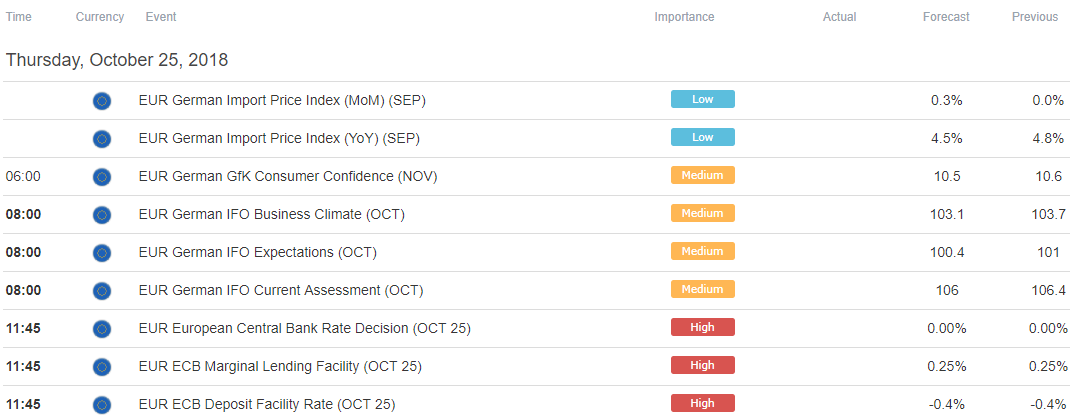

All eyes are on the ECB rate decision in European trading hours. A change in policy is not expected but the press conference with central bank President Mario Draghi following the policy announcement will be closely monitored for a forward guidance update.

As it stands, ECB plans to wind down QE asset purchases by the end of the year. Priced-in expectations implied in OIS rates suggest the first subsequent interest rate hike will come no sooner than September 2019. Euro volatility is likely if M.r Draghi’s remarks are seen to be altering that timeline.

On balance, a dovish adjustment seems more likely than the alternative. A recent rebound in inflation seems to have occurred for all the wrong reasons, reflecting a weaker currency rather than a pickup in economic activity. Indeed, PMI survey data suggests growth has slowed for most of this year.

Swelling political risk makes matters worse. The spread between Italian and benchmark German 10-year bond yields is near a five-year high as the recently installed anti-establishment government in Rome clashes with EU authorities over budget plans.

ECB tightening would only compound pressure on the debt-laden Italian economy. To the extent that this might spill over regionally and undercut bloc-wide growth, it may also derail policy normalization plans. With that in mind, Mr. Draghi and company may be inspired to moderate their position somewhat.

This can take a variety of forms. For example, the bank may signal that the reinvestment of maturing QE assets may be longer-lasting than previously thought after asset purchases wind down. Any such pivot is likely to weigh on the Euro, sending it broadly lower against its G10 FX counterparts.

ASIA PACIFIC TRADING SESSION

EUROPEAN TRADING SESSION