Following a long wait, 2017 was the year that being a globally diversified investor finally seemed to pay off. The MSCI ACWI ex USA Index beat the S&P 500 by more than 500 basis points (bps), outperforming for the first time since 2012. Many wondered if the baton was finally being passed to the international markets—after a decade of lagging the U.S.—to lead us into the next stage of the global equity rally.

Funny how quickly things can change.

It seems like a long time ago, but for the first four months of 2018, the U.S., the EAFE region (consisting of Europe, Australasia and the Far East) and emerging markets (EM) regions all performed almost exactly in line with each other. Since then, a massive gap has emerged. Over the last six months, the S&P has beaten the MSCI ACWI ex USA Index by more than 14.5%—a performance gap that falls into the top decile of history.

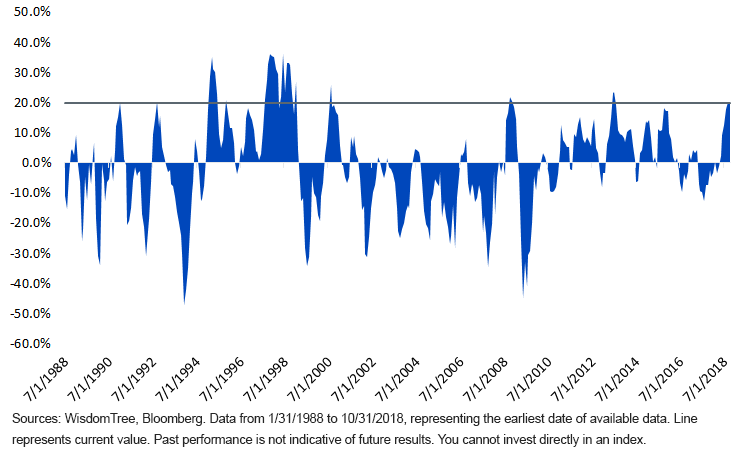

Looking at EM, the difference has been even more stark, with a nearly 20% gap between the two regions in just six months—in the 92nd percentile of history!1 Outside of the Asian debt crisis in the late 1990s, outperformance of this magnitude has not tended to last long; given the stark differences in fundamentals in the asset class between now and then, it seems reasonable to believe an eventual reversion to the mean will arrive.

S&P 500 – MSCI Emerging Markets Trailing Six-Month Performance

Was October 2018 an Inflection Point?

Even with the recent U.S. outperformance, there are some signs that the divergence momentum has slowed. The S&P 500 lost 6.8% in October, its worst month since September 2011. October seemed like an inflection point in the U.S. markets, with sentiment shifting away from what had previously done well: