Below is a summary of my post-CPI tweets:

half hour to CPI. Welcome again to the private channel. Tell your friends!

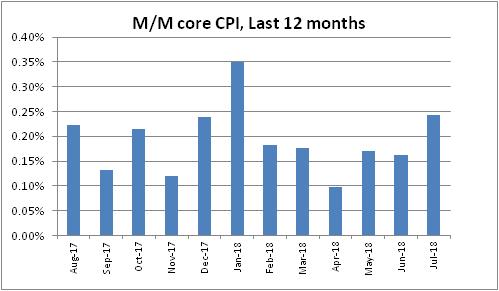

Another easy comp (0.143%) versus year ago. August 2017 was +0.222%, Sep was 0.132%, Oct was 0.214%, and Nov was 0.121%. So we still have some easy comps ahead although not easy as they were. That means core should keep rising, although slower than over the last 6 mo.

Pretty safe economist estimate for 0.2% on core and for y/y to stay 2.3% rounded. As long as m/m core is 0.162%-0.259%, y/y will stay in that range.

Rents have been leveling out recently, and not providing as much upward oomph. That passes the baton to core goods and more generally to core ex-shelter.

Ironically, even though core goods started to accelerate before any sign of tariffs, investors I think might “look through” inflation like that, which they can explain away by saying “ha ha tariffs trump ha ha.”

One other item – I will be especially attentive to Median CPI this month, which jumped to 2.80% y/y last month. That looks a little like an acceleration past the prior trend (meaning 2013-2015), well past merely erasing the 2016-17 dip.

I should note that this month’s CPI report is being brought to you from sunny Curacao! Only 20 minutes to the number.

Well, 0.23% on core CPI was a bit higher than expected, but oddly got a tick higher in the y/y to 2.354%, rounding up to 2.4%. The SA y/y is still 2.3%, but NSA is 2.4%. This happens from time to time because seasonal factors change year to year.

Last 12 Rorschach test.

CPI – Used Cars and Trucks +1.31% m/m, pushing y/y to 0.84% y/y FINALLY. Private surveys have been saying this for a while.

Owners’ Equivalent Rent +0.29% (3.395% y/y), up from 3.37%, and primary rents +0.32% to 3.628%, up from 3.58% last month. Lodging away from home +0.4% m/m after -3.7% last month, so some give-back.

Core goods back to 0% y/y, first time in 5 years it has been out of deflation!

A fair amount of that is cars.

User rating: 0.00% ( 0

User rating: 0.00% ( 0

The Complete List Of Wilshire 5000 Stocks

The Complete List Of Wilshire 5000 Stocks

Future Market Returns = Dividend Yield + Earnings Growth +/- Change In P/E Ratio

Future Market Returns = Dividend Yield + Earnings Growth +/- Change In P/E Ratio

USD/JPY Making A Bullish N Pattern Through Chuvashov Fork

USD/JPY Making A Bullish N Pattern Through Chuvashov Fork

Ebay Rises As Morgan Stanley Double Upgrades On Payments Shakeup

Ebay Rises As Morgan Stanley Double Upgrades On Payments Shakeup

The Pension Crisis Gets A Catchy Name: “Silver Tsunami”

The Pension Crisis Gets A Catchy Name: “Silver Tsunami”