As US GDP growth rises at 3% or more for the second quarter in a row, French investment bank Natixis urges investors to prepare for the U.S. economy to “slow down substantially” as early as 2018.

Video length: 00:00:53

Patrick Artus, chief economist at Natixis, warned that the current level of corporate investment is “abnormally high” and suggested a downward correction.

“The US economy will in all likelihood slow down substantially: there is a limit to the rise in the participation rate and the employment rate; real wages are slowing down,“

Artus concluded:

“investors should therefore prepare for the consequences… If US growth slows down markedly … equity valuation and share prices will start falling.”

For now he is almost alone in the wilderness as Wall Street analysts are falling over themselves to extrapolate trends, call the death of the bond bull market, and declare escape velocity is finally here (but carefully noting that this has nothing to do with Trump at all…)

As Alhambra Investment Partners’ Jeffrey Snider notes, there’s even less inside the Q3 GDP report… especially where it counts.

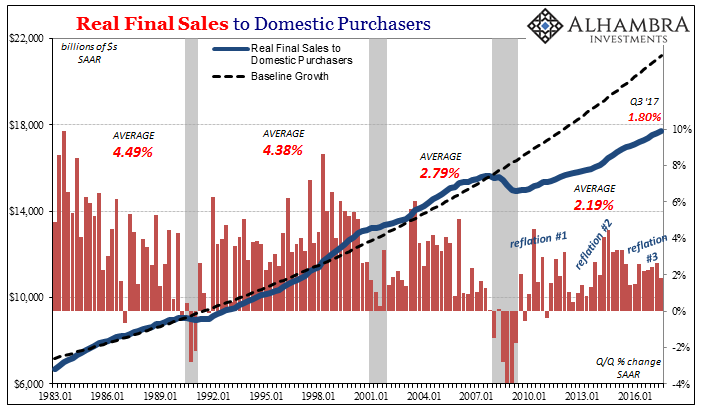

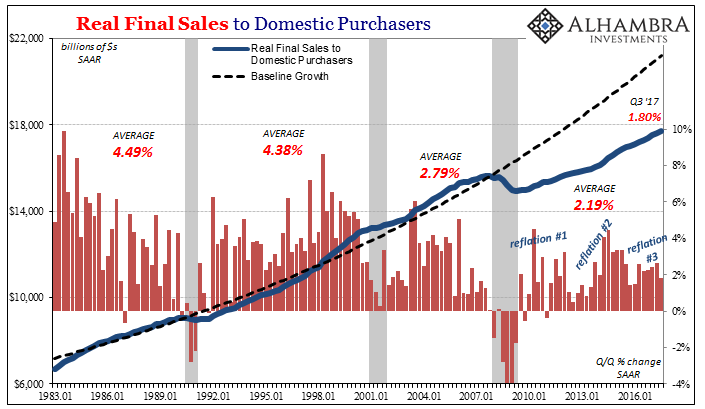

Inside the advance third quarter GDP report, the details in most of the important categories suggested slowing after two quarters consistent with “reflation” at least in its third try. If the economy swings between shallow downturns and often shallower upturns, these subcategories give us some insight as to why. Overall, growth remains at a level that is not growth, whether consumers or business investment.

Real Final Sales to Domestic Purchasers, a measure of US demand regardless of where the goods/services originated, increased by just 1.80% (Q/Q SAAR) in Q3. That was the lowest rate of expansion since Q1 2016 and the near-recession trough. It doesn’t bode well for future growth both as a reflection of incomes and the labor market but also the slight uptick in inventory detected by GDP also in the third quarter. That’s a potential problem for domestic producers as well as those overseas (China).