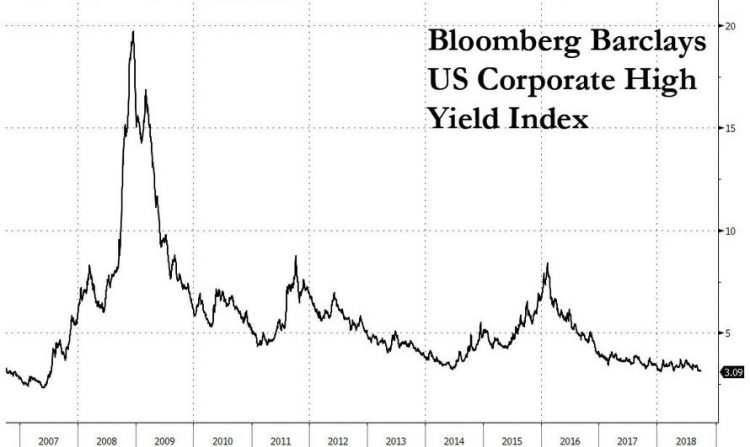

At the start of the month, we highlighted that the “incredibly shrinking junk bond spread” had just passed a historic landmark, when the Bloomberg Barclays U.S. Corporate High Yield index broke below the lowest spread since before the financial crisis, dipping to 309bps, the tightest level since late 2007.

The key reason for this relentless demand for “junk paper” has been the accelerating shrinkage in high-yield supply, as last month was the slowest September for junk bond issuance since 2011, while the high yield market as a whole has been contracting as investors have shifted their focus to leverage loans where – together with CLOs – demand has exploded recently, and the size of the loan market has soared even as the junk bond market has continued to shrink.

Meanwhile, with rates continuing to rise, investor demand has shifted ever more aggressively to floating-rate debt, i.e., leveraged loans, which provide buyers with interest rate protection as the cash interest is indexed to Libor or Prime which rises alongside the Fed Funds rate (earlier today, 3M USD Libor hit the highest since 2008) at the expense of traditional junk bonds where due to the fixed coupon, price is inversely affected by rising yields.

Which brings us to another landmark inflection point: according to Bloomberg calculations, in the past week the total notional of outstanding USD leveraged loans has just hit $1.27 trillion for the first time, overtaking the high-yield bond market which dipped to $1.26 trillion, and cementing the status of loans as the go-to financing source for junk bond companies. Additionally, October is on course for the highest loan issuance since June, while junk bond sales are the slowest since 2009.

While understandable – investors don’t want to be penalized for rising rates in the current tightening environment – the relentless growth in the loan market has prompted numerous and widespread warnings, from banks such as Bank of America and JPMorgan, to prominent investing luminaries such as Howard Marks and Scott Minerd, all the way to the Fed, which in its latest FOMC Minutes on Wednesday, warned that it is watching for “possible risks to financial stability” from the leveraged loan industry, which unlike traditional junk bonds, belongs largely to the domain of non-bank lenders and as a result is generally unsupervised by regulators.