As we wrote in our preview of NVDA’s Q3 earnings, it is safe to say that more were paying attention to today’s earnings report from Nvidia than did to all of the other giga caps or frankly any other company this quarter, thanks to the thunderous, impact Nvidia has had on the broader market in general, and the AI bubble in particular. And while the excitement may not have been as palpable as last quarter when JPM trader Stuart Humphrey said “The anticipation is LITERALLY killing us!” (clearly he was being metaphoric since he is still alive), UBS said that while positioning has come down from a scale of 10 in last print to 9 now, expectations remain stratospheric and while sentiment is better than last print, it isn’t as strong as the Goldilocks scenario into May Print that saw a +25% move.Well, the anticipation is finally over, and moments ago NVDA reported Q3 earnings that crushed estimates and gave Q4 guidance that while also above consensus, was in line with the top end of the whisper range, which may have disappointed some as it shows that even NVDA may have a limit to its growth.Here is what NVDA reported about Q3 earnings:

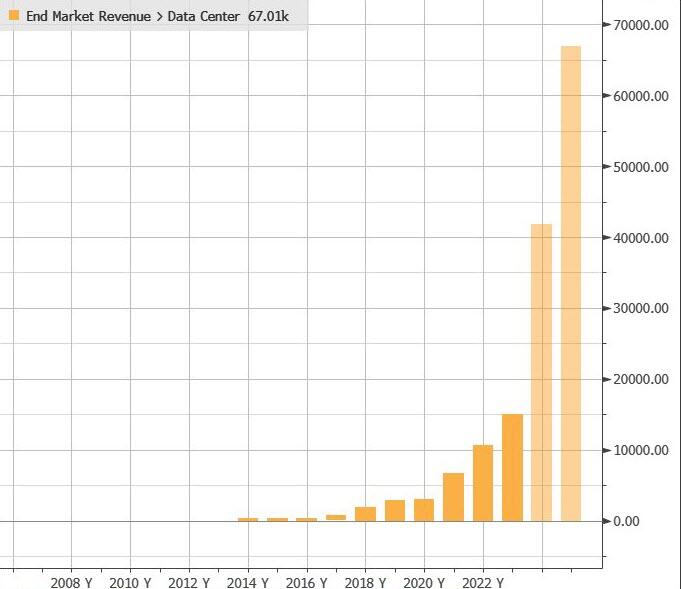

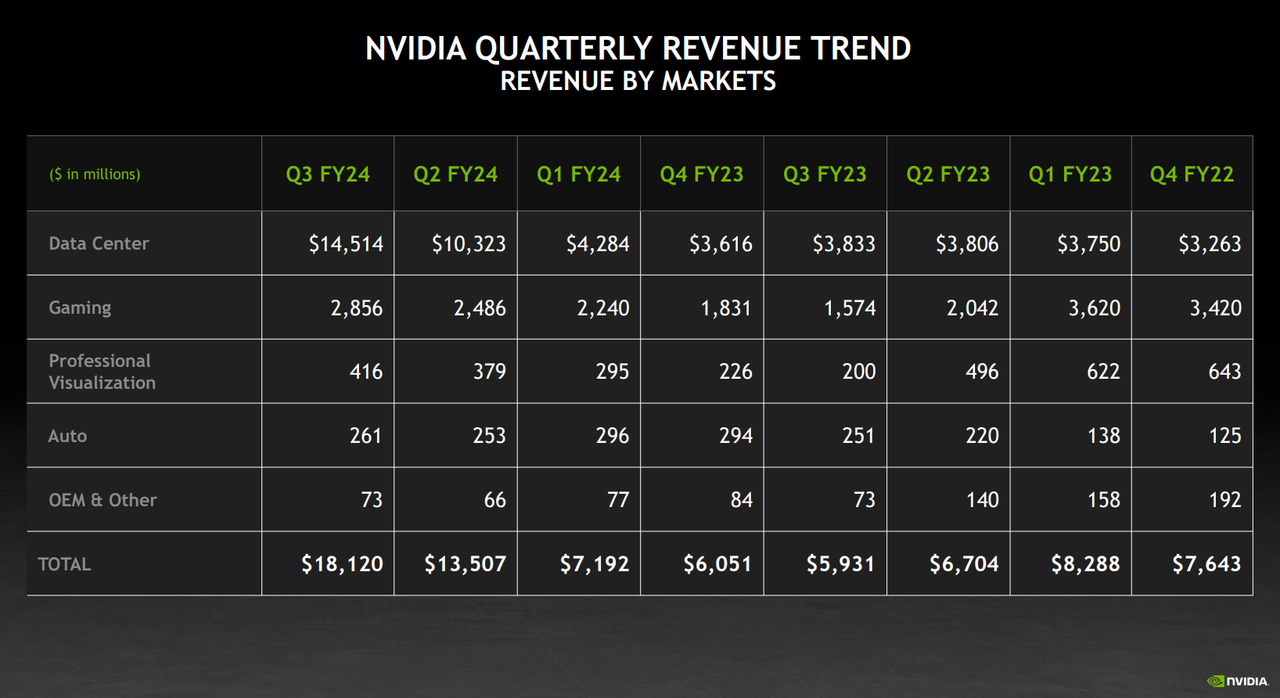

- Data center revenue $14.51 billion vs. $3.83 billion y/y, beating estimates of $12.82 billion

- Gaming revenue $2.86 billion, +82% y/y, beating estimates of $2.7 billion

- Professional Visualization revenue $416 million vs. $200 million y/y, beating estimate $409.2 million

Some more details on the revenue breakdown:

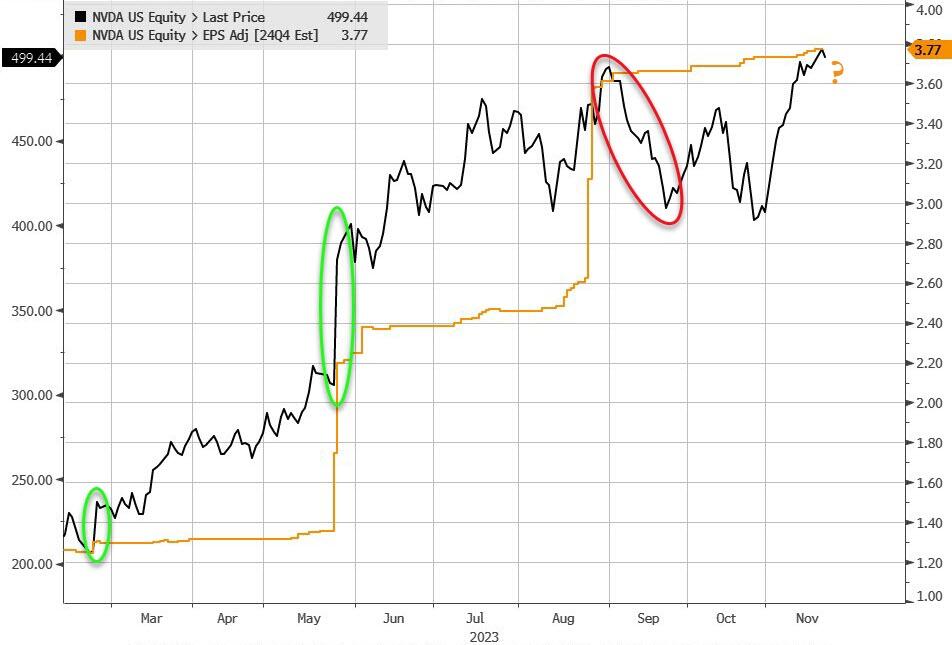

The chart below shows all you need to know about the company’s main revenue driver

Going down the line:

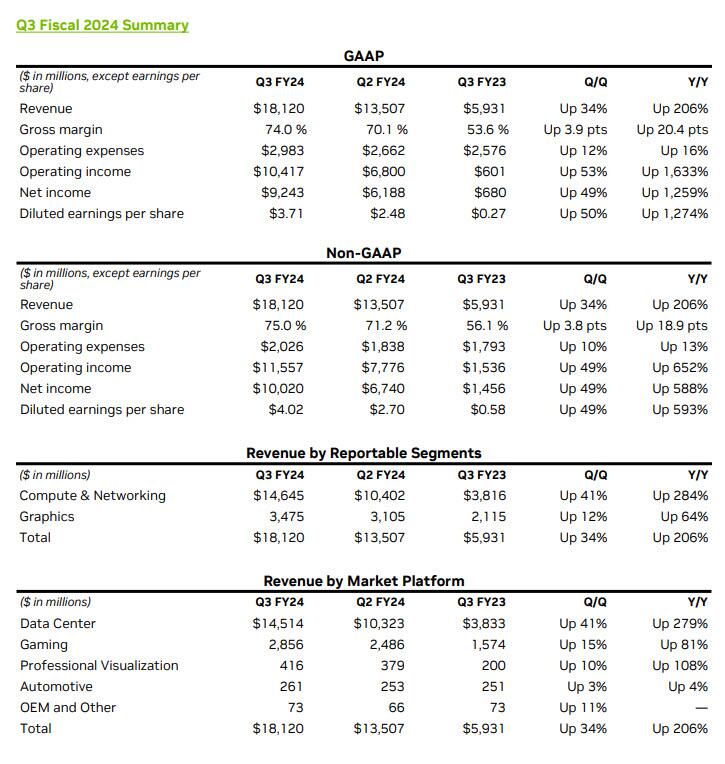

- R&D expenses $2.29 billion, +18% y/y, higher than the estimate $2.21 billion

Gross Margin:

Expenses:

The financial results in a nutshell:

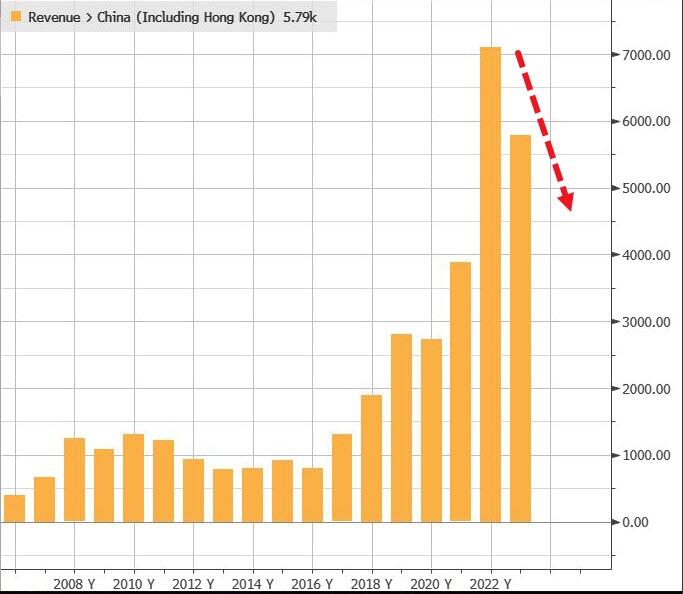

Commenting on the results, CEO Jensen Huang said that “our strong growth reflects the broad industry platform transition from general-purpose to accelerated computing and generative AI…. Large language model startups, consumer internet companies and global cloud service providers were the first movers, and the next waves are starting to build. Nations and regional CSPs are investing in AI clouds to serve local demand, enterprise software companies are adding AI copilots and assistants to their platforms, and enterprises are creating custom AI to automate the world’s largest industries…. NVIDIA GPUs, CPUs, networking, AI foundry services and NVIDIA AI Enterprise software are all growth engines in full throttle. The era of generative AI is taking off,” he said.Maybe it is… but China is starting to stumble, because as the company admitted, sales to China “will decline significantly in the fourth quarter of fiscal 2024, though we believe the decline will be more than offset by strong growth in other regions” to wit:

Our sales to China and other affected destinations, derived from products that are now subject to licensing requirements, have consistently contributed approximately 20-25% of Data Center revenue over the past few quarters. We expect that our sales to these destinations will decline significantly in the fourth quarter of fiscal 2024, though we believe the decline will be more than offset by strong growth in other regions.

The market did not like that. It also did not like that the guidance – which handily beat consensus – only matched the top end of the whisper range, which recall according to JPM, was $19.5BN to $20.0BN. Here is NVDA’s full Q4 and full year guidance:

- GAAP and non-GAAP gross margins are expected to be 74.5% and 75.5%, respectively, plus or minus 50 basis points.

- GAAP and non-GAAP operating expenses are expected to be approximately $3.17 billion and $2.20 billion, respectively.

- GAAP and non-GAAP other income and expense are expected to be an income of approximately $200 million, excluding gains and losses from non-affiliated investments.

- GAAP and non-GAAP tax rates are expected to be 15.0%, plus or minus 1%, excluding any discrete items.

So how did the market react? Well, the blowout earnings were certainly good news… but the warning about declining China sales and the guidance which only tagged the top end of the whisper guidance, that was not quite as exciting, and as a result, the stock initially dumped as much as $30 after hours, before recovering most of its losses, but has since resumed drifting lower again…

… setting up the stock for its first post-earnings drop since the advent of ChatGPT almost exactly one year ago.  Which begs the question: now that Nvidia performed only in line, was this it for the tech/Mag 7 rally?More By This Author:‘Hawkish’ FOMC Minutes: Warn On Fading Consumer, Financial System Stability Risks

Which begs the question: now that Nvidia performed only in line, was this it for the tech/Mag 7 rally?More By This Author:‘Hawkish’ FOMC Minutes: Warn On Fading Consumer, Financial System Stability Risks

Inflation-Battered Americans Raiding 401k’s To Pay Mortgages And Rent

Ranking The Credit Ratings Of Major Economies