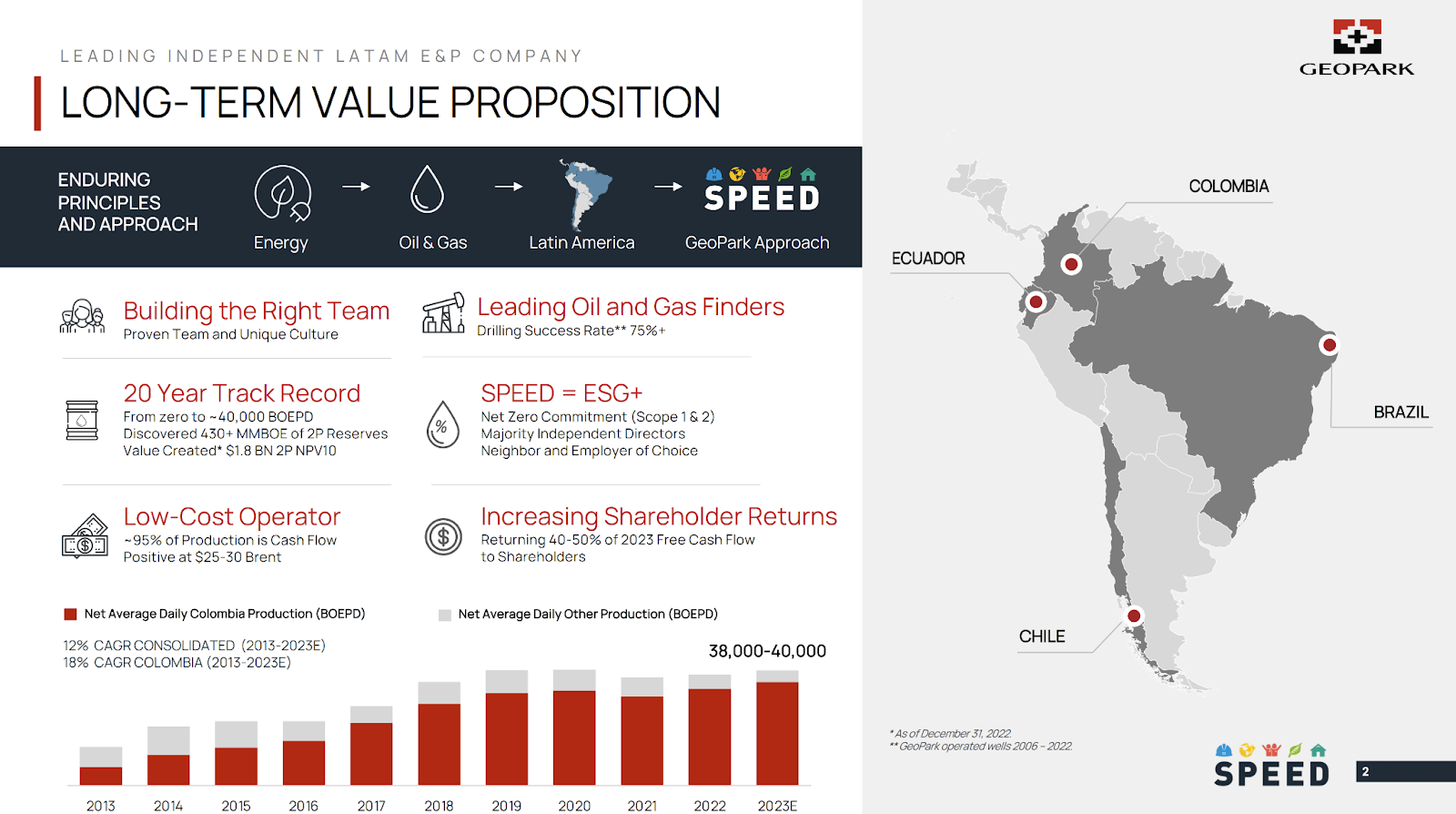

It’s been a turbulent year for the markets, to say the least. FreepikInterest rates have been surging, labor strikes have taken a bite out of the automobile and entertainment industries, a few big banks have failed, and wars are raging on two continents.The future looks no less uncertain. Inflation has eased a bit, but it’s still too high for the Fed to fully ease up on interest rates. The wars in Europe and the Middle East continue, making food and energy prices more volatile than they have been in years.And closer to home, next year proves to be one of the most divisive election years in memory.In short, 2024 promises to be another uncertain year in the markets.That’s why we’ve had our team of analysts and researchers identify the most promising stocks to keep an eye on in 2024.Let’s take a look…Stock #1 for 2024 – GeoPark Ltd. (GPRK)Analyst: Jay Soloff, StockNews, POWR IncomeI’ve spoken before about the price support that is in place for oil globally, and the recent outbreak of violence in the Middle East will only serve to bolster recent price increases.Due to its small size and location in Colombia, GeoPark Ltd. (GPRK), an upstream oil and gas company, simply flies under the radar of most investors. But after taking a close look under the hood, I believe there’s a compelling story here. Actually, GeoPark is an income stock in value clothing.Take a peek at what I found…Business OverviewGeoPark is a leading independent exploration, developer and producer of oil and gas reserves in Chile, Colombia, Brazil, Argentina and Ecuador. Fact is, Latin America remains one of the world’s richest and most underexplored hydrocarbon regions.GeoPark’s value begins in its drilling operations where GPRK has a 75% drilling success rate over the past 16 years.Its prize asset is the Llanos 34 block—in its own words, “the largest oil discovery in over 20 years in Colombia.” Gross production has rocketed from zero to 75,000 barrels of oil per day in less than a decade.The drilling site was purchased for $30 million in 2012, has produced almost $2 billion since drilling began, and is estimated to contain another $2 billion of production today.GeoPark also has a strategic partnership with ONGC Videsh – the government oil company of India – to jointly acquire, invest in, and create value from upstream oil and gas projects across Latin America. The company has net proven reserves of 87.8 million barrels of oil equivalent.Here’s a look at all of GPRK’s operations:

FreepikInterest rates have been surging, labor strikes have taken a bite out of the automobile and entertainment industries, a few big banks have failed, and wars are raging on two continents.The future looks no less uncertain. Inflation has eased a bit, but it’s still too high for the Fed to fully ease up on interest rates. The wars in Europe and the Middle East continue, making food and energy prices more volatile than they have been in years.And closer to home, next year proves to be one of the most divisive election years in memory.In short, 2024 promises to be another uncertain year in the markets.That’s why we’ve had our team of analysts and researchers identify the most promising stocks to keep an eye on in 2024.Let’s take a look…Stock #1 for 2024 – GeoPark Ltd. (GPRK)Analyst: Jay Soloff, StockNews, POWR IncomeI’ve spoken before about the price support that is in place for oil globally, and the recent outbreak of violence in the Middle East will only serve to bolster recent price increases.Due to its small size and location in Colombia, GeoPark Ltd. (GPRK), an upstream oil and gas company, simply flies under the radar of most investors. But after taking a close look under the hood, I believe there’s a compelling story here. Actually, GeoPark is an income stock in value clothing.Take a peek at what I found…Business OverviewGeoPark is a leading independent exploration, developer and producer of oil and gas reserves in Chile, Colombia, Brazil, Argentina and Ecuador. Fact is, Latin America remains one of the world’s richest and most underexplored hydrocarbon regions.GeoPark’s value begins in its drilling operations where GPRK has a 75% drilling success rate over the past 16 years.Its prize asset is the Llanos 34 block—in its own words, “the largest oil discovery in over 20 years in Colombia.” Gross production has rocketed from zero to 75,000 barrels of oil per day in less than a decade.The drilling site was purchased for $30 million in 2012, has produced almost $2 billion since drilling began, and is estimated to contain another $2 billion of production today.GeoPark also has a strategic partnership with ONGC Videsh – the government oil company of India – to jointly acquire, invest in, and create value from upstream oil and gas projects across Latin America. The company has net proven reserves of 87.8 million barrels of oil equivalent.Here’s a look at all of GPRK’s operations:

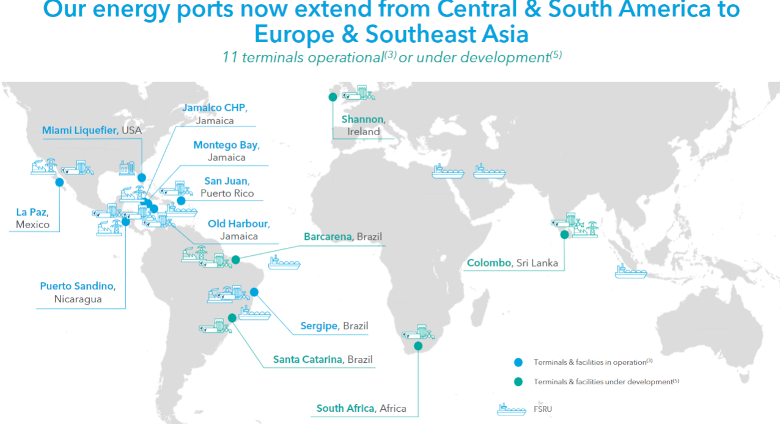

They will not accomplish that.Nor will they help you when their advice turns sour.In short, predicting the market is a waste of time. You are far better off reacting to what the market does during the year.When stocks sell off and everyone hates stocks, you should look for good companies at great prices. It will make you a lot of money over a year or two.If you find companies with outstanding momentum attracting institutional buying, you should buy them. As long as the fundamentals improve, the stock price should keep climbing higher.If stocks soar in value and sell for ridiculous multiples of asset values and cash flows, you should sell them.If you can buy bonds in companies with a high probability of surviving until the principal is due, that yield more than historical stock market returns, you should do that.I know that is not what you want to hear.It is not what publishers or market directors want to see either.It’s the right way to approach investing in 2024, but everyone wants magic stock picks.I will not give you any of the picks I gave my members. It hardly seems fair to give you something they are paying for, does it?Since the two anomalies that never go away, which I mentioned above, are value and momentum, I will give you two cheap stocks that could recover and give you huge returns. Both have passed my credit filters and should not experience any severe financial distress in 2023.Along with that, I will give you stocks with fundamentals and price momentum that have the potential to keep climbing higher.Our first value pick is JELD-WEN Holdings (JELD). This company makes windows and doors for homebuilders, home improvement, and replacement markets. It will be a bumpy road, but we need new homes, especially at the lower end of the market, to meet demand, which could drive substantial profit gains for JELD-WEN.The upside could be enormous with the stock trading at an enterprise to earnings before interest and taxes multiple of just 5.My next pick combines being undervalued and something of a long shot. PHX Minerals (PHX) is a natural gas and oil mineral company with acreage in Oklahoma, Texas, Louisiana, North Dakota, and Arkansas. It is a royalty company that has been working to increase its acreage and grow cash flows. The stock is currently trading at just 94% of tangible book value.The company just turned down a takeover offer from a larger royalty company as inadequate. A higher offer in 2024 would not be a surprise.Our first momentum stock is an Orlando-based company, MtronPTI (MPTI). The company makes radio frequency components that it sells to all the major defense companies. Its products are used in space flight, defense, aircraft, and instrumentation for air and spacecraft.Its products are also used in hypersonic missiles, missile defense, drones, and electronic warfare.Business is good.Thanks to geopolitics and the overwhelming stupidity of nations, it will keep getting better.Sales and earnings are growing. Margins are expanding. Analysts are raising estimates for sales and profits this year and next.Fundamental momentum is driving strong price momentum.Profile Systems (PFIE) makes burner management and combustion systems for the oil and gas industry. Its products make using burners that are part of the oil and gas production process safer by acting as a kind of thermostat to prevent accidents.It’s a low-priced stock with strong sales and earnings momentum that is attracting buying pressure from institutional and retail buyers alike. Profits have exceeded analyst expectations, and Wall Street has been raising its estimates for Profire’s earnings in 2023 and 2024.Profire’s fundamentals have everything you want to see in an outstanding growth stock. If that continues, this could be one of the biggest winners of 2024.There you have it.Flawless predictions for market behavior in 2024 that have been correct every year for all my years in the business.Two growth stocks and two value stocks that have the characteristics of winning stocks.Anything more is just guesswork and marketing.Now, if you will excuse me, I have to go work on the shopping list for Thanksgiving and figure out what to buy the granddaughters for Christmas. Stock #7 2024 – Main Street Capital (MAIN)Analyst: Tim Plaehn, Investors Alley, The Dividend HunterI regularly review a large number of high yield stocks. I try to dig out the details that separate a high-quality company from one that has the potential to truly whack investor wealth. I often talk about how tremendous value can be found in the dark corners of the stock market, where the investing public doesn’t understand how these undiscovered nuggets of dividend paying companies operate. But sometimes I realize I need to go back and discuss a stock that should be a core holding for almost every stock market investor.And this one may just be the best income stock that exists.That’s why Main Street Capital (MAIN) is my conservative pick for 2024. The increase in interest rates dictated by the Fed over the last year has been very good for the profitability of business development companies (BDCs). Main Street Capital is the class of the BDC sector. The company has an unmatched record of dividend growth. MAIN pays monthly dividends. Plus the company historically has paid quarterly supplemental dividends.MAIN is a stock that will produce consistent low to mid-teens compound annual total returns.Legally, a BDC is a closed-end investment company, like closed-end mutual funds (CEF). The difference is that a CEF owns stock shares and bonds, while a BDC makes direct investments into its client companies.A BDC will have up to hundreds of outstanding investments to spread the risk across many small companies. The client companies of a BDC will be corporations that are too small or too new to be able to issue stock or bonds into the publicly traded markets.As a risk control factor, BDCs are limited to debt of no more than two times its equity.This means that if a BDC has $500 million of equity raised from selling shares, it can borrow $1 billion. The company can then make $1.5 billion of loans or equity investments.Main Street Capital Corp. is really quite different from the rest of the BDC crowd. Since its 2007 IPO, MAIN has tripled the total return average of its BDC peers.Houston-based Main Street Capital has helped over 200 private companies grow or transition by providing flexible private equity and debt capital solutions.The company provides “one-stop” capital solutions (private debt and private equity capital) to lower middle market companies and debt capital to middle market companies.Main Street’s lower middle market (LMM) companies generally have annual revenues between $10 million and $150 million. While Main Street’s middle market debt investments are made in businesses that are generally larger in size.The company’s current investment portfolio consists of 51% LMM, 36% Private Loan and 7% Middle Market companies and 6% other investments.On December 31, 2021, Main Street Capital had 30 middle market clients with an average loan amount of $13 million. The loans total over $306 million or about 7% of MAIN’s total portfolio.Middle market loans are floating rate and match with MAIN’s floating rate debt facility. The average 11.8% yield on this group of loans is 4.75% higher than Main Street’s debt used to fund the loans to clients. The 4.5% interest margin is almost pure cash flow that can be used to help pay dividends on MAIN’s stock shares.The largest portion of the portfolio is lower middle market (LMM), where the company takes equity stakes along with providing debt financing. Equity provides a significant boost to the total returns generated. Lower middle market companies are smaller than the typical BDC client and have annual revenues between $10 and $150 million.There are over 175,000 companies in this revenue bracket in the U.S., and MAIN has 79 lower middle market clients with loans and equity investments worth $2.1 billion. The loans to the companies in this part of the portfolio have an average yield of 12.6%.The equity position gives an average 41% ownership of the client companies. The equity stakes are what have allowed MAIN’s net asset value (NAV) to increase from $12.85 in 2007 to $27.23 on March 31, 2023 – 112% growth.The equity investments are what set MAIN apart from most other BDCs. The rules under which these companies operate prevent them from setting aside loan loss reserves. Because a BDC makes higher risk loans, there will be loan losses. These losses have a direct negative effect on a BDC’s book or net asset value. That is why most BDCs struggle to maintain their book values compared to the growing value built by Main Street Capital.In recent years, Main Street has been growing what it calls its PrivateLoan Portfolio. These are loans originated through strategic relationships with other investment funds on a collaborative basis and are often referred to in the debt markets as “club deals”.The private loan portfolio makes up 36% (86 loans for $1.5 billion) of the overall MAIN portfolio and carries an average yield of 12.4%. The loans have floating interest rates and benefit from lower overhead costs.This three-tier investment portfolio is what sets MAIN apart from the rest of the BDC crowd, and what makes it an income stock for all seasons.The lower middle market client, middle market client, and private loans mix provides a combination of net interest income to support MAIN’s very excellent history of dividend payments. Plus, MAIN holds an industry leading position in cost efficiency, with an Operating Expense to Assets Ratio of 1.4%.The result has been a BDC that has generated both regular dividend growth for investors and special dividends to pay out capital gains. As an additional bonus, MAIN pays monthly dividends, smoothing out the cash flow into your brokerage account. MAIN should be a core holding for any income focused investor.These facts add up to a very high-quality income investment with a 7% yield on the monthly dividends alone. The bonus dividends are just that, an added bonus on top of a great yield. The regular dividend increases will result in a low-teens yield on cost in just a few years. I know of no other stock that can be counted on to pay you 12-plus dividends per year and provide a growing cash income stream. If you do not own any MAIN shares, go buy some. Stock #8 2024 – New Fortress Energy (NFE) Analyst: Tim Plaehn, Investors Alley, The Dividend HunterOngoing global events have me convinced that liquified natural gas (LNG) could be the world’s most important energy source for years—possibly decades—to come. The LNG infrastructure system allows the cost-effective transport of clean-burning natural gas from regions of plentiful supply to more populous countries with limited energy sources.That’s why, for a more aggressive play for 2024, I’ve chosen New Fortress Energy (NFE). It’s a rapidly growing company focused on developing and operating downstream LNG infrastructure assets including LNG regassification and power generation. New Fortress also has employed the first of its Fast Gas upstream liquefaction plants that is installed on an offshore oil and gas rig. Business OverviewNew Fortress Energy operates primarily as a downstream seller of natural gas, delivered to its global network of LNG gasification terminals.At the end of 2021, New Fortress Energy had 11 regasification terminals, up from five a year earlier. Now the company shows 14 facilities either operating or under development. Gas transport ships totaled 20, up from five. These assets provide LNG midstream and downstream services. New Fortress Energy will soon complete the cycle with its first LNG upstream investment. New Fortress Energy operates on long-term contracts to deliver LNG-based natural gas to customers served by the transport and terminals network. The contracts make New Fortress the exclusive gas supplier to its contracted customers.

To continue to expand, New Fortress Energy is moving to upstream LNG production with what it calls Fast LNG (FLNG). The first project will be to provide offshore liquefaction at Italian integrated energy company Eni’s offshore development in the Republic of Congo.On March 31, 2022, the company filed to build its second Fast LNG offshore LNG export plant, off the coast of Louisiana. The company plans to have this plant up and running in 2023. In July, a third FLNG project was added to develop facilities off the coast of Mexico.The Fast LNG projects will provide low-cost LNG to be resold to the company’s upstream customers.The next project will be a green hydrogen production facility located in Texas. The plant will produce clean hydrogen close to end-users in the power generation, petrochemical, refining, and steel sectors. Investment ConsiderationsDuring the 2021 fourth-quarter earnings call, New Fortress CEO Wesley Edens noted, “This really does mark the end of the beginning of us as a company.”By that comment, he means the company has invested a lot of capital over the last few years to get to the point where the company is now very profitable, and additional capital investment will grow those profits.Long-term LNG supply contracts provide a stable revenue base. The Fast LNG facilities will produce low-cost LNG to supply those contracts. Fast LNG can also ramp up production during price disruption to sell more gas into the markets when prices spike higher.All in all, New Fortress Energy has strong visibility for the next two years of tremendous earnings growth. The company is also poised to continue to grow as LNG becomes the dominant form of global energy.Currently, NFE pays a $0.10 quarterly dividend, for a 1% yield. The dividend has been paid since the 2020 fourth quarter.In December 2022, the company announced a supplemental dividend plan to pay out 40% of adjusted EBITDA in semi-annual installments. A $3.00 per share dividend was declared at that time and paid in January.New Fortress generated EBITDA of $600 million in 2022, will exceed $1 billion in 2023, and is forecasting $1.6 billion and $2.4 billion for 2024 and 2025, respectively.More By This Author:2 Long Shot Investments To Start Your 2024 Off RightWhat I’m Excited For In 2024 Two All-Or-Nothing Longshot Stocks For Thanksgiving