The US Dollar (via the DXY Index) has seen prices alternate between gains and losses on Wednesday as market participants digest the results of the 2018 US midterm elections. With the base case scenario having been achieved – Democrats controlling the House, Republicans controlling the Senate – reaction across financial markets has been limited.

If there is a surprise about the election results, it’s the extent to which Republicans extended their majority in the Senate. Such gains portend to an environment that makes it more likely Republicans will also control the Senate after the 2020 elections. To this end, with the Trump tax plan largely to remain in place for the foreseeable future (years), US equity markets have been outperforming as one of the major factors lead to strong earnings growth is likely to stay in place.

Otherwise, fiscal policy gridlock is coming. The only significant area of agreement between House Democrats and President Trump is infrastructure, but it’s still a longshot that a deal can be reached after such a confrontational election season. Deregulation efforts may be slowed, but will ultimately continue as Trump-appointed agency heads will remain in place.

If you missed it, now that the midterm elections are in the rearview mirror, it’s a good time to review the top charts and themes that will come back into focus as the calendar winds down into the end of the year.

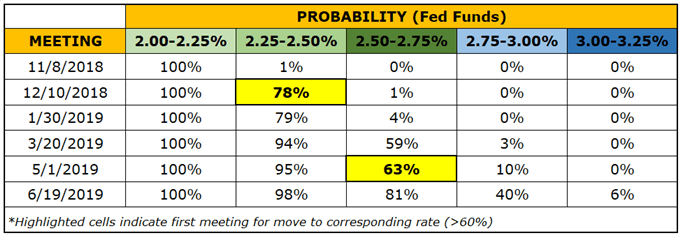

Looking ahead to tomorrow, as far as FOMC meetings go, the November gathering should turn out to be one of the duller central bank rate decisions in 2018. Rates markets are pricing in a 1% chance of a 25-bps rate hike, effectively making the meeting a placeholder for future gatherings.

Fed Rate Hike Expections (November 7, 2018) (Table 1)

The lack of anticipated action at the November meeting shouldn’t be a surprise, as market participants have been classically conditioned by policymakers at the major central banks to only anticipate policy changes when new forecasts are in hand and the head of the central bank is afforded a press conference: November will yield neither of these; December will. Accordingly, there is a 78% chance of a 25-bps hike next month.