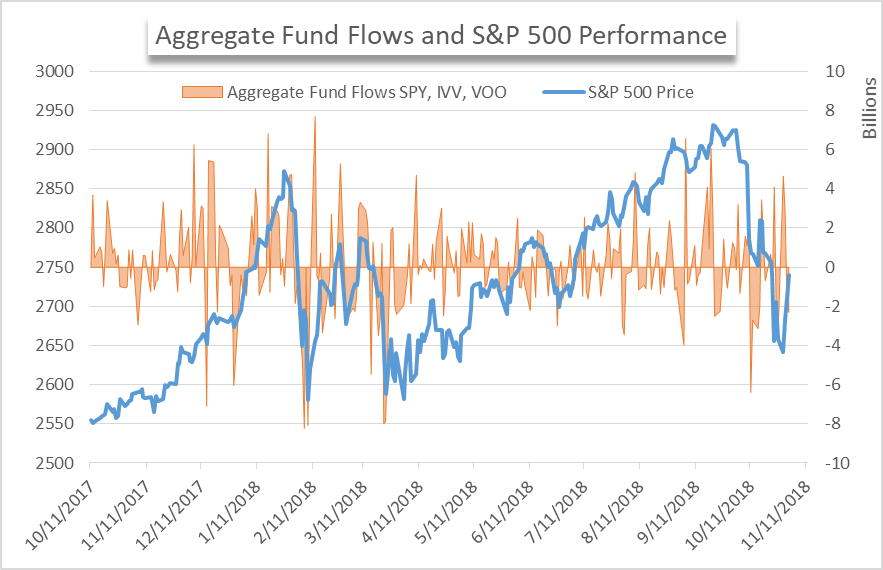

After scrambling out of correction territory earlier in the week, the S&P 500 closed slightly lower Friday. At the close, the index is now -7.15% below its peak on September 21st. Still, meaningful gains were posted this week and the index is once again positive for 2018. Some investors may have sensed a bottom as they poured an aggregate $4.65 billion into VOO, SPY, and IVV on Monday.

S&P 500 Hourly Price Chart October 2018

In total, the three ETFs saw $3.5 billion in inflows for the week. That puts the monthly total at $3.4 billion during a period when the S&P 500 shed over -6.5%. The consistent demand for US equity exposure suggests investors are still content with the risk profile of the asset class. However, there are some areas where that demand may be waning.

Aggregate Fund Flows versus S&P 500 Performance

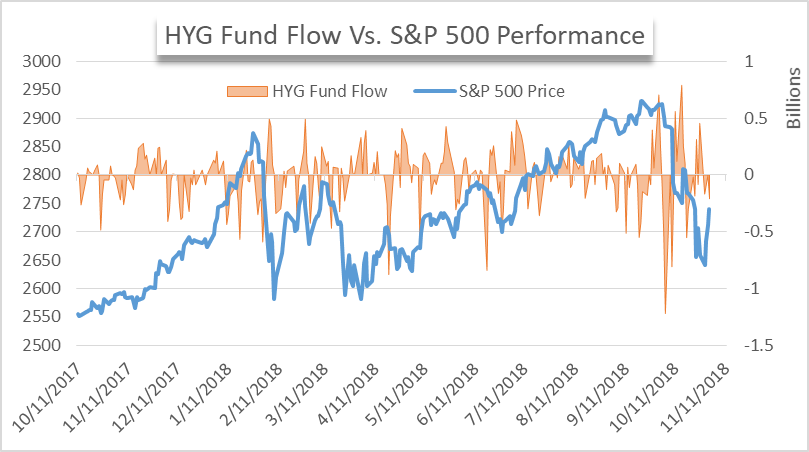

One such area is the high yield corporate bond (HYG) ETF. Rising interest rates have distorted the risk premium offered by the underlying asset and thus the fund saw consistent outflows this month. Outflows totaled -$861 million or roughly 6% of the fund’s market capitalization. Further, HYG saw its largest single-day outflow since late 2016 earlier in October.

High Yield Corporate Bond ETF (HYG) Fund Flow and S&P 500 Price

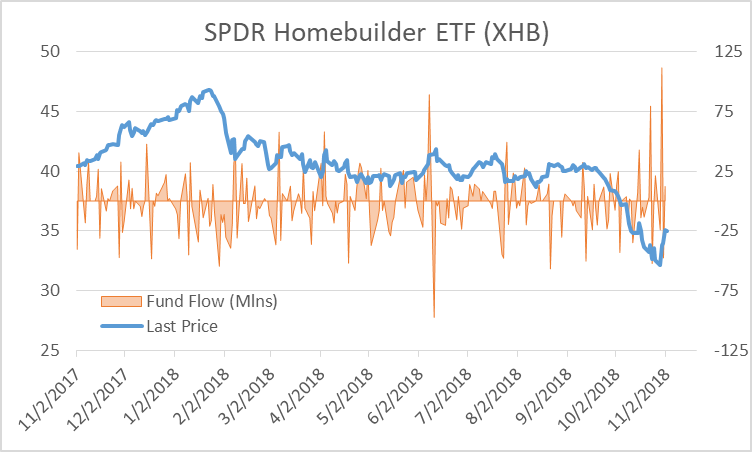

Federal Reserve officials may hike rates again at next Wednesday’s meeting, although highly unlikely. Rising rates have also weighed on the housing market. This week, mortgage applications dipped and a consumer confidence survey revealed fewer American’s plan to buy a home in the coming months.

Unsurprisingly, the rising rate environment has exerted downward pressure on the SPDR Homebuilder ETF XHB. Interestingly, XHB saw its largest single-day inflow for the year and the largest since late 2016 this week.

SPDR Homebuilder ETF (XHB) Fund Flows and Price

The inflows could suggest some investors see the impact of rising rates as overblown. Similarly, the fund closed at its lowest price in nearly two years on Tuesday so the flows could be a simple “buy the dip” move by shorter-term investors. Either way, next week’s FOMC decision and minutes will offer crucial insight for the outlook of XHB and the housing sector.