If you’re just waking up to seeing U.S. equity futures up by more than 1%, you’re likely in a better mood than last week, when markets ended the week with the major averages down more than 1 percent. It’s been one thing after the other causing markets to decline since February. But this week marks the end of the quarter for traders and one that will find portfolio managers rebalancing and hoping for a better 2nd quarter performance for the markets. That’s right, this is the last trading week of the quarter, so traders should expect volatility in equities this week or should I rather say a continuation of volatility. The VIX, after all, ended last week at 24.87, but like equity futures rebounding, the VIX is relaxing somewhat and is presently down 7% in the premarket.

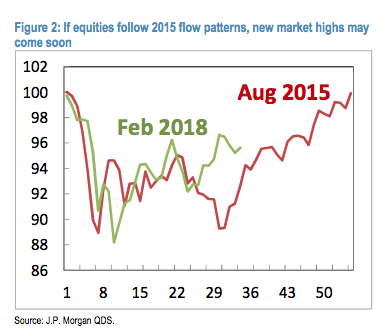

The chart below, offered by the J.P. Morgan’s quant team (subscription required), is an overlay of the August 2015 sell-off and the February 2018 sell-off in flow terms. As one can see, the current market flow has a similarity with the August 2015 sell-off.

Back in 2015, this greatly impacted the short-VOL trade forcing covering of short volatility positions, momentum triggered CTA outflows, and dealers’ option gamma prompted selling of futures. These outflows happened at a time when electronic (high-frequency) liquidity in index products collapsed. The similarities between the flow and market sell-off then are remarkable when compared to the present flow and market sell-off.

What typically happens during such market sell-offs that don’t warrant or accompany recessions is that short-term momentum returns to the markets. The causation of this market cycle is due largely to short-term options expiring within a 1-month cycle and realized volatility starts declining prompting volatility sensitive investors to renew buying activities. This all happened in 2015 and has been happening during certain periods of March. We’ll have to wait and see if 2018 more precisely mirrors the August 2015 market sell-off and volatility spike.