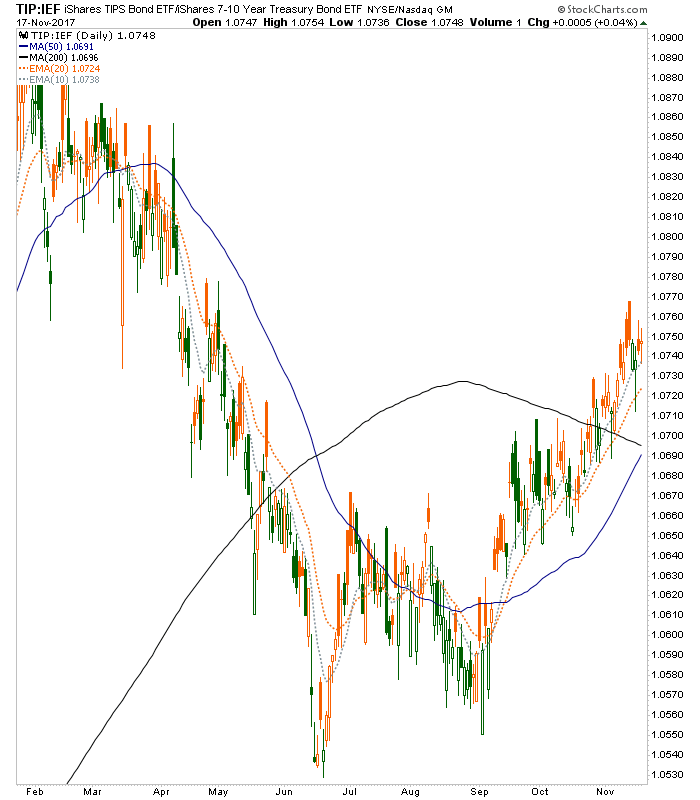

The TIP/IEF ‘inflation gauge’ is still motoring upward after breaking above the SMA 200. If this turns the 200 up along with the MA 50 it could indicate a mini hysteria about inflation.

The problem lately has been that the longest duration bonds have been relatively strong, putting a cap on yields and inflationary signaling, if not indicating deflationary pressure. TIP/TLT has not nearly kept up as 30yr yields have been a big drag over the last couple of weeks (this could still turn out to be a bottoming pattern though).

Of course, the Tin Foil Hat wearer in me wonders where some of this pressure might be coming from. Political and monetary authorities who have an interest in keeping long-term rates capped, maybe? Macro Tourist checks in with some details (last part of the article) about potential political shenanigans in the long-term Treasury bond market.

You Can’t Make This Shit Up

From WSJ:

The Treasury Department has unveiled a new strategy for managing federal debt that could ease pressures set to push up long-term interest rates and reduce a potential drag on the economy.

Under the plan unveiled earlier this month by Treasury, the department would increase the share of shorter-term debt issuance and reduce the share of longer debt issuance, ending a yearslong trend that favored long-term debt issuance.

Total issuance of government debt will still rise in coming years with growing federal budget deficits. As that supply increases, it is likely to weigh on bond prices, pushing up yields, which rise as prices fall. And Treasury yields influence other household and business borrowing costs throughout the economy, such as on mortgages and corporate bonds.

The Treasury’s new approach will shift some of that upward pressure on yields to shorter-term debt and away from longer-term debt.

That last sentence is key. What again was Operation Twist’s main goal as stated by the Fed itself? To “sanitize” inflation by driving up short-term yields and holding down long-term yields by selling and buying these maturities, respectively.