Note: We’ve updated the charts below based on monthly data through August.

Here’s an interesting set of charts that will especially resonate with those of us who follow economic and market cycles.

Imagine that five years ago you invested $10,000 in the S&P 500. How much would it be worth today, with dividends reinvested but adjusted for inflation?

The purchasing power of your investment has increased to $18,050 for an annualized real return of 11.87%.

Had we posed the same question in March 2009, the answer would have been a depressing $6,654. The -8.12% real return would have cut the purchasing power of your initial investment by a third.

Fun Runs of the Roller Coaster

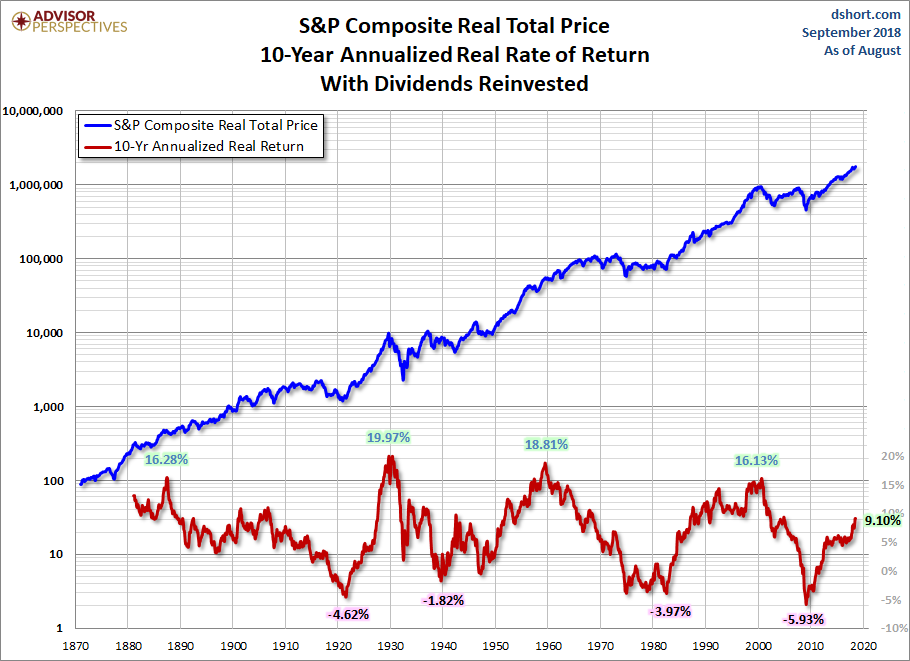

Let’s increase the time frame to 10 years. The annualized return is considerably smaller than the 5-year time frame. As of the end of last month, your $10K invested 10 years ago has grown to about $24.76K adjusted for inflation, an annualized real return of 9.10%.

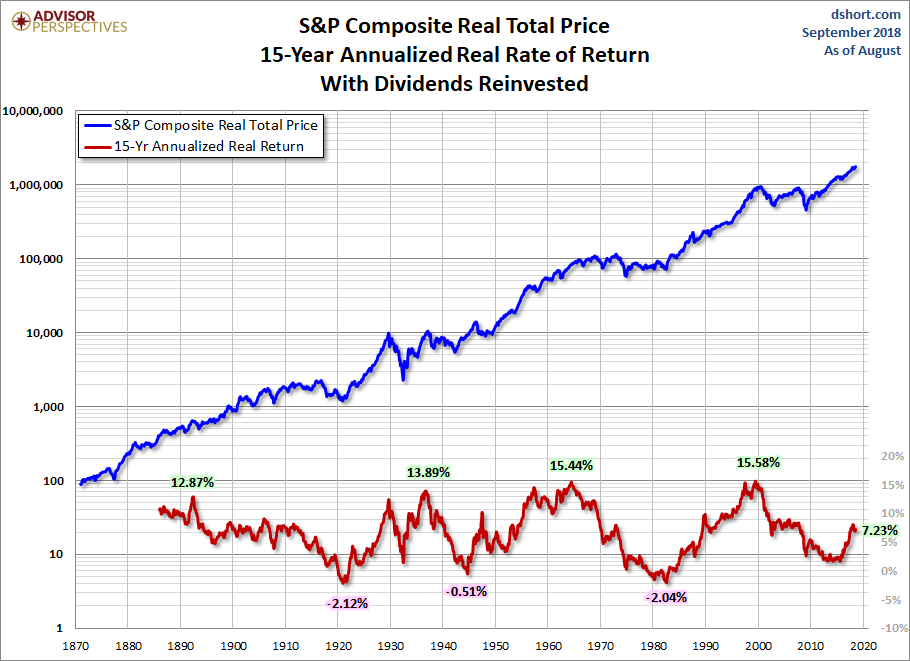

The 15-year time frame is only slightly more profitable. Your one-and-a-half decade investment of $10K has grown to about $29K adjusted for inflation for an annualized real return of 7.23%.

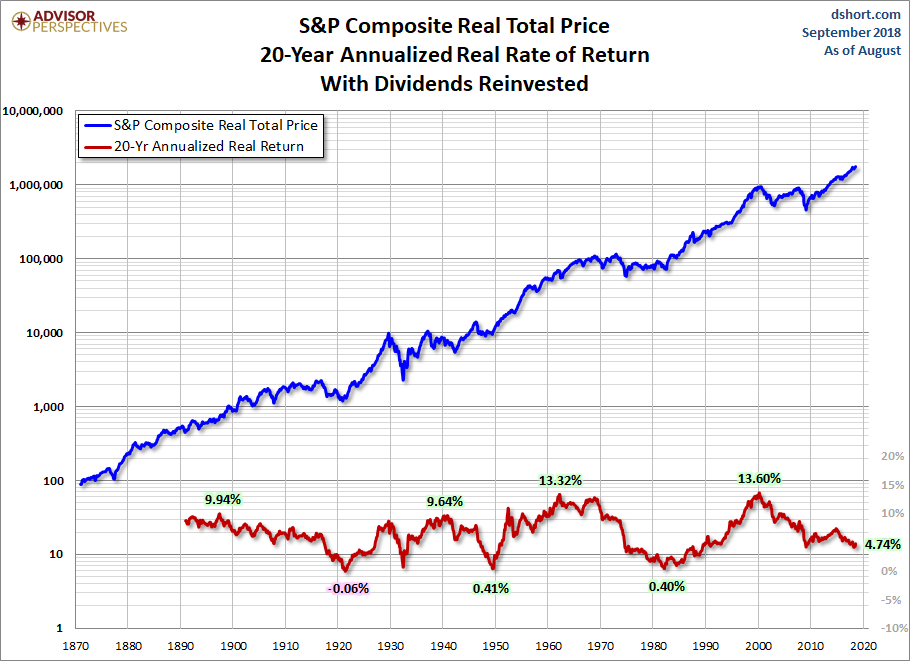

If we extend our investment horizon to 20 years, the roller coaster is less volatile with higher lows and lower highs.

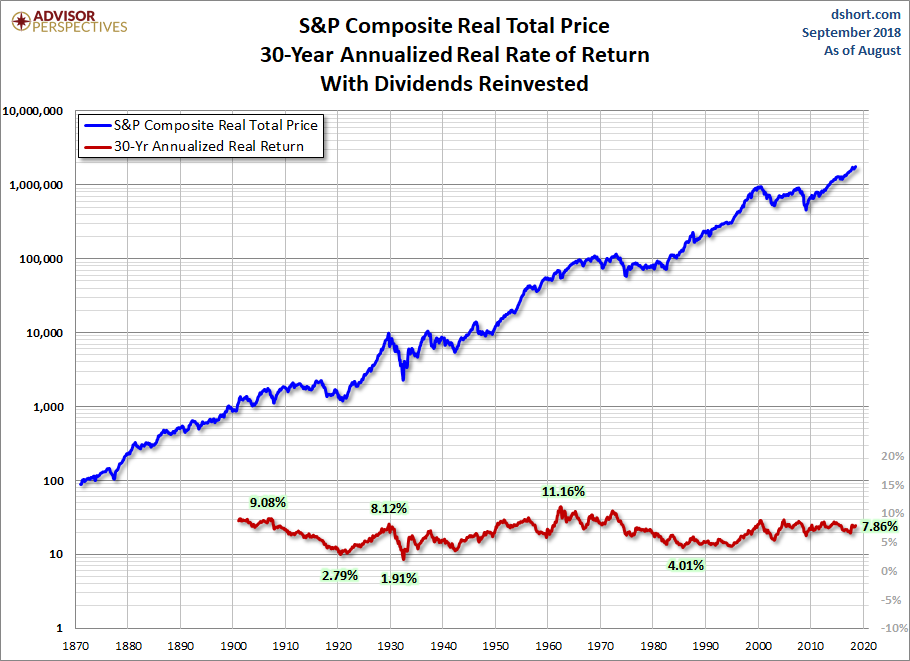

The volatility decreases further with a 30-year timeline. But even for that three-decade investment, the annualized returns since 1901 have ranged from less than 2% to over 11%.

As these charts illustrate, and as many households have discovered during the 21st century so far, investing in equities carries substantial risk. Households approaching retirement should understand this risk and make rational decisions about diversification. In the past, we’ve suggested that they should also consider fixed income alternatives for that part of the nest egg that will pay non-discretionary expenses not covered by Social Security and pensions. Unfortunately, this traditional wisdom has been less helpful in recent years owing to the Fed Zero Interest Rate Policy (ZIRP) and various stimulus strategies, which have collectively shrunk interest rates. With the end of ZIRP in December 2015 and several rounds of Fed rate hikes, it will be particularly interesting to see how this slow-motion roller coaster plays out in the years ahead.