Consumer Sentiment Strong

The University of Michigan consumer sentiment report showed sentiment was 100.8 in the preliminary September reading.

This beat the average estimate for 97 and last month’s reading of 96.2. It also beat the highest estimate which was 99. This report showed the most optimism since March 2018. Other than that, this was the most optimism since 2004.

Specifically, the current conditions index increased almost 6 points to 116.1. In theory, this indicates consumer spending will be strong, but that’s far from a guarantee.

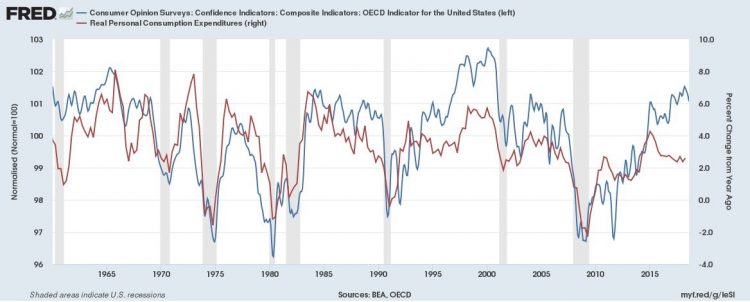

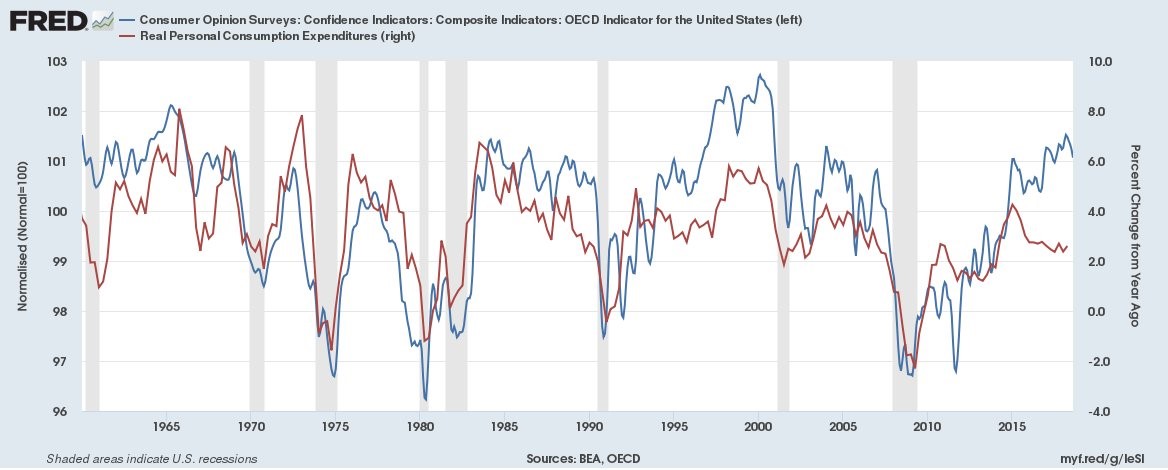

As you can see from the FRED chart below, consumer opinion surveys were correlated with real personal consumption growth up until the past few years.

Q1 had weak real consumption growth and Q2 had strong real consumption growth. Hurricane Florence could cause a spike in auto buying in September or October which would boost consumer spending in Q3 or Q4.

Some parts of North Carolina are still dealing with flooding; the last thing many victims are thinking of is buying a new car.

As I discussed in a previous article, retail sales in August were weak on a month over month basis. They were strong on a year over year basis, with particular strength in restaurant and online sales.

Consumer Sentiment – Expectations in the consumer sentiment report increased 4 points to 91.1.

Much has been made about how the current conditions index is higher than the expectations index because it’s supposed to be a bad sign. However, there’s not much more you can ask of the expectations index as it hit a 15 year high.

Tariffs were mentioned by 1/3rd of respondents instead of 1/5th like in the prior months. Obviously, the tariffs haven’t done much because consumers are very optimistic even about the future.

The fear of tariffs hasn’t equated to a changing outlook. Many consumers probably aren’t aware of the ramifications of a trade war because they haven’t lived through one.