From a volatility accident to SNB flashbacks, these are some of the unexpected pitfalls that may strike the financial markets before year-end.

A December to Remember?

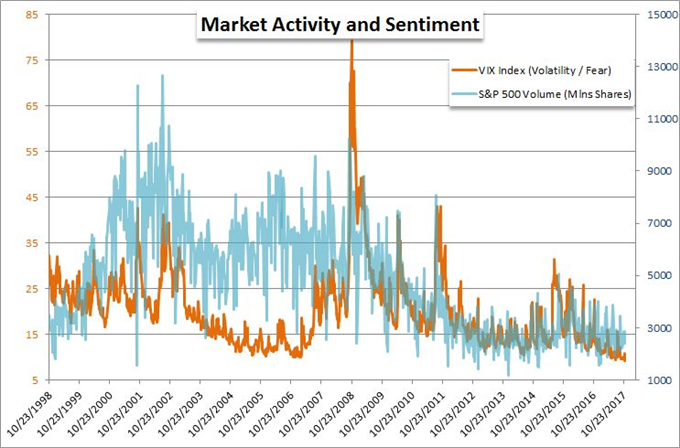

Historically, December is a consistently quiet month for the financial markets due to the abundance of market holidays and the need among funds to balance the books. However, I see a significantly higher chance this year that a volatility ‘accident’ could befall the markets between under-appreciated risks and over-extended investors. There is a record amount of leverage – both notional and thematic – being employed across the markets which makes market participants exceptional at-risk in already thinned market conditions. Consider how much return would be made by riding out a ‘long-risk’ position through the untended close to the year against the exceptional risks we face if something goes wrong.

Another sudden Swiss surprise?

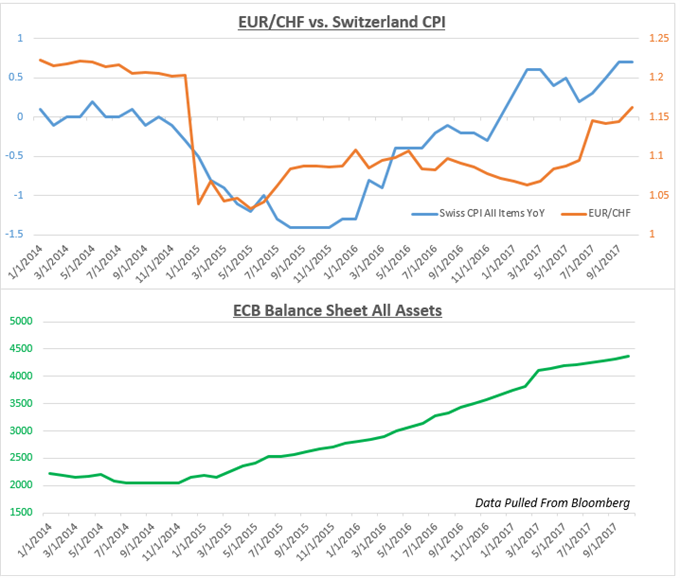

The Swiss National Bank has a penchant for shocking markets with abrupt changes in the stance of monetary policy. Swiss inflation has trended higher for nearly two years and the key EUR/CHF exchange rate is at highs unseen since before the epic collapse in January 2015. Meanwhile, the ECB has dialed back the pace of its QE effort while most political threats seen at the start of 2017 have not materialized. If Germany muddles through coalition talks despite recent setbacks and Angela Merkel looks stable at the helm, the SNB may feel secure enough to pull back on some elements of its stimulus framework, perhaps without pre-announcing it. That might produce another sharp surge in Swiss Franc volatility.

BOJ Stimulus Exit: Are We There Yet?

Bank of Japan sources have been dropping hints to various news agencies (most notably Reuters) that the extraordinary monetary stimulus provided by the Bank could be withdrawn sooner than markets expect. It’s possible that BoJ Governor Haruhiko Kuroda might allude more explicitly to this possibility before this year’s end. Be careful though. He will not be able to go too far, or to be too clear. Any change of policy cannot be announced too far in advance and the BoJ is clearly not yet ready to move. But look out for the omission of “powerful monetary easing,” so long a fixture in his commentary, and perhaps some broad sketching of what a stimulus-exit plan would look like. These will be Yen supportive, if they come.