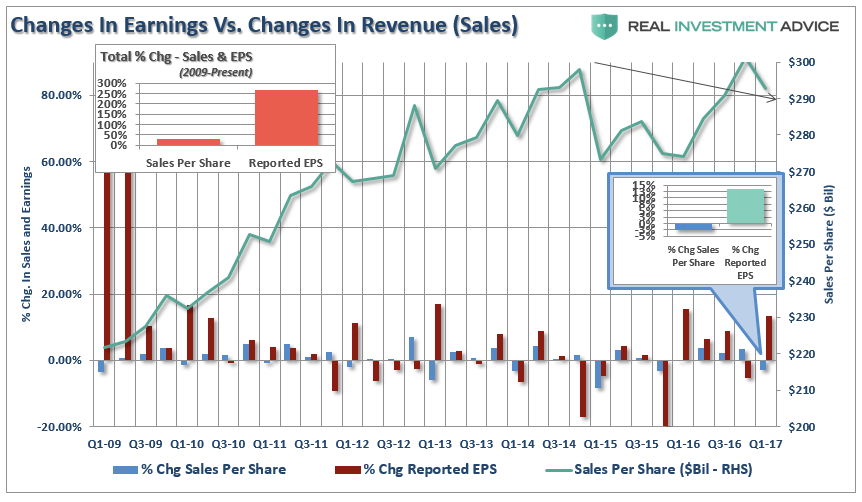

However, despite the improvement in reported earnings for the quarter, the thing that jumped out was the decline in revenues which slumped from $301.12/share in Q4 to $292.78/share in Q1. This was a decline of -2.77% for the quarter.

In other words, while top line SALES fell, bottom line revenue expanded as share buybacks and accounting gimmickry escalated for the quarter.

Earnings Manipulation Reaching Limits

There is no arguing corporate profitability improved in the first quarter as oil prices recovered. The recovery in oil prices specifically helped sectors tied to the commodity such as Energy, Basic Materials, and Industrials. However, such a recovery may be fleeting as the dollar remains persistently strong which continues to weigh on exports and the recovery in oil prices continues to remain muted.

Furthermore, as stated previously, the decline in oil prices during Q2 puts earnings estimates at risk. To wit:

“First, with respect to oil, the bounce in oil following the crash in prices that began in 2014 resulted not only in the bulk of the decline in earnings initially but also the recovery in earnings with the bounce. However, that bounce has now faded but forward earnings expectations have likely not been revised lower. Per FactSet, the energy sector is expected currently to post a 396% gain in earnings on a year-over-year basis. Given the recent fall in oil prices, there is a huge risk of disappointment.”