US economic growth remains strong, based on data published to date, but today’s business-cycle profile continues to suggest that we’ve seen the peak. Recession risk remains low and near-term projections point to more of the same. The question is whether there’s trouble brewing for 2019?

At this stage it’s too early to answer with anything more than rank speculation. Looking beyond two or three months for business-cycle analysis is always a guessing game. As such, the upbeat state of the economy in the here and now remains the best guess until yet-to-be-published numbers offer a convincing reason to think otherwise. Nonetheless, the rear-view mirror tells us that the cycle has peaked and so the only mystery at this point: How far, how deep, and how long will the deceleration run?

Leaving those crucial questions aside, the macro profile for the US remains healthy. Consider, for instance, that the average nowcast for GDP growth in the third quarter (based on current estimates via the Atlanta Fed and New York Fed’) is a solid 3.3%. That’s a moderate decline from Q2’s sizzling 4.2% increase, but the current outlook for Q3 betrays no sign that a recession is imminent.

No surprise, then, that The Capital Spectator continues to estimate a virtually nil probability that a new NBER-defined downturn started in August, based on a diversified set of economic indicators. (For a more comprehensive review of the macro trend with weekly updates, see The US Business Cycle Risk Report.) One implication: Monday’s release (Sep. 24) of the Chicago Fed’s National Activity Index for August (based on the three-month average) will likely confirm that recession risk was low last month.

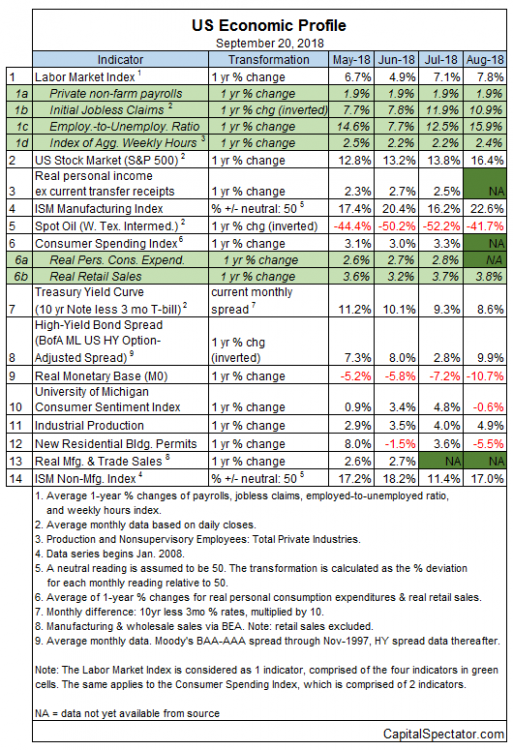

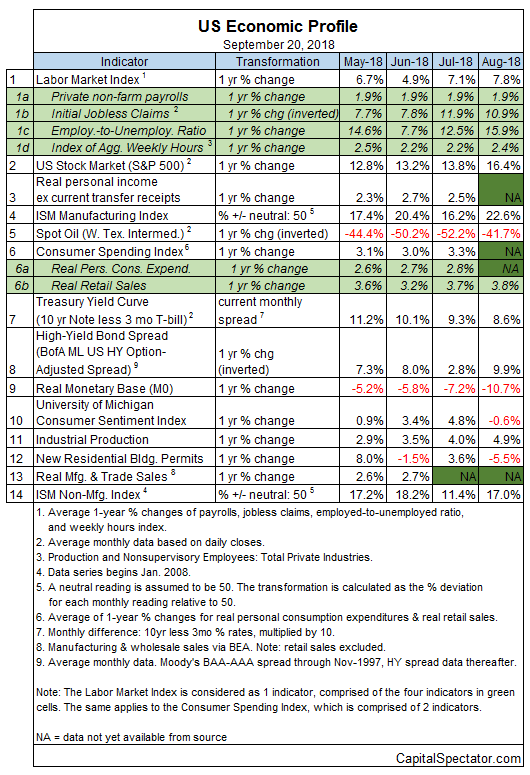

Aggregating the data in the table above continues to indicate a strong positive trend overall. The Economic Trend and Momentum indices (ETI and EMI, respectively) remain well above their respective danger zones (50% for ETI and 0% for EMI). When/if the indexes fall below those tipping points, the declines will mark warning signs that recession risk is elevated and a new downturn has started or is near. The analysis is based on a methodology that’s profiled in my book on monitoring the business cycle.