Crown Castle (CCI) only began paying dividends in 2014, but the company currently offers income investors a dividend yield that’s nearly twice as high as the market’s with 7% to 8% annual dividend growth potential.

More importantly, Crown Castle has an attractive business model with substantial recurring revenue, excellent free cash flow generation, substantial barriers to entry, and extremely high incremental margins.

These are all likely reasons why Bill Gates’ investment manager holds a meaningful stake in Crown Castle. You can view Bill Gates’ complete dividend portfolio here.

Let’s take a closer look at Crown Castle’s business to see if this company deserves to be in our list of the best high dividend stocks.

Business Overview

Founded in 1994, Crown Castle began operating as a real estate investment trust (REIT) in 2014 for tax purposes and is the largest provider of shared wireless infrastructure in the country.

Crown Castle owns approximately 40,000 towers and 26,500 miles of fiber supporting small cell networks (expected to grow to 60,000 miles post the Lightower acquisition). The company also has a small cell platform with 50,000 small cell nodes on air or under deployment.

The company leases its towers out to wireless carriers, which need Crown Castle’s infrastructure to provide wireless services to consumers and businesses.

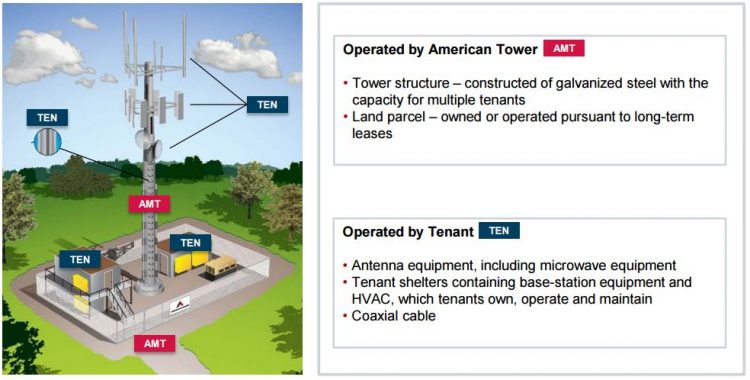

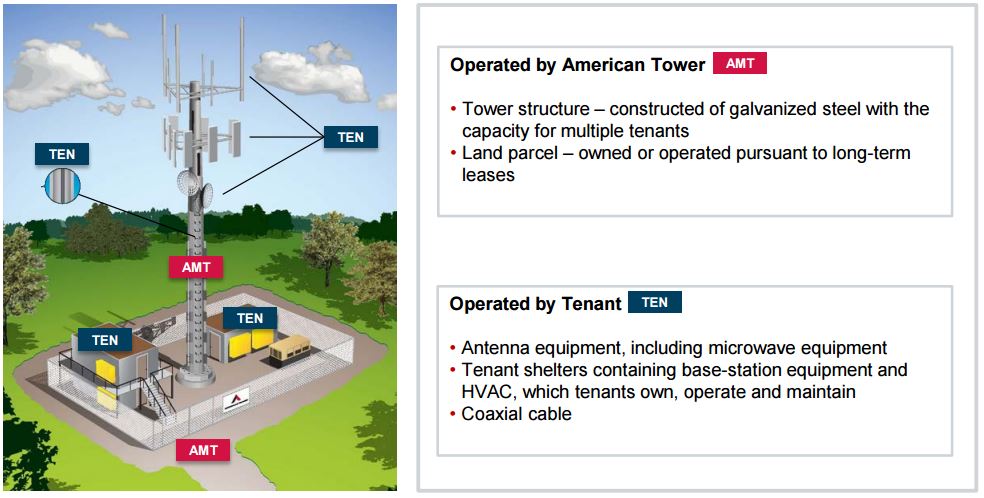

Tenants deploy communications equipment, coaxial cables, and antennas at the top of Crown Castle’s towers that transmit signals between the tower and mobile devices. Most towers have the capacity for at least four tenants.

Here’s a look at the tower setup, courtesy of Crown Castle’s competitor American Tower (AMT):

Source: American Tower Investor Presentation

The big four wireless carriers account for 90% of Crown Castle’s site rental revenue, and the company is completely focused on the U.S. wireless market, where over 70% of its towers are located in the top 100 largest markets.

Over 80% of the company’s revenue is recurring, and most of its site rental revenue results from long-term leases with initial five to 15-year terms and five to 10-year renewal periods thereafter.

Business Analysis

Despite its customer concentration, Crown Castle’s business model is attractive for a number of reasons, beginning with its predictability.

The company has an average remaining customer contract term of six years and approximately $19 billion remaining in contracted lease payments (compared to $3.2 billion in 2016 site rental revenue), providing excellent cash flow visibility.

Crown Castle’s leases also have built-in price escalators, which are expected to continue adding around 3% to the company’s annual earnings growth.

In addition to annual rent escalators, tower economics are also attractive because very little cost is involved to add additional tenants.

An investor presentation by Crown Castle last year highlighted that the company enjoys a 96% incremental margin when it adds an additional tenant to one of its existing towers, for example.

In other words, if a new tenant brings in $25,000 of additional rental revenue, Crown Castle keeps $24,000 in gross profits. The operating leverage in this business is tremendous, and substantially all of Crown Castle’s wireless infrastructure can accommodate additional tenancy.

As data growth continues accelerating, it seems reasonable that demand for Crown Castle’s wireless infrastructure will also rise over time as carriers invest in their networks to handle increasing traffic.

Demand should also be helped as T-Mobile (TMUS) pours billions of dollars into improving its wireless network to better compete with Verizon (VZ) and AT&T (T).

Additionally, Sprint (S) is exploring merger deals with T-Mobile, Charter Communications (CHTR), and Comcast (CMCSA). A decision is expected soon.

Sprint has long been the weakest wireless carrier, but combining with a financially healthy partner would allow the company to make the investments necessary to provide more reliable service, boosting demand for the tower space provided by Crown Castle.

While consolidation can give carriers more bargaining power with tower operators, carriers still have no substitutes for wireless infrastructure, which is mission-critical for their businesses to operate.

Additionally, by collocating on shared wireless infrastructure, wireless carriers only have to pay for their proportional usage of the infrastructure.

Instead of needing to occupy an entire company-owned tower themselves, carriers can rent only the space they need to enhance their network coverage and continue servicing their customers.

As a result of these factors, tenant leases have historically enjoyed a high renewal rate. Non-renewals have averaged just 2% of site renewal revenues over the last five years.

Crown Castle has also been making strategic acquisitions which have helped in expanding its portfolio in some of the best markets in the U.S. Some of these recent acquisitions are Sunesys in Philadelphia and Southern California; FiberNet in Miami and Houston; and the Wilcon acquisition which has a similarly extensive footprint in Southern California.

The Wilcon acquisition will also increase Crown Castle’s fiber asset base in the fastest-growing market for small cells. The demand for small cells is higher in urban and suburban geographies where towers are not available or are not able to meet the high bandwidth requirements.